This article has not been updated since 2015 besides this editors note telling you to check out recent SEC charges

Original article intact can be found below

$RIOT’s Chairman and CEO John O’Rourke has resigned following the SEC’s allegations of securities fraud filed on Fridayhttps://t.co/YRjA6Fnbp3

— Hindenburg Research (@HindenburgRes) September 8, 2018

Proud day here. We’ve been early in covering multiple schemes run by Honig & individuals charged today, including $OPK $PGLC $RIOT & $MARA

Props to @sharesleuth & @buhlreports for their leading work on this subject as well

Relatedly, we have a special treat for you on Monday…

— Hindenburg Research (@HindenburgRes) September 7, 2018

Note that an unsealed DoJ plea agreement in a related securities fraud case named Honig as well.

Given the scope of these SEC charges and given the DoJ’s known investigation we expect criminal charges are next. (h/t @buhlreports)$OPK $RIOT $COOL $PGLChttps://t.co/B2c31U2ggh

— Hindenburg Research (@HindenburgRes) September 7, 2018

WOW the SEC just filed a massive, far-reaching complaint against Phil Frost, Barry Honig, Opko Health, and numerous related entities. $OPK $RIOT $MARA $COOLhttps://t.co/HLllY3SUG4

— Hindenburg Research (@HindenburgRes) September 7, 2018

IDI: Strong Sell On Fraud Lawsuits, Bankruptcy And Technology Failure, -92.4% Downside by The Pump Stopper

Summary

- Frost mixed up with “the wrong crowd” as Barry Honig and Michael Brauser have spun a tiny struggling debt collections business, acquired with $5.7m cash, into temporarily inflated ~$200m shell.

- Chairman Brauser’s biography has “interesting” omissions including bankruptcy, wipeout, and fraud lawsuits, with Equifax suing him alleging “fraudulent misrepresentations” with Softbank lawsuit alleging “various frauds”.

- IDI stock temporarily inflated from extensive Yahoo message board stock-pumping scheme, touting IDI across dozens of boards with interconnected aliases, similar to halted and bankrupt FNRG.

- IDI’s Transunion lawsuit could mean instant $0 for stock as IDI future apparently based on IP they don’t own, which Transunion acquired when IDI CSO Poulsen’s last company went bankrupt.

- Confluence of temporary factors above have inflated IDI stock to the obviously unsustainable valuation of ~$200m or >40x revenue, creating imminent -92.4% downside in “best case” scenario.

I believe Idi Inc. (NYSEMKT:IDI) is another worthless Brauser and Honig wipeout. This famous wipeout team has joined forces to temporarily resuscitate a fraud ridden shell with a tiny debt collections firm, acquired with $5.7m cash payment, to the unsustainable valuation of $200m or >40x revenue. In what appears a desperate attempt to salvage his failed fraud shell, Frost has clearly gotten involved with the “wrong crowd” and regrettably stained his reputation through association with one of the worst penny stock wipeout teams in America.

Brauser’s biography conveniently “forgets” to include a long track record of fraud lawsuits, bankruptcy and shareholder wipeouts. While touting involvement in Naviant, Brauser neglects to mention he was apparently sued by data fusion giant Equifax (NYSE:EFX) for “fictitious receivables” and by Softbank for “various frauds” with apparent multimillion dollar payments to Equifax. Shockingly, the Naviant debacle barely scratches the surface and Barry Honig’s background looks even worse.

(picture credit IDI)

IDI faces an insurmountable lawsuit while desperate for cash and with a $160m equity shelf filed IDI stock is now “coincidentally” being pumped with an apparent sketchy online Yahoo message board stock promotion campaign, similar to halted and bankrupt Forcefield Energy (NASDAQ:FNRG) where the chairman was arrested for fraud.

IDI is eerily similar to the BVSN, VNRG, USEL, IZEA and DRNE wipeouts thiese people oversaw, With a huge amount of IDI shares becoming unlocked soon, a $160m shelf filed for IDI stock sales and an abusive $31m+ free payment to Brauser and Honig, IDI is at imminent risk of total wipeout.

It’s not often you get to short a cash burning penny stock wipeout team with a declining, $5.7m cash acquisition trading at >40x revenue for <7% cost to borrow. I recommend you pour yourself a tall glass of Gilby’s vodka and sit down as what you read will be shocking….

“Interactive Data” A Tiny, Struggling Debt Collections Business With $0 R&D Spending, Bought With $5.7m Cash

Now that IDI has officially announced they are winding down the China billboard business with huge write offs, 100% of IDI’s ongoing business will be “Interactive Data, LLC”. I think IDI investors are confused and don’t understand what this business actually is.

“Interactive Data, LLC” is the business IDI is pinning their “data fusion!” hype-story on, which IDI just acquired last year with a $5.7m cash payment.

Strip away the hype, we see “Interactive Data, LLC” is a tiny firm with just 9 full time employees founded in 2001. Based in Georgia, Interactive Data seems focused on providing contact information verification to the debt collection business. When a debt collector calls a defaulted creditor, they are not allowed to harass people with similar names and face severe lawsuits if they make that mistake. Therefore, debt collections agencies pay tiny amounts for some very basic offerings which allow them to be sure they are tracking down the correct person.

(picture credit)

The contact verification business is a brutally competitive business where, over the years, Interactive Data finds itself facing larger, superior competitors with cheaper, better products and dominant sales teams. Due to this, Interactive Data has struggled and been apparently forced to hire outside sales consultants and, based on their transactional pricing model, chase after the smallest and least profitable customers in the industry. Interactive Data isn’t even a real technology company anyway because this tiny business seems to have been built largely by acquisition with no R&D in 2012, 2013 and apparently 2014 as well.

We can see Interactive Data’s financial struggling below in the only clear Interactive Data financials I could find, available here.

(click to enlarge)

(picture credit IDI inc filings)

We can see Interactive Data’s 2014 revenue declined -7% versus last year while gross profit fell -18.5%. Also interesting: Interactive Data claims to have spent zero on R&D in most of 2014, 2013 and 2012 and even with this expense at $0 and without public company expenses or any of the other SG&A Brauser/Honig/etc are layering on this tiny failure, it only generated a ~$474k in profit, which also declined -34.8% from the previous year.

Considering IDI has already opened multiple branches in FL and WA with 8+ engineers and the typical >$400k of annual cash cost just to be a public company, I estimate IDI’s cash burn in the future will be at least -$2m per quarter. Perhaps this is why none of IDI inc’s press releases include the financials of this tiny struggling “business” they just acquired? Clearly the above “business” is worth nothing vaguely close to IDI’s current ~$200m market cap. Recall that there is nothing else here. The only aspect to IDI’s business is this tiny, marginally profitable and extremely competitive company. That’s it.

So what are Brauser and Honig doing with a fraud ridden shell and this tiny struggling debt collection firm? Let us dig deeper to understand what is truly going on here….

Brauser’s “Selective” Disclosures = Fraud Lawsuits, Bankruptcy and Wipeout

As a reminder, Michael Brauser, Barry Honig and their investment vehicle Marlin are clearly the financial architects of IDI to me and I don’t see how IDI would even exist without them.

Michael Brauser: History of Fraud Lawsuits, Bankruptcy and Wipeout

Picture credit IDI inc

Brauser seems to “selectively” tout his background, picking and choosing certain companies while failing to transparently disclose lawsuits around his involvement with other companies. A large number of these undisclosed companies wiped out big piles of retail shareholders.

Naviant = Fraud Allegations

(picture credit Naviant)

For instance, Brauser touts his “Naviant” track record sale with Equifax in his biography. What seems to have been forgotten though is he was apparently sued by Equifax for fraud allegations over that transaction and apparently saw millions of dollars go to Equifax as a result. This amazing lawsuit alleges Brauser “participated in the fraudulent creation of fictitious receivables and further participated in accounting overstatments that disguised Naviant’s true financial condition” going on to allege further:

“maintained one set of book for Naviant that was more accurate and complete and another that omitted the low-priced e-mail transaction, which Naviant provided to Equifax and it’s accountants during merger negotiations.”

Shareholder Softbank also sued, claiming

“Defendant Michael Brauser had been “intimately involved in carrying out various frauds at Naviant and covering up their misdeeds through threats and intimidation.” Softbank also claims that Defendant Michael Brauser represented to Softbank that he was ‘judgment proof’ as a result of transferring away all of his personal assets, with the exception of his Bentley automobile and personal computer”

While the Equifax fraud allegations seem to have resulted in big cash payments it’s not clear to me how the Softbank suit ended. Unfortunately though it appears this Naviant mess is just the tip of the iceberg…

Biozone: “this is not even investment – it is stealing“

Brauser was again sued (with Honig, etc) in a case involving Biozone Pharmaceutical including (emphasis mine):

“an illegal scheme by a group of predatory investors utilizing facially despicable methods”

And goes on to explain that, in addition to allegations involving violations of federal securities laws:

“this group of investors misled Plaintiff Fisher through aninvestment scheme designed to divest Plaintiff of all the economic rights and goodwill be had built through his company over the course of the previous 22 years”

“the defendants (Brauser, Honig, etc) immediate financial motivation in taking a legitimate economic contributor is to turn it into an investment vehicle in which they will pump up the stock price, and then proceed to sell off the shares, without regard to the well being of the business.”

“violating the Racketeer Influenced and Corrupt Organizations Act for engaging in a pattern of similar behavior against other companies.”

This lawsuit is remarkable, and I strongly encourage you read it. This case seems to have also been shuffled around so it’s not clear what the ultimate resolution was for poor Daniel Fisher. However with all the Honig, Brauser, etc lawsuits, I would strongly recommend everyone read all the legal background documents to make sure you truly understand what you are getting yourself into with these people.

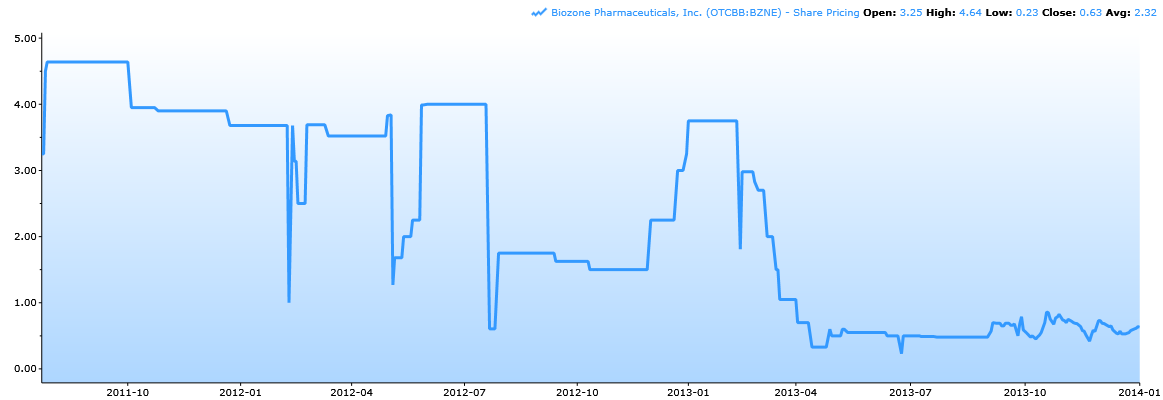

Unsurprisingly, Biozone seems to have been a wipeout for original investors as the stock imploded -80.62% over the time frame below and was sued for “breach of fiduciary duty” after basically all of Biozone’s important assets were transferred to another Honig/Brauser company. I remind you that Frost was also somehow convinced to invest in this mess too.

(click to enlarge)

The List Goes On: Even MOAR Alleged “Misrepresentations” and Bankruptcy

Brauser was sued again 1/30/2009 for fraud in Kast vs. The Tube Media Corp (09-06285) a publicly traded company that apparently also failed, was delisted and seems to have ceased operations 10/2007. Allegations included “filing materially false and misleading financial reports, and intentionally making misrepresentations of material facts”. Also not discussed in Brauser’s biography was the apparent bankruptcy of FL Telephone Co or that Brauser was sued in an adversary proceeding related to that bankruptcy. Murky situations abound with further allegations of improper side deals and Brauser potentially plotting to violate FL law through undisclosed $1m commission payments. Despite all these red flags, retail investors seem to fall for the “Brauser and Honig Show!” over and over again, as yet another lawsuit here against Brauser (as chairman of Sendtec) alleges “violations of securities laws”. While some of these lawsuits seem to have resulted in cash payments like Equifax, other lawsuits seem to have eventually been dismissed or possibly settled, so I recommend you read these legal documents yourself to gain the full picture. Regardless though, investing with anyone who has repeatedly faced such serious allegations clearly warrants extreme caution.

Furthermore, just because you invest in a company and own shares of equity does not make you a “founder” as much as you’d like. If I own Coca Kola (NYSE:KO) stock for years that doesn’t mean I’m a “founder” and even if I sit in on four phone calls per year with the board that obviously doesn’t mean I “built the business!” either. Confused retail stock investors like to tout “but he sold Interclick!”. While ignoring the fact that being on the board is a passive role merely requiring a few meetings a year, ICLK traded at $12.98 before it was eventually sold for $9. That means many shareholders took a severe loss and the company was actually sold at a discount to where it had traded previously.

Interclick: “sometimes even when you win….you lose”

(click to enlarge)

Brauser seems to love to tout that he was on the board of InterClick when it was sold to yahoo (NASDAQ:YHOO).

As you see above though, before Yahoo stepped into salvage this mess, InterClick was ALSO on its way to being another wipeout. Even with Yahoo buying the company at a premium (and the deal apparently failing later on), the takeout price was still -30% from where it had traded previously. So I see that even in the blind chance Brauser accidentally doesn’t wipe a company out or get sued with fraud allegations, in the biggest success of his whole life, many shareholders STILL lost a substantial part of their investment.

For Brauser’s more recent forays into stocks, as well as virtually everything he touches, bad things happen to retail investors…..

The Honig & Brauser “PlayBook”: Frost’s Name Thrown Around, Then Shareholders Get Wiped Out

Unsophisticated retail investors seem to think Frost’s name on a filing means an investment is a sure thing, ignoring the fact that Frost is ~80 years old and has money in dozens and dozens of investments. Unfortunately, it seems the financial contamination of Honig and Brauser involvement more than overwhelms any limited positive benefit from a claimed Frost connection. Best I can tell the end result is shareholder wipeout, lawsuits or bankruptcy in almost every instance.

It seems to me Frost has gotten mixed up with the wrong guys, and while investing in a company that only Frost is involved in may be worth considering, the moment Honig or Brauser pop up you should basically just light your wallet on fire and get it over with.

With so many people involved in the following wipeouts, the time frames are messy. As a result the % decline estimates and charts in this report are all my best estimate of the best time frame to represent the impact of these people on the companies in question.

Aside from IDI inc where Tiger Media was already found to involve fraud, there are countless examples. Like VPCO where Frost name was again touted with absurdly promotional articles while Brauser and Honig were also involved and apparently Scott Frohman, who seems to have some past tie to Brauser’s much-touted Seisant (also with some very questionable stuff going on) was also involved. None of that mattered though as Vapor Corp (NASDAQ:VPCO), and the 65%+ retail shareholder based, have experienced a -93.43% disaster (so far).

(click to enlarge)

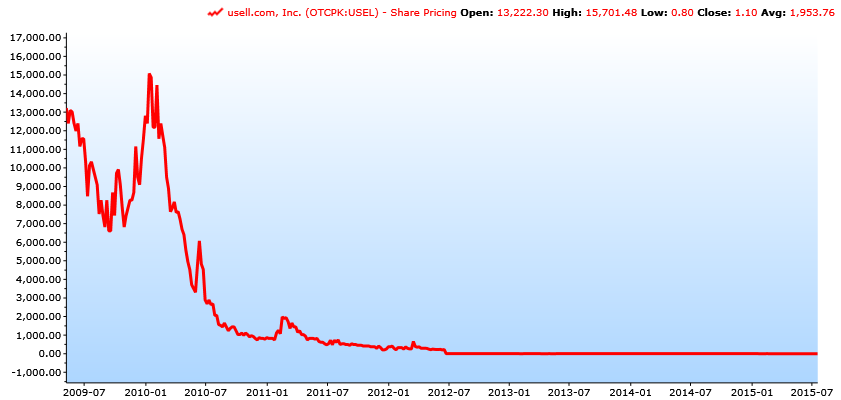

And uSell.com which seems to have had Honig, Brauser with current IDI board members Peter T. Benz and IDI director Daniel Brauser (uSell.com’s CEO) all involved. Despite promotional SeekingAlpha articles and Frost’s public involvement, it essentially went straight to $0, falling -99.91% and wiping out anyone unfortunate enough to have invested.

(click to enlarge)

(click to enlarge)

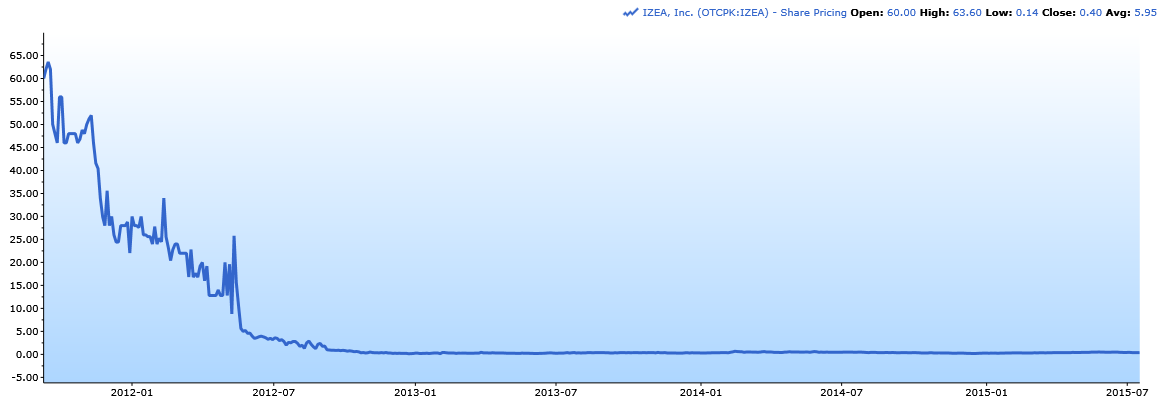

Frost’s name was again touted with promotional articles from curious authors about IZEA. Barry Honig and Brauser were also involved and (with a ~40%+ retail shareholders base) now sports a $23m market cap as OTC listed Izea, inc (OTCQB:IZEA), which has been a disaster for everyone over any time frame with -99.35 wipeout.

(click to enlarge)

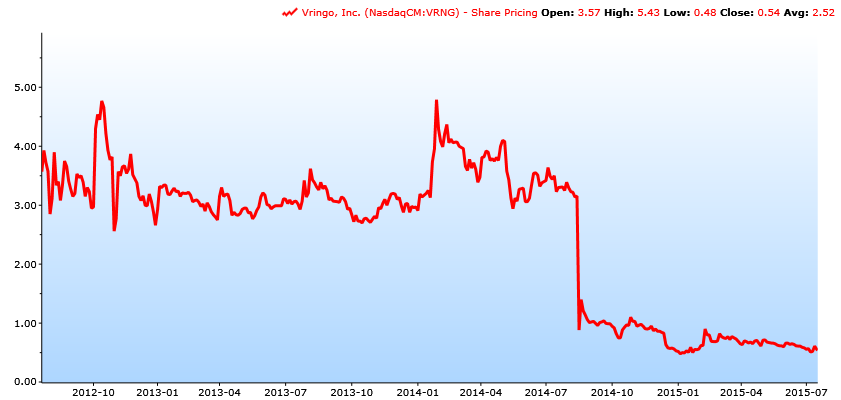

Or Vringo (NASDAQ:VRNG) which had Frost, Brauser and Honig all involved but apparently Honig/Brauser again offset even Frost’s genius as the ~79% retail shareholder based “enjoyed” a quick -84.87% decline with no recovery.

(click to enlarge)

These people have done this over and over again. How about Document Security Systems (NYSEMKT:DSS), which I estimate has ~80% retail shareholders, who have also “enjoyed” a quick -82.73% wipeout?

(click to enlarge)

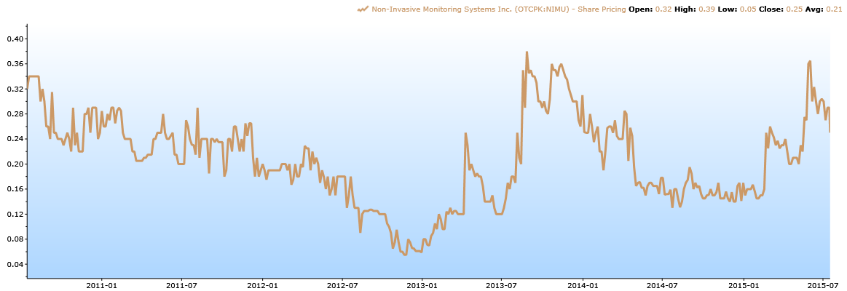

Frost has been involved in plenty of wipeouts so the list goes on, like Non-Invasive Monitoring Systems, inc (OTCPK:NIMU) where frost was involved and the ~57% retail shareholder base “only” lost -22% (so far – be patient)

(click to enlarge)

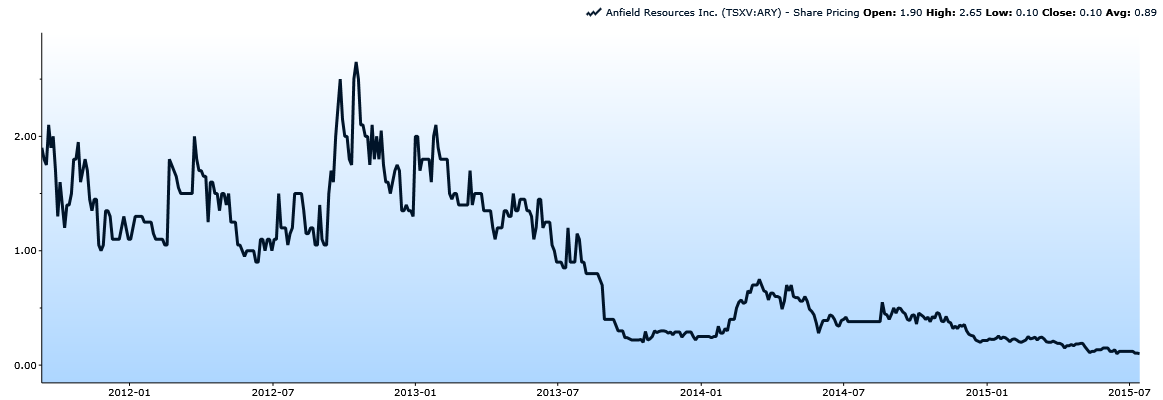

Or Anfield Resources: -94.74% Wipeout

(click to enlarge)

Or MSLP where shareholders have had a volatile ride to a -64.28% loss

(click to enlarge)

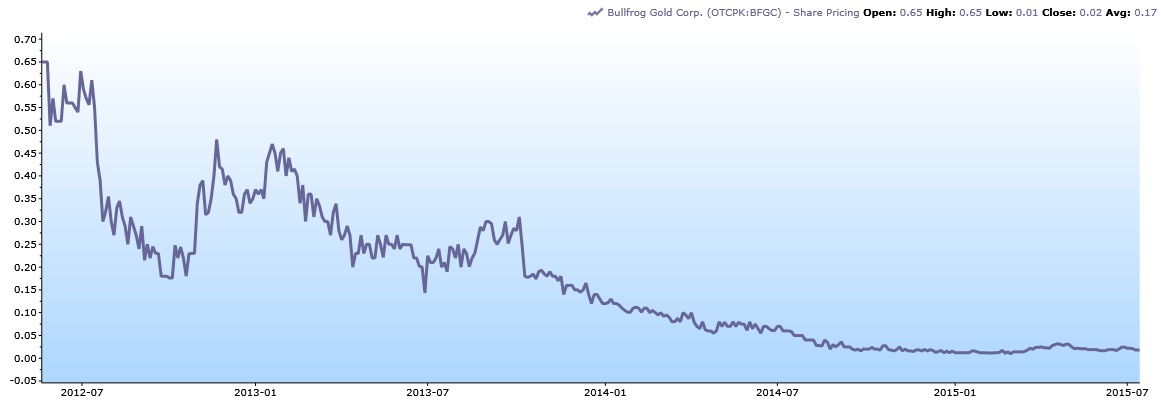

Or Bullfrog (OTCQB:BFGC) which, with a ~79% retail shareholder base, seems on it’s way to $0.00 with a -97.38% decline already

(click to enlarge)

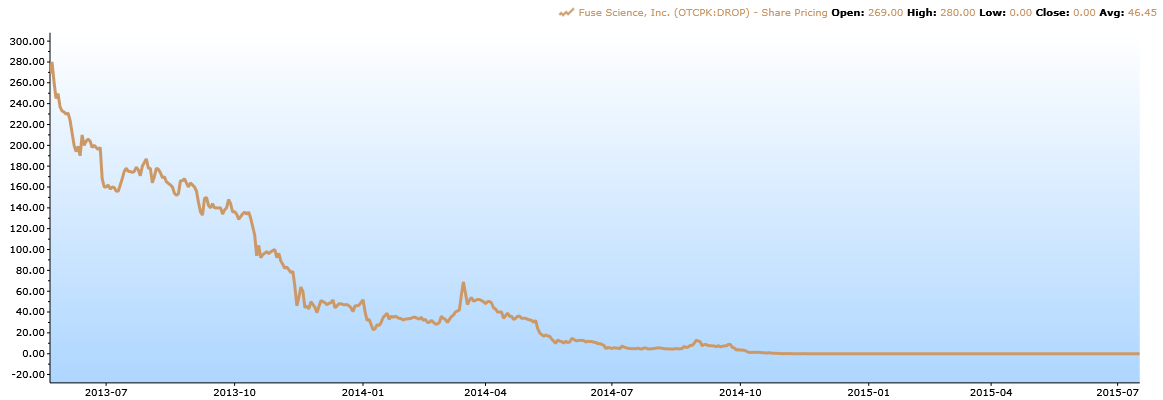

Or Fuse Sciences (OTCPK:DROP) which Honig and Brauser seem to have convinced Frost to invest in (unfortunately) through MSLP in 2013. This seems to have gone to $0 with a -100% decline showing

(click to enlarge)

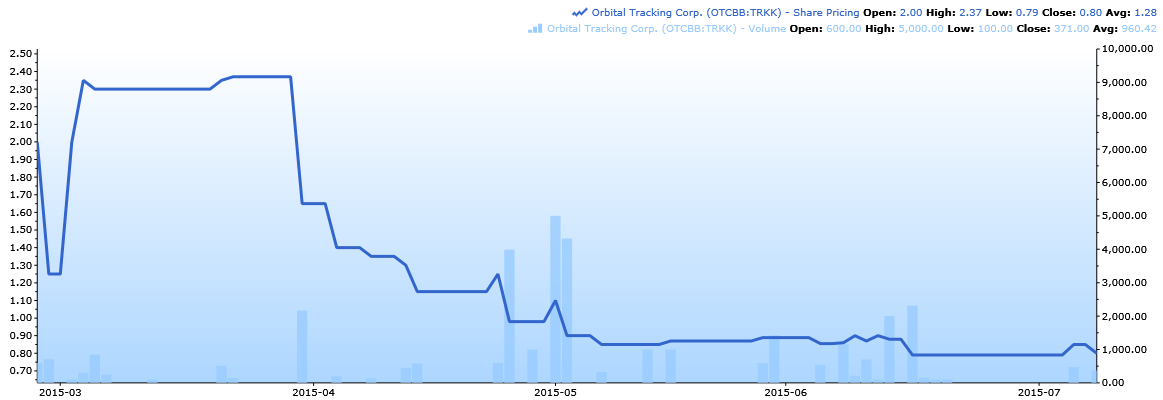

Or perhaps Silver Horn Mining with Brauser, Honig and Frost all involvedwhich then seems to have become GWSTT and then TRKK but…. basically wiped everyone out on the way to an $8m market cap with (another) swift -61% decline.

(click to enlarge)

Drone aviation (OTCQB:DRNE) is another good and recent example where Frost’s name was touted, the notorious RedChip was then apparently paid hundreds of thousands of trading shares and cash for their promotion along with current IDI board member Steven Rubin involvement. DRNE has an absolutely egregious 97% retail shareholder base, who have now been wiped out with a -78.42% decline so far

(click to enlarge)

Michael Brauser Parties With “Nelly”, Retail Shareholders Get Wiped Out

Picture credit

As long-term readers of mine know, I am a huge Nelly fan. For those of you who don’t click the links in my articles, you should. That said though, I like oldies too. So n that note, I would like to dedicate a songto the Honig-Brauser Gang.

Picture Credit

Quoting directly from the song’s lyrics: “Ha-ha-ha-ha-ha-ha-ha-ha-ha-ha-ha-ha-a, WIPEOUT!” There’s not much else to say about that…

Barry Honig: Lawsuits, Even More Wipeouts and “Curious” Promotional Stock Articles

In case the pages of horrific red flags above are not enough to cause concern, “coincidently” many Barry Honig names also seem to garner curiously promotional SeekingAlpha articles before the stock eventually gets wiped out. As outlined in Bleeker street’s impressive piece of research, there are many questionable ties between Barry Honig and promotional stock report authors.

Picture credit: Bleeker Street

Similar to Brauser, Honig has been named in lawsuits regarding everything from alleged violations of securities laws to situations involving “unjust enrichment“, alleged forgery and a “brutal beating” involving professional boxer Briggs and Honig’s Empire Sports. While I’m not sure what confidential settlements, lawsuit losses or wins may have resulted, the pattern here is clearly startling.

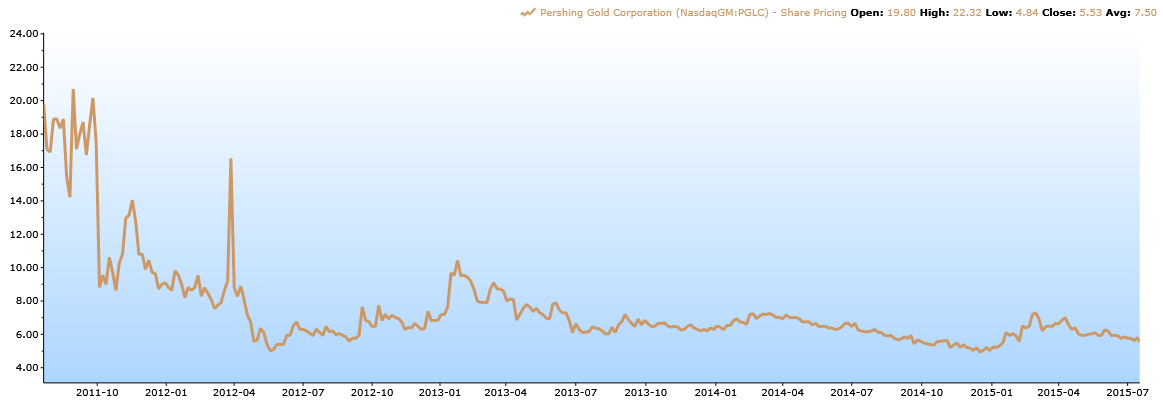

Don’t Let This Happen To You

Strangely, Honig’s boxing disaster Empire Sports seems to have ultimately became Sagebrush Gold (NASDAQ:SAGE) on 6/1/2011? And then, after announcing involvement of Dr. Phillip Frost, the company then changed name to Pershing Gold (NASDAQ:PGLC) in March 2012 and has been a total disaster for shareholders. Since these guys got involved, despite Frost involvement and lots of promotional SeekingAlpha articles by authors who disclose zero PGLC stock ownership, Pershing Gold Declined -72.07%

(click to enlarge)

Or this other Honig wipeout Spherix inc (NASDAQ:SPEX): -96.49% Decline

(click to enlarge)

As you can see, investing in anything with Brauser or Honig involved, even when Frost is named somewhere in the filings, is typically a total disaster for poor retail share(bag)holders. It’s not just Brauser and Honig though, IDI inc’s CSO Ole Poulsen, COO James Reilly and CEO Derek Dubner all seem to forget to include the fact that their last company TLO went bankrupt and nearly wiped out shareholders completely.

There are countless other Honig/Brauser disasters and I am getting tired of going through all their wipeouts. I think you get the point already, so in the interest of time I will pose one serious question: of all the Brauser/Honig/Marlin stocks in the market today, how many have market caps >$200m or generate >$2m in profit per year?

Given IDI true market cap is currently >$200m, this is a serious question.

If anyone can find a single current Brauser/Honig/Marlin stock with a $200m+ market cap or one consistently generating >$2m per year of profit, I will video tape myself personally singing you a song on YouTube. Not joking.

What’s in IDI for Brauser and Honig?! 2.5m FREE IDI Shares Worth Over $31m!

Now that you understand what is truly going on here, let’s look at how Honig and Brauser get rich in this scheme and why I believe they are involved.

The most egregious part of this whole IDI debacle to me are the crazy and, what I view as clearly abusive, contracts Honig and Brauser are mistreating IDI shareholders with via their Marlin vehicle. For example, regardless of how much dilutive equity it may take, what business is acquired or at what stock price, it seems to me Brauser/Honig/Marlin basically get 2m+ IDI shares essentially for free with some offensively low hurdles and loose terms set for their payday:

“The Marlin Consulting Agreement provides for equity compensation issued to Marlin in the amount of 10,000,000 Restricted Stock Units (“RSUs”), of TBO, which shall vest in four (4) equal, annual increments beginning October 13, 2015 and ending October 13, 2018, provided that one of the Milestones (as hereinafter defined) has been achieved on or before such date, and subject to Marlin Capital providing services on each applicable vesting date. As used in the Marlin Consulting Agreement, “Milestone” means: (NYSE:I) TBO generating $15 million in revenues over any 12 month period; or (ii) TBO generating $10 million in revenues over any 12 month period and generating positive earnings before interest, taxes, depreciation and amortization (with all stock based compensation not included as an expense) for such 12 month period. “

I would note there is a clear lack of any “per share” measurements and, shockingly, dilutive stock compensation to insiders is specifically excluded from this whole mess.

Even more offensive, Michael Brauser has apparently already received 500k shares of IDI stock rsu for what I view as basically nothing! I estimate this is worth >$1.25m today!

“On October 2, 2014, the Board of Directors approved the issuance of 500,000 RSUs to two consultants. One of the consultants to receive 500,000 RSUs is Michael Brauser,”

Even worse, it seems that part of this plan from the start was to get it all going with a ton of cheap stock given to their group at what I view as unreasonably favorable terms:

“On December 4, 2014, TBO sold 12,360,000 shares of TBO Common Stock to various investors at $0.50 per share on a “best efforts” basis for an aggregate of $6,094,338 in net proceeds after deducting discounts and expenses”

Whatever associates of the Brauser and Honig gang may have participated in this insane capital raise, they seem to have received $6.18m of IDI stock at split adjusted $2.50 per share right before a message board tout campaign started! What a coincidence! Now with IDI at $12.50 per share they are sitting on HUGE gain in a company that was just acquired with a $5.76m cash payment but now (temporarily) trades for a ~$200m valuation!!

(Picture credit)

So while primarily retail shareholders in IDI get led to their financial wipeout, Brauser, Honig and Marlin are set to get a free payday of $30m!?! How is that possibly seem fair?!

IDI Inc Partnered With “Palladium Capital Advisors, LLC”: Named Defendant in Madoff Lawsuit?!?

You can tell a lot about the quality of a stock or company by the quality of the investors it is able to attract. “Real” businesses, that honestly have a bright future, have no problem attracting high quality VC investors or other reputable financial partners while questionable shells on their way to wipeout often struggle and are forced to take “bottom tier” money at loan shark terms.

IDI inc lists “Palladium Capital Advisors” as a placement agent for TBO in 11/2014, who received warrant for 28k shares at $2.50 for their help in addition to $70k in cash. A quick Google on this curious financial partner apparently turns up a “Palladium Capital Advisors” as a named defendant in a Madoff Ponzi Lawsuit as recipients of “stolen customer property and other proceeds of the illegal scheme”.

It is not clear to me what happened here as the lawsuit is complex and long, so I’ll leave the reading on this to you, but if IDI was actually forced to partner with a named defendant allegedly involved in the Madoff Ponzi legal debacle, that is very scary stuff indeed.

“But Wait! You Also Get!” MOAR Lawsuits, Spam Email Pump & Dumps, and Shareholder Wipeouts.

While Honig and Brauser are apparently just the leaders of this crew, there are many others equally as bad. IDI director Peter T Benz seems to have been previously named in lawsuit (along with Bi-Coastal Consulting Group and Jonathan Lebed) alleging Fraud, Market Manipulation (stated halfway throug first paragraph), Unjust enrichment and Negligent Misrepresentations in the “Warning Management Services” case. Robert N. Fried was also sued at SearchMedia where he was co-chairman post-merger and CEO of Ideation. The lawsuit alleges “revenues had been massively overstated due to flagrant accounting irregularities” involving “fictitious business transactions“.

Interestingly IDI is also covered by Gilford Securities. Gilford also has a checkered past, including Gregg M Berger, former Gilford broker, who pled guilty and was jailed for involvement in “pump and dump schemes” apparently using spam emails involving thinly traded stocks to generate more than $30m of illegal proceeds. It also appears Gilford was fined $125k by FINRA recently for failing to disclose “the research analyst received compensation“.

Furthermore, it appears the SEC fined Gilford Securities $995k for failing to properly supervise the broker who served Vancouver Spam Promoter “John” Hui and the firm which allegedly facilitated a $33m pump and dump scheme. The SEC also went on to allege Gilford allowed employees to improperly execute customer orders without requisite trading licenses, and violating Regulation S-P by sharing nonpublic customer information with unauthorized third parties.

IDI Inc’s Message Board Stock Promotion Campaign: Similar to Disgraced, Halted and Bankrupt FNRG

How has IDI stock been temporarily pumped up to this obviously unsustainable valuation?

IDI is currently being supported by one of the most widespread and extensive online message board tout campaigns I have ever seen. As a reminder, FNRG experienced something similar (but far less egregious than IDI) before FNRG’s chairman was arrested for fraud and the company went bankrupt.

“The strategy for these posters is to seek out companies whose share price has risen strongly and which are getting a lot of attention. The posters then seek to draw readers’ attention to ForceField. Some small portion of the readers end up buying into ForceField, elevating share price and volume. Surprisingly, this strategy can work if there are thousands of postings to other high performing and high interest stocks.”

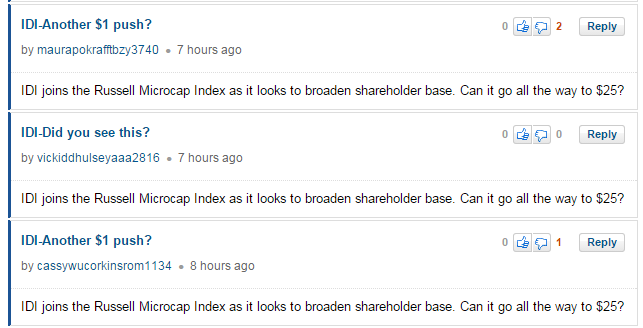

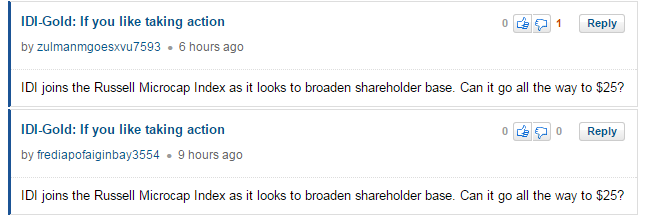

Similarly, on the Yahoo message boards for example, we see countless yahoo ID’s recently created which only tout IDI across the message boards in huge volume. Tellingly though their promotion campaign doesn’t take place on IDI’s board, presumably since anyone on the IDI board already knows about IDI stock and is not a useful target. I think the goal here is obvious: to lure in unsuspecting retail investors into IDI stock and temporarily inflate the stock price.

For example, we can see username “ermelindarqkabergerc3138? joined yahoo on 6/26/2015 and then immediately began posting comments across unrelated boards, often times literally within seconds of the last comment.

From yahoo message boards

Similar to FNRG touts posting on high traffic stocks, we see IDI touts posting repeatedly on the AliBaba message board, which clearly has zero to do with IDI.

A simple Google keyword search shows IDI touts flooding message boards with an apparent target of the highest trafficked and unrelated yahoo message boards including: Coca Cola , Kinder Morgan, iPath S&P500 VIX etn (NYSEARCA:VXX), EXTR, FITB, PLNR, CNET, LTRE, HUM, and BBY, among many others.

We can also see this tout campaign appears coordinated as we are seeing different aliases post identical promotional messages on IDI

(click to enlarge)

(click to enlarge)

Among the many IDI tout aliases I have found just on the Yahoo message boards include: “Ermelindarqkabergec3138“, “kennedyfettigovo“, “auroreparagasgql“, “kassikontoseta“, “euniceewelluip“, “fidelatimothycyd“, “dellamlcurtneruts4050“,arnettexvschiffelbeintqo2626 and likely many others.

To be clear, I am not certain exactly who the individuals are by name behind this shady online tout campaign (although I have my guesses). However, I don’t see how anyone would do this kind of extensive and premeditated work for free and typically stock promotion is not done without compensation.

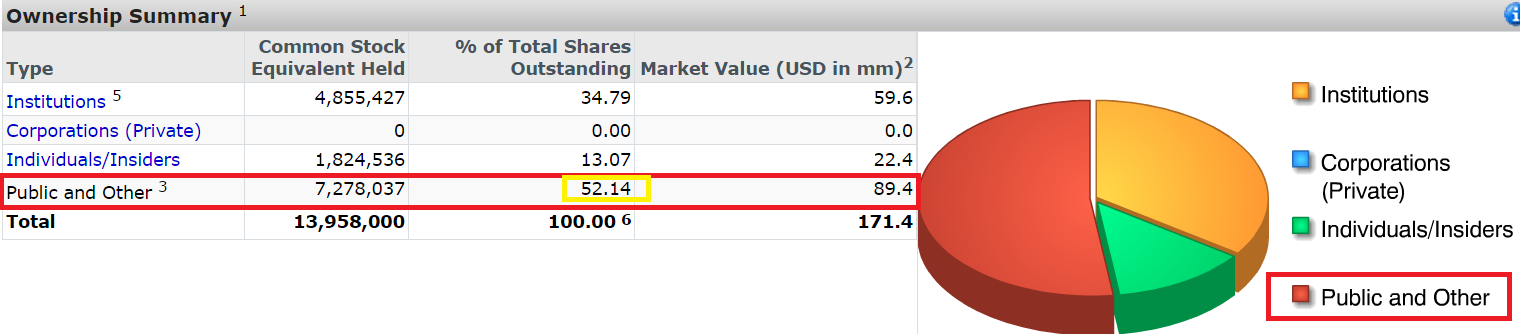

IDI Shareholder Base Is Essentially All Retail: Where Are The Credible “Real” Investors?!?

Given this horrific penny stock wipeout team and yahoo message board tout campaign, it is not surprising to me IDI’s shareholder base is mostly retail. In fact the only institutional investor involved of note is Frost ( through the original failed Tiger Media Investment). If you exclude insiders who didn’t buy their shares on the open market and Frost (who is involved through a failed investment in a fraud), IDI inc is held almost entirely by unsophisticated retail owners. There are no real institutions of any worth involved in IDI other than a few random ETF/Index followers resulting from IDI’s inclusion in the Microcap ETF.

(click to enlarge)

(picture credit Capiq)

Why doesn’t any “real” investment firm want any part of IDI?

(picture credit me)

TransUnion Lawsuit Renders IDI a “Zero” Immediately Anyway

What IDI’s retail shareholders need to understand is that this lawsuit is devastating to IDI’s desperate technology claims which, in part, support IDI’s temporarily inflated stock price. The TLO IP in this lawsuit took TLO >4 years and $100m+ to develop with a huge team, when IDI loses this lawsuit and any claim to the IP there is simply no way this tiny fraud ridden shell company has any hope of recreating it. Therefore once IDI loses this lawsuit, the only “technology” left will be some tiny debt collections company that has been struggling since 2001 and apparently spends $0 on R&D. Furthermore, now that TransUnion is embroiled in IDI’s technology and business I think if IDI makes any technology claims in the future: Transunion will respond with swift and endless litigation claims claiming any new IDI products are based on “prior art” and Transunion’s IP.

Furthermore, Brauser’s Federal Fraud litigation with Equifax and egregious lawsuit with Transunion clearly renders both of those companies “off limits” to IDI. In the data industry I see no way any company can be successful if they are “black listed” from having any dealings with those two juggernauts. Let alone the fact that Transunion seems intent on destroying IDI and if you read the court documents I believe you will see the TransUnion/TLO team feels offended personally by all of this.

Pic credit Transunion’s TLO

All the documents from the Transunion litigation against Brauer and IDI are free and publicly available here and I especially recommend reading the complaint and any transcripts. In the interest of time I will not go into detail and recommend you read up on this yourself. I will give you my quick-summary read on it though, which is once Transunion tried to enforce their noncompete agreements against IDI employees alleged to have violated them, Brauser tried to extort Transunion over claimed license fees due based on IP which TransUnion already purchased in the TLO bankruptcy auction.

The lawsuit centers around “BOLT code” which is code written in BOLT that scans across data sets. This is a common and any multiple data base tool like lexis Nexis or others have something like this. The other contested IP is the “BParser” code, which converts the BOLT code to C++ (universal programming language).

This is one of the most direct and obvious lawsuits I’ve ever seen because, comically, both of these pieces of IP appears expressly explained and spelled out to me in the 363 asset sale documents Transunion and TLO participated in. I think there is ~100% chance that IDI loses this resoundingly. For example, check out the express and direct description of the assets sold in bankruptcy as cited in doc 61 filed 3/18/15

“[T]o the extent that Ole Poulsen holds or asserts any interests of any kind in the BParser code converter software used or useful by the Debtor in the conduct of the Business (the “BParser Code”) or any other Business Assets, such BParser Code and other Business Asset shall be deemed an Acquired Asset and may be sold to the Buyer free and clear of all such interests….”

Furthermore, Brauser and IDI CEO Derek Dubner were intimately involved in the bankruptcy auction as Transunion states they served the sales order on both Brauser and Derek Dubner, as well as Interactive Data. While after the close of the sale, Poulsen and Brauser both had extensive ongoing involvement with the case concerning division of sale proceeds. Lastly, all of this IP appears to have been created using TLO hardware, stored on TLO’s servers and used 40+ TLO programmers. Even Poulsen was a full time employee of TLO at the time working on the IP and was paid by TLO and then by Transunion for this, and his home was even paid for by TLO, so any claims IP developed at home are his seems worthless as well.

None of this even matters much anyway, as TransUnion’s TLOxp is a dominant competing product that is cheaper and with more functionality than anything IDI can offer.

If you call TLO, their sales people will be happy to explain all the reasons they are superior to anyone else, and even if they were in fact inferior (they aren’t) Transunion’s enormous global sales force would steamroll anyone stupid enough to confront them. If TLO wasn’t superior then why would Brauser try to buy them before and get sucked into this impossible lawsuit over the IP?

TLO and Transunion are far cheaper too as they offer in depth reporting tools with “all you can eat” pricing for <$175 a month. For small, low-volume customers who prefer transactional pricing, TLO’s superior service costs ~$0.30 per search, making IDI’s quoted average price of $0.75 a full +925% more expensive than TLO This makes IDI inc’s desperate product offerings not just hopelessly behind the curve but simultaneously too expensive to be competitive. I don’t see how Transunion doesn’t just eat them alive over time.

IDI Board of Directors: It Gets Even Worse…..

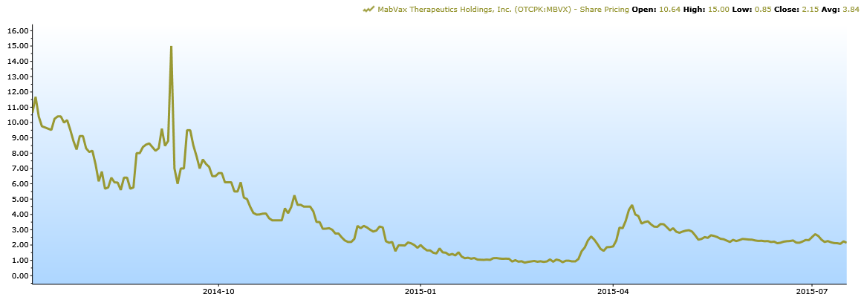

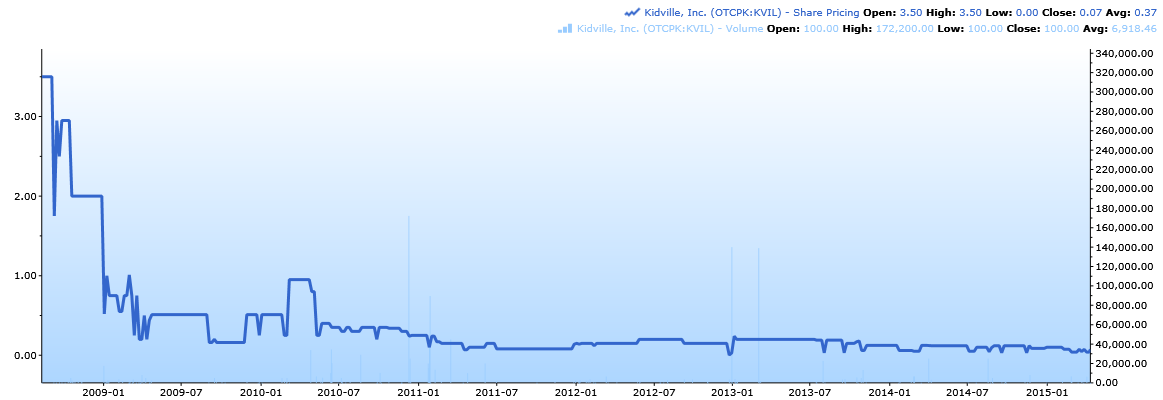

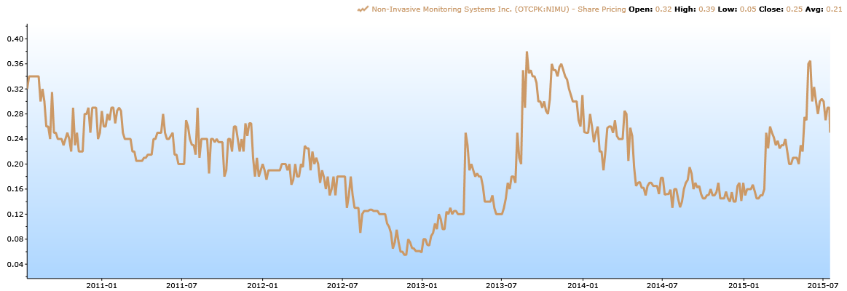

It’s not just Brauser and Honig though, basically everyone involved in this company is tied to financial disasters. You may think these people are protecting your best interest but, for example, take board member Steven Rubin, who is involved in:

MabVax Therapeutics Holdings (OTCQB:MBVX): Swift -79.79% wipeout

(click to enlarge)

And Kidville (OTCPK:KVIL): -78.86% Disaster

(click to enlarge)

And one of the “best ones” he is involved in, Non-Invasive Monitoring Systems Inc has been crazy volatile and is “only” down -21.84% at the moment

(click to enlarge)

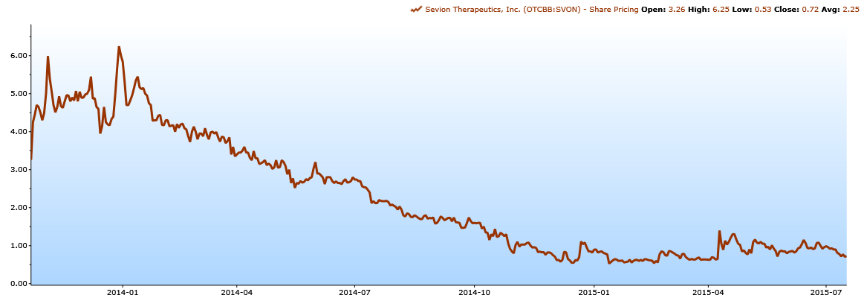

The list is nearly endless, so I won’t keep going much longer but look at Sevion Therapeutics (OTCQB:SVON) now -77.78% already despite raging biotech bull market

(click to enlarge)

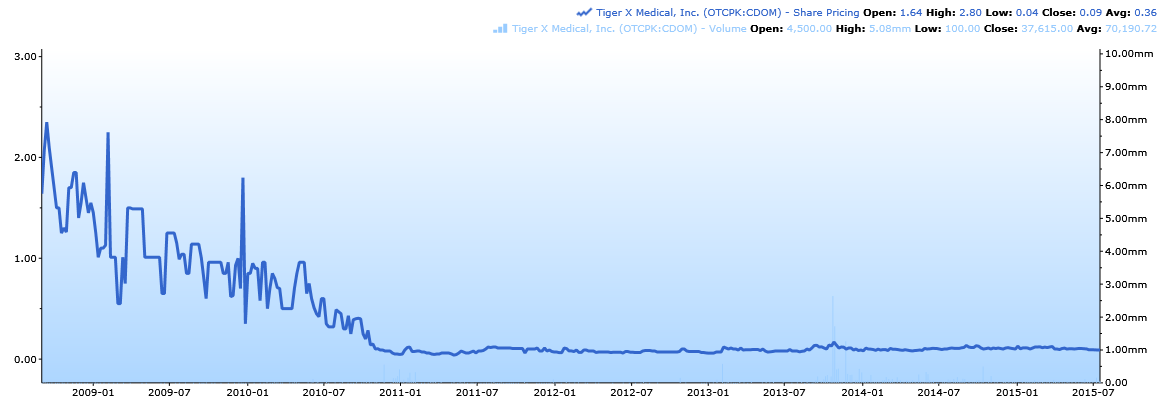

And Tiger X Medical (OTCPK:CDOM) which is now down -94.51%

(click to enlarge)

Another example is IDI board member Robert Swayman, briefly involved in Vapor Corp along with Honig and Brauser, which has (unsurprisingly) been a complete disaster

Vapor Corp -94.23% Stock Decline to date

(click to enlarge)

(all charts from CapIQ)

With everything you’ve read, are these really people you want to invest with? Are you honestly unable to find a SINGLE better company in the world run by better people to invest in?!

IDI Inc Management Response

Since IDI inc has been active in promoting themselves to investors it is not hard to meet them. I spoke with them not long ago but found their responses to issues raised to be underwhelming and disappointing. Instead of offering a clear picture of the current business, I found them to offer excessively promotional claims to TAM size and other vague claims. In response to questions regarding management quality, they claim IDI to be founded by the people who started the data fusion industry. However, the real genius leader of that (Hank Asher) passed away quite some time ago now and the last company these current people were involved in went bankrupt and nearly wiped out equity holders completely. I don’t see how this is reassuring. Furthermore it seems their sales and technology strategy is just “throw money at it” and I don’t see how they can possibly compete against sales and technology beasts like Transunion. IDI claims the lawsuit is irrelevant. However, I think the documents point to a different view while claims of litigation irrelevance ignore the reality I see, which is that Transunion seems intent on crushing IDI and wiping them out completely. Considering any future for IDI is based on technology, I don’t see how Transunion contesting their IP claims, likely forever, is anything other than disastrous.

IDI inc Catalyst: Heinous $160m Equity Shelf, Wall of Dilution as Shares Become Unlocked For Sale

What is rare with IDI is the clear and identifiable catalysts to collapse the share price. Primarily, IDI just filed an absolutely heinous shelf offering for the sale of $160m worth of IDI stock, considering IDI’s total market cap is ~$200m, this alone could wipeout current IDI shareholders.

It gets better though, as we have a huge amount of IDI inc shares becoming unlocked very soon. If you read the lockup agreement, there is no date next to the signature but we know the shares are locked up for 1 year starting sometime late 2014 or early 2015. This means that soon a wall of shares become unlocked for sale for a company trading at >40x revenue I think they will sell aggressively (if they are smart).

IDI inc = Desperate For Cash, Dilutive Secondary Offering Imminent

IDI also seems desperately low on cash, as we see here in 2014 where IDI claims they have enough cash to survive 12 months. However, IDI’s cash burn has ramped up, and the shutdown of the Chinese billboard business will cost at least -$1m in cash to shut down, while we are now nearly 8 months into 2015. This means IDI will have to raise cash within the next 4 months, and given companies rarely wait until their cash account is literally $0, I believe investors should expect another dilutive IDI capital raise sometime in the next 2 months. This seems like a lot of simultaneous wipeout-catalysts occurring very soon.

IDI inc’s Auditor “Deficiencies” and Inability to File SEC Filings On Time

Considering Brauser was sued by Transunion for alleged involvement in falsifying statements, it makes me horrified to see IDI has internal accounting integrity questions.

For example, of the two 10q and 10k filings IDI inc has been required to file since they became IDI inc, a full 100% of those have been filed late (the 2014 10k and the Q1 10q). One of these 10q filings seems to have been given to investors accidentally before IDI inc’s auditor was able to review it?!

Even more worrisome, IDI inc has curiously changed it’s auditor to “RBSM LLP” who in 2013 was just recently found by the PCAOB to have “audit deficiencies” and “failure to perform sufficient procedures to evaluate the presentation of certain revenue”. This does not appear to have been an isolated incident either as this 2013 inspection followed up an even worse 2009 PCAOB inspection where RBSM had “audit deficiencies” including a “deficiency of such significance that it appeared to the inspection team that the firm did not obtain sufficient competent evidential matter to support its opinion on the issuer’s financial statements”

IDI Inc’s Stated Market Cap on Yahoo Finance Not Accurate

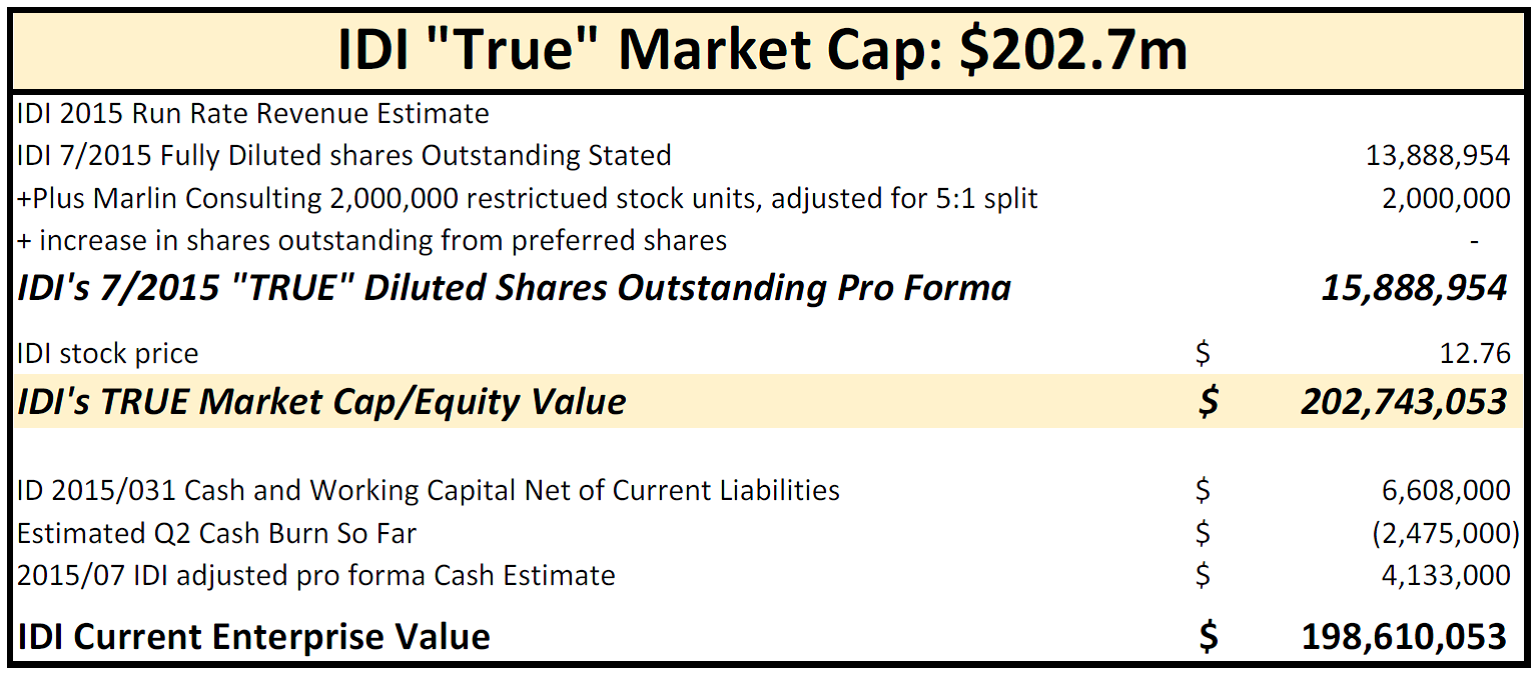

The first thing you need to know is that I believe the yahoo finance stated market caps are NOT completely correct as they do not seem to include the crazy “free” 2m IDI rsu shares that will be issued to Honig and Brauser’s through Marlin if/when IDI hits the comically low hurdle of $15m of sales or $10m of sales and positive EBITDA (excluding stock comp). At today’s price those rsu shares alone are ~15% dilution to current shareholders and if you correct for this, I estimate IDI’s current “true” market cap is $202m.

(click to enlarge)

Valuing IDI: “Best Case” Fair Value Analysis Shows -92.4% Downside

Even if IDI insiders were geniuses AND had shareholder interests at heart AND we use the most optimistic estimates possible, IDI inc is STILL overvalued by somewhere between -83.54% and -98% today.

Thankfully, valuing IDI inc is actually very easy as we have two very direct and recent comparisons we can use to value IDI. One of them is literally the transaction of the company IDI just bought that makes up all of IDI’s ongoing business. The other recent comparison is the recent auction of TLO, LLC which is a superior business to IDI in every way possible but we can use that sale price as the most optimistic upward bound possible for valuing IDI inc.

With these relevant comparisons we can then use some of the most optimistic assumptions possible to estimate “Fair value” for IDI inc. Unfortunately, even using the most optimistic assumptions possible I still come up with per share value for IDI inc stock with between -98% and -83.5% of downside today. Note this would also be very consistent with many other Honig/Brauser wipeouts which quickly fell between -70% and -100%.

(click to enlarge)

(estimated chart created by me)

As you can see above, valuing IDI based on the Interactive Data, LLC transaction they just did shows fair value per share for IDI inc of $0.969 per share for -92.4% downside from today’s stock price. Note that this analysis is using a $5m+ t12m revenue estimate for IDI inc also which I believe is quite generous considering the <$4m in revenue Interactive Data LLC was just producing and the nearly $0 in recent R&D spend they disclosed.

If we use Ole Poulsen and Derek Drubner’s latest bankruptcy TLO, LLC we can see that despite multiple bidders and an extended auction, there was only $19m of equity/stockholder value left. Note that this purchase price by TransUnion likely assumes that TLO’s products could be pushed through TransUnion’s enormous global sales force, allowing Transunion to pay more than would typically be a fair value. If we use that equity valuation as a comp for IDI we see that IDI inc stock is worth a maximum of $0.26 per share, for -98% near term downside for current shareholders.

If we even take the whole analysis to the most optimistic view possible and literally completely ignore ALL of the $100m+ in debt/liabilities TLO, LLC filed bankruptcy with and just give that all to equity holders instead, then retain the bullish $5m+ revenue estimate for IDI inc, we STILL see that IDI inc stock has near term downside of -83.54% from today.

As you can see, IDI inc today trades at what is an impossible “bubblicious” valuation that would make many doc com stocks blush. Educational tip: if you ever see a promotional investor presentation with endless rambling about the “Addressable Market!” but ZERO mention of the company’s current financials or earnings, that company is likely to be a future wipeout.

(picture credit)

Frost Himself Seems To Know IDI inc Not Worth Anything Close to Today’s Prices

Lastly and most hilariously, we know Frost expressed interest in bidding on TLO in bankruptcy. We know TLO had 200+ employees, was built by the founding genius of the industry, had ~$100m of liabilities (likely a good proxy for cash burned), and took 5+ years to be built with its ~$23m of revenue. Clearly this is a superior company to IDI inc in every way possible.

(click to enlarge)

(picture credit)

We also know that Tranunion initially won the stalking horse with their ~$100m bid (which basically wiped out the equity and covered the debt/liabilities) after Frost was rumored to have put in a bid worth ~$100m, leaving ~$0 value for TLO equity/shareholders. From this we can clearly infer that Frost was not interested in paying $100m+ to own the vastly superior TLO company (otherwise HE would have been the stalking horse or done the DIP, etc). Yet now we have IDI inc, inferior in every way imaginable, trading for >$200m implied valuation!

Plungey Makes The Call: IDI Will Be A(nother) Shareholder Wipeout With -92.4% Wipeout (or worse)

(click to enlarge)

(picture credit me and Indiana Jones)

IDI inc: -98% Near Term Downside with Wipeout Coming = DON’T FALL FOR IT.

I believe the bottom line is that under no reasonably reality is IDI worth anything even vaguely close to $200m. The people in charge of IDI saw their last company recently go bankrupt despite leadership from the undisputed king of the modern data era Hank Ahser, who unfortunately passed away and will be deeply missed. Remember TLO took 5 years, hundreds of employees and apparently at least $100m of cash, to build and that still went bankrupt and nearly wiped out the equity investors entirely. Michael Brauser and Barry Honig seem to me a penny stock wipeout team so toxic that even if Frost invests, their involvement virtually ensures wipeout or fraud accusations. The wreckage of bankruptcy and wipeout in their path is truly eye watering. Furthermore, IDI currently trades at a “bubblicious” valuation relative to obviously superior and much larger companies while the current Yahoo message board stock promotion campaign is extremely concerning.

While hyped up “data fusion!” fad claims and yahoo message board stock promotion may temporarily inflate valuation, reality and the wave of IDI stock sales coming will bring this disaster crashing back down, like so many other Honig and Brauser wipeouts. Ultimately, IDI is made up of a tiny, 14 year old, struggling debt collection service paid for with $5.6m in cash and no amount of weirdly promotional stock tout articles or confused “mom & pop” retail stockholders can change that.

This temporarily insane 40x revenue valuation coupled with large $160m shelf offering filed, and a huge volume of shares becoming unlocked, means insiders could aggressively dump their shares onto the market until IDI falls all the way to $4 per share. At which point IDI would STILL have another -85% downside even from there. I believe it is obvious that, like VRNG, IZEA, BVSN, USEL, DROP (and countless others), the end will come suddenly and violently, leaving you with no chance to avoid suffering a crippling financial loss.

DON’T FALL FOR IT.