“Davidson” submits:

Trying to absorb all the significance of the information at any point in time can be an enormously daunting task. It is much like being suddenly absorbed in a dense ‘FOG’. For investors it is the ‘FOG’ of too much information. It is why stepping back from it all lets one visualize which trends hold up over time as actually carrying predictive value for investors.

Over the long term markets are driven by employment trends and resulting retail consumption. But, there is so much happening which seems significant, with so many differing opinions in the media that it is really quite easy to become baffled about what the best decisions are at any point in time.

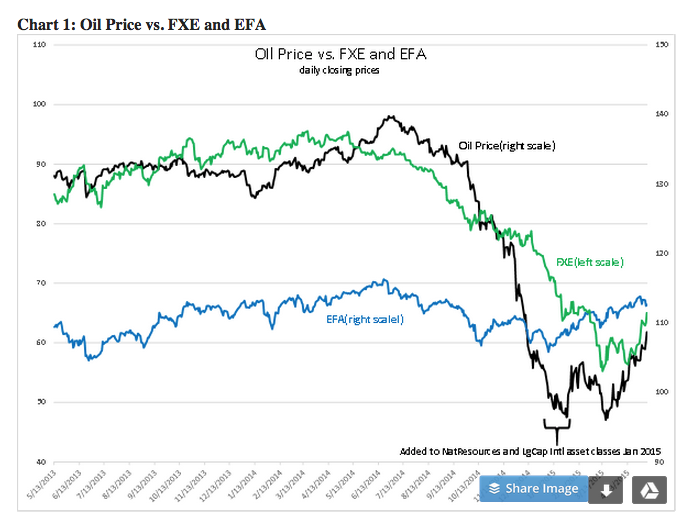

The last 12mos has witnessed a collapse in oil prices, the soaring value of the US$ vs. global currencies, historically low global interest rates and for US based investors a fall in the relative values of foreign equities. See Chart 1: Oil Price vs. FXE and EFA. It looks like a real mess brewing!! How does one sort it out to make prudent decisions going forward?

How does one sort it out to make prudent decisions going forward?

Part 1:

In Chart 1: Oil Price vs. FXE and EFA, Oil Prices ($OIL) ($USO) per bbl. in US$ daily closing prices is shown by theBLACK SOLID LINE on the left scale, the ratio of the US$/EURO is represented by FXE and shown by the GREEN SOLID LINE while the LgCap Intl equities is represented by EFA and shown by the BLUE SOLID LINE.

Lets walk through what the we experienced since 5/13/2013. From 5/13/2013 to roughly 3/18/2014 oil was rising along with EFA and the FXE. At that point in time many Hedge Funds had short bets against the US$ vs. foreign currencies and long bets on oil prices as many stated they believed that the Fed QE actions would result in ‘Hyperinflation’ for the US. The general feeling was that we were in a global recovery, European and International equities appeared to carry better opportunities.

Capital was adjusting to take advantage by shifting away from the US$ and into oil and Intl Equities. Then Vladimir Putin began his action to seize parts of the Ukraine. This did not cause an immediate investment change globally as investors took several weeks to assess the severity of Putin’s actions, but one of the first actions a look back reveals was a shift of short-term capital into the US$ which caused the FXE to fall beginning 3/18/2014.

The EFA continued to rise till 6/19/2014 till it began to fall. Oil peaked 6/26/2014 before its fall began. The evidence supports the scenario of 1st a burst of capital left Russia due to Putin’s actions. This capital entered US Treasuries (lowering the rates/causing a price rise). Then as it appeared that Putin was widening his invasion of Ukraine bets were removed from Intl LgCap assets. As both EFA and FXE fell, oil prices may have risen somewhat on concerns of global disruptions, but Hedge Funds were seeing losses with heavily levered currency and short US Treasury positions.

Oil’s price rise eventually peaked 6/16/2015 as losses from ‘Hyperinflation’ bets forced Hedge Funds to sell oil to cover mark-to-market margin calls. The correlated price changes shown in Chart 1: Oil Price vs. FXE and EFA reflect a short term unwinding of a ‘Hyperinflation’ bet which did not pan out and the result of a highly levered trade impacted by a geo-political event. The media reports reflect that significant damage to Hedge Funds during this period. Oh, by the way, inflation has remained between 1%-2% for the past 5yrs and the latest read is 1.6% from the Dallas Federal Reserve.

Subsequently, many have assumed that global economic activity has entered a major correction. A number have called for significant market corrections in the near future. The bounce back since we repositioned portfolios in Jan 2015 to take advantage of EFA and Natural Resource declines has already been significant. The economic data does not support a pessimistic outlook.

In my experience, I expect a recovery in EFA, oil and FXE to occur over the rest of the year. Expecting a return of EFA to new highs, a return of oil to ~$90bbl and a return of FXE to 130-140 is not unreasonable if the global economy continues the current uptrend in my opinion.