The Fed – Between a Rock and a Hard Place

July 31, 2015

By Steve Blumenthal

“Now look at them yo-yo’s that’s the way you do it

You play the guitar on the M.T.V.

That ain’t workin’ that’s the way you do it

Money for nothin’ and your chicks for free.”

Money For Nothing – Dire Straits

The Fed is sitting between a “rock and a hard place”. A recent Bloomberg survey sees a 50% chance the Fed will lift rates in September. Oh, the consequences. Increasing U.S. interest rates further increases the valuation proposition of Treasurys vs. Bunds, Japanese Bonds and just about every other developed country debt. Further advantage to the U.S. dollar and significant disadvantage to the $9 trillion in U.S. dollars denominating Emerging Market debt. That amount owed goes higher with the dollar and we think Greece and Puerto Rico are issues.

Today I highlight two great letters. One from Lacy Hunt and the other from Bill Gross.

“The excessive debt burden, slow money growth, declining money velocity, the Wicksell effect and the high real rate of interest indicate that the fundamental elements are exerting downward, rather than upward, pressure on inflation.” Lacy Hunt

Fed officials themselves predict that the Fed funds rate will rise to 1.625% by the end of 2016. Hunt concludes interest rates are heading lower thus hold onto your long-term Treasury bond exposure.

Gross argues that the Fed’s low rate policy is a large part of the problem. There is much to gain from both Hunt and Gross’s viewpoints.

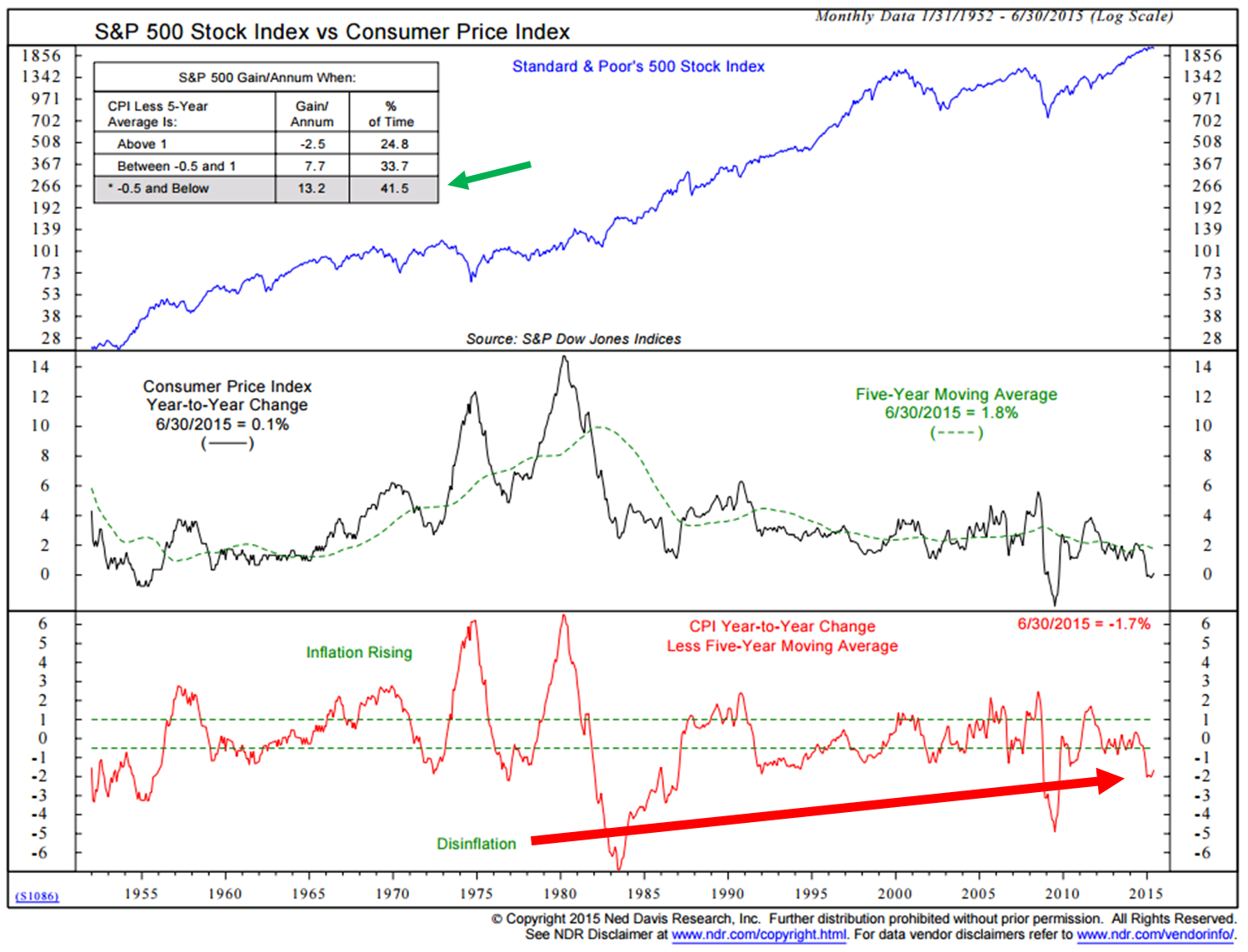

The battle today is one of inflation vs. deflation. The global central bankers are independently and collectively trying to drive inflation higher. So far, as we’ll see in the next chart, they are losing that battle (bottom red arrow).

Put me in the 50/50 camp for a September rate increase. The Fed wants to get off the zero bound peg but the risks are many. Getting to 1.625% in 2016 or even less will come with consequence. More from Hunt:

“The predicament the Fed is in is one that could be anticipated based on the work of the late Robert K. Merton (1910-2003). Considered by many to be the father of modern day sociology, he was awarded the National Medal of Science in 1994 and authored many outstanding books and articles. He is best known for popularizing, if not coining, the term “unanticipated consequences” in a 1936 article. He also developed the “theory of the middle range”, which says undertaking a completely new policy should proceed in small steps in case significant unintended problems arise. As the Fed’s grand scale experimental policies illustrate, anticipating unintended consequences of untested policies is an impossible task. For that reason policy should be limited to conventional methods with known outcomes or by untested operations only when taken in small and easily reversible increments.”

Untested operations only when taken in small and easily reversible increments. Global QE has been extraordinarily massive. Small and easily reversible? No way.

Money Ain’t for Nothin’ Get Your Fed for Free. Between a Rock and a Hard Place – indeed.

I link to these two great pieces below and conclude with a few short thoughts and, most importantly, a wish for you to slow down, detox from work and find a nice place this August to escape to.

Included in this week’s On My Radar:

- Lacy Hunt – Misperceptions Create Significant Bond Market Value

- Bill Gross – Say A Little Prayer

- Trade Signals – Watching Out for Minus 2

Lacy Hunt – Misperceptions Create Significant Bond Market Value

Here are a few highlights:

- Lacy ultimately believes that the yield on the 30-year bond will move much lower.

- He notes: From the cyclical monthly high in interest rates in the 1990-91 recession through June of this year, the 30-year Treasury bond yield has dropped from 9% to 3%. This massive decline in long rates was hardly smooth with nine significant backups. In these nine cases, yields rose an average of 127 basis points, with the range from about 200 basis points to 60 basis points (Chart 1).

- The recent move from the monthly low in February has been modest by comparison. Importantly, this powerful 6 percentage point downward move in long-term Treasury rates was nearly identical to the decline in the rate of inflation as measured by the monthly year-over-year change in the Consumer Price Index which moved from just over 6% in 1990 to 0% today. Therefore, it was the backdrop of shifting inflationary circumstances that once again determined the trend in long-term Treasury bond yields.

- In almost all cases, including the most recent Quarterly Review and Outlook Second Quarter 2015 rise, the intermittent change in psychology that drove interest rates higher in the short run, occurred despite weakening inflation. There was, however, always a strong sentiment that the rise marked the end of the bull market and a major trend reversal was taking place. This is also the case today.

- Lacy sites four misperceptions have pushed Treasury bond yields to levels that represent significant value for long-term investors. These are: 1. The recent downturn in economic activity will give way to improving conditions and even higher bond yields. 2. Intensifying cost pressures will lead to higher inflation/yields. 3. The inevitable normalization of the Fed funds rate will work its way up along the yield curve causing long rates to rise. 4. The bond market is in a bubble, and like all manias, it will eventually burst.

- He dispels all four.

- Most interesting to me was the following: The expectation of lower long rates is also bolstered by the well-vetted economic theory of “the Wicksell effect” (Knut Wicksell 1851-1926).

- Wicksell suggested that when the market rate of interest exceeds the natural rate of interest, funds are drained from income and spending to pay the financial obligations of debtors. Contrarily, these same monetary conditions support economic growth when the market rate of interest is below the natural rate of interest as funds flow from financial obligations into spending and income. The market rate of interest and the natural rate of interest must be very broad in order to capture the activities of all market participants. The Baa corporate bond yield, which is a proxy for a middle range borrowing risk, serves the purpose of reflecting the overall market rate of interest. The natural rate of interest can be captured by the broadest of all economic indicators, the growth rate of nominal GDP.

- In comparing these key rates, it is evident that the Wicksell effect has become more of a constraint on growth this year. For instance, the Baa corporate bond yield averaged about 4.9% in the second quarter. This is a full 230 basis points greater than the gain in nominal GDP expected by the Fed for 2015. By comparison, the Baa yield was only 70 basis points above the year-over-year percent increase in nominal GDP in the first quarter.

- To explain the adverse impact on the economy today of a 4.8% Baa rate verses a nominal GDP growth rate of 2.6%, consider a $1 million investment financed by an equal amount of debt. The investment provides income of $26,000 a year (growth rate of nominal GDP), but the debt servicing (i.e. the interest on Baa credit) is $48,000. This amounts to a drain of $22,000 per million. Historically, the $1 million investment would, on average, add $2,500 to the annual income spending stream. Over the past eight decades, the Wicksell spread averaged a negative 25 basis points (Chart 3).

- Since 2007, however, the market rate of interest has been persistently above the natural rate and we have experienced an extended period of subpar economic performance. Also, during these eight years, the economy has been overloaded with debt as a percent of GDP and, unfortunately, too much of the wrong type of debt. The ratio of public and private debt moved even higher over the past six months suggesting that the Wicksell effect is likely to continue enfeebling monetary policy and restraining economic growth and inflation.

- In summary, economic theory and history do not suggest the secular low in inflation, or that its alter ego, Treasury bond yields, is at hand. The excessive debt burden, slow money growth, declining money velocity, the Wicksell effect and the high real rate of interest indicate that the fundamental elements are exerting downward, rather than upward, pressure on inflation. Inflation will not trough as long as the U.S. economy continues to become even more indebted. While Treasury bond yields have repeatedly shown the ability to rise in response to a multitude of short-run concerns that fade in and out of the bond market on a regular basis, the secular low in Treasury bond yields is not likely to occur until inflation troughs and real yields are well below long-run mean values. We, therefore, continue to comfortably hold our long-held position in long-term Treasury securities.

Here is a look at the declining money velocity Hunt mentioned: The velocity of money has fallen off a cliff.

No signs of inflation. Deflation is winning for now. Click here for the full piece.

Bill Gross – Say A Little Prayer

Here are a few highlights:

- Speaking of bumpy air, trespassing, and the forgiveness of debt, the Greek/German tragedy of mid-summer seems to have landed on terra firma for at least a few months, although inevitably the weakness of the Eurozone with its common currency, but disparate fiscal philosophies, spells renewed turbulence in financial asset markets. The Eurozone – and the Eurounion itself as Britain’s 2017 referendum may eventually reveal – is a dysfunctional family and may always be. Examples: 1) Germany vs. France; 2) the Balkans; 3) Southern peripherals; and 4) the more stoic Nordic countries. They are all so different that a common purpose seems to be missing. Perhaps that purpose is summed up in three words “Peace and Prosperity” but while the peace seems to be assured by German passivity and the military blanket of NATO, prosperity is a subject of conflicting views as to which policies lead to long-term growth.

- Draghi’s ECB and the Merkel controlled EZ ascribe to the old theory of “Feed a fever, starve a cold” – the “fever” in this case being financial bull markets fed with 0% credit, and the “cold” being fiscal austerity starved by balanced budgets. So far, the philosophy seems to be working well for Germany, miserably for Greece, and not so well for all other EZ countries in between.

- But these conflicting views as to how to treat a fever or cure a cold are global in scope.

- Japan appears to be feeding both monetary and fiscal maladies with its persistent QE and substantial budget deficits, yet has little to show for it in terms of either inflation or real growth.

- China seems to resemble a desperate patient, changing doctors and proposed remedies every other month or so. First, it feeds the Shenzhen market fever, allowing it to “double bubble” in the first six months of 2015, then authorities starve it by “inactivating” two thirds of market listed shares and then eventually create financial SOEs (state owned enterprises) to buy billions of stocks to bail out naïve first time investors and ultimately its own economy.

- But, because it is the finance system’s global locomotive, it is the United States where this debate seems to be most critical, and where it subtly seems to be changing. It is not the fiscal stance that appears to be morphing, however. Republican “tax cut” orthodoxy will likely dominate for at least another few years.

- It’smonetary policy where the battleground for evolutionary ideas is taking place as the Fed begins to recognize that zero percent interest rates increasingly have negative, as well as, positive consequences. Historically, the Fed and almost all other central banks have comfortably relied on a model which assumes that lower and lower yields will stimulate not only asset prices but investment spending in the real economy.

- With financial assets, the logic is straightforward: higher bond prices and stock P/Es almost axiomatically elevate markets, although the assumed trickle-down effect leading to higher real wages has not followed suit. In the real economy, it seemed almost straightforward as well: if a central bank could lower the cost of debt and equity closer and closer to zero, then inevitably the private sector would take the bait – investing in cheap plant + equipment, technology, innovation – you name it. “Money for nothing – get your chicks for free”, I suppose. But no. Not so.

- There is no statistical reason per se for the Fed to raise interest rates, yet absent a major global catastrophe, we are likely to get one in September. But the reason will not be the risk of rising inflation, nor the continued downward push of unemployment to 5%. The reason will be that the central bankers that are charged with leading the global financial markets – the Fed and the BOE for now – are wising up; that the Taylor rule and any other standard signal of monetary policy must now be discarded into the trash bin of history.Low interest rates are not the cure – they are part of the problem. Say a little prayer that the BIS, yours truly, and a growing cast of contrarians, such as Jim Bianco and CNBC’s Rick Santelli, can convince the establishment that their world has changed.

The global central banks have taken unconventionally large steps (not small). Come on folks – this is not normal. “Say a Little Prayer” is a relatively short read and written with Bill’s dry wit and good humor.

Click here for the full piece.

Trade Signals – Watching Out for Minus 2

The aged cyclical bull market up trend remains in place; however, fewer stocks are holding the market up. Our favorite Trend Model, Big Mo, is in decline but continues to favor stock exposure.

As for bonds, the Zweig Bond Model remains in a “buy” signal – bullish on long-term bond exposure. High yield bonds are a different story. They look shaken and for now the trend is lower. Our CMG Managed High Yield Bond Program remains on a “sell” signal but prices appear to be stabilizing.

I believe it is “All About That Fed”. Each week I post the Don’t Fight The Tape or The Fed indicator. The markets do best when the Fed is supportive. The current reading remains at -1. The market has not performed well historically when that indictor reached -1. But it is a -2 reading that we really have to watch out for.

For now, stay patient, risk focused and tactical. Overall, risk remains high. Let’s keep watching out for minus 2.

A quick updated summary of the various charts on Trade Signals:

- Cyclical Equity Market Trend: The Primary Trend Remains Bullish for Stocks

- Volume Supply is Greater than Volume Demand: Sell Signalfor Stocks

- Weekly Investor Sentiment Indicator:

- NDR Crowd Sentiment Poll: Extreme Pessimism (short-term Bullishfor stocks)

- Daily Trading Sentiment Composite: Extreme Pessimism (short-term Bullishfor stocks)

- Don’t Fight the Tape or the Fed: Modestly Bearish – Watch Out for Minus Two

- U.S. Recession Watch – My Favorite U.S. Recession Forecasting Chart: Currently signaling No U.S. Recession

- The Zweig Bond Model: The Cyclical Trend for Bonds is Bullish

Click here for the link to all of the charts.

A few concluding thoughts:

Oftentimes emotion seeps into investment decision making. That is mostly not a good thing. The point I’d like to express is to remain mindful of the elevated risks. Consider various hedging techniques and allocate to a handful of non-correlating tactical strategies. Send me a note if you’d like to learn more.

The cyclical equity bull market is overvalued and aged. Recently, a long-time client called wanting to invest in dividend paying stocks convinced that now is the best time to get in. He missed the move. We’ve seen this show before (2000 and 2007/08) – experience whispers a warning in my ear.

Debts a drag and so are the unmanageable entitlement programs. Cut the debt, decrease the promises are tough choices to make. Alternatively, expect higher taxes. All of this is a drag on growth. Put me in Lacy Hunt’s camp.

However, put me in the Fed will raise rates in September – not because of the economic evidence but because the Fed is desperately trying to get off the zero peg. At least to test the waters. I believe they will ultimately drop rates back down again in the not too distant future.

Deflation is winning but this is a confusing game with many moving parts. It may be we get both deflation, declining short-term rates and rising long-term rates. I envision sovereign debt and junk bond crises that re-prices risk (interest rates move higher). QE4 is in our future.

There is little value today in overpriced equities – forward returns in the low single digits over the next ten years. But the next ten months? Who knows? There is also little value in bonds – forward returns in the low single digits. The equity bull market may grow to become more overvalued and more aged.

We need to help our clients see the risk. That whisper of experience. The logic of valuations and likely returns. Fortunately, you and I can set in place a strategy that allows us to both participate and protect.

For now, hedge that equity exposure, broaden exposure to include alternative trading strategies, overweight tactically managed strategies and tactically trade that bond exposure. We can shift back to overweight equities when valuations and forward returns offer better reward. On the other side of the next crisis is one super great buying opportunity. We are not there yet.

Personal note:

Some down time is in my near future. A long weekend is ahead. Susan’s brother has an amazing house in Lake George, New York. We are loading our gang of eight into a few cars and heading up for a visit this weekend. Susan’s mother will be there. It is nice to watch the close relationship she shares with her family. The cousins will be manning the water ski boat. We call it Camp Jim. I can’t wait for the happy hours and dinner time when we all come together.

Wishing you the very best and time spent with those you love most!

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman, CEO and CIO. Steve authors a free weekly e-letter titled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.

»