In the wake of a recent flurry of buying action in Western Potash Corp., investors are left wondering whether the advanced-stage potash developer is in the crosshairs of a deep-pocketed suitor.

We have reason to believe that this is likely the case. And we believe that smart investors are merely positioning themselves ahead of a potential takeover bid or the signing of a joint venture partnership with a mining industry giant.

Weighing in Western Potash Corp. (TSE:WPX)’s favor is the fact that its world-class Milestone project in Saskatchewan boasts a projected annual production of up to 2.8 million tonnes of potash. As we laid out in our Initiating Coverage on February 19, 2014, Milestone has an anticipated minimum 40-year mine life with one of world’s lowest projected production costs.

Recently on March 1, 2014, the Deccan Herald – a leading English-language daily newspaper in India – propelled M&A speculation to the next level in an article titled “Roping in Canada for food security”:

“In the future greater potash supplies from Canada will also reach Indian shores via investments being made by companies like Rashtriya Chemicals and Fertilisers Limited which is looking to acquire a 40 per cent stake worth a billion US Dollars in a joint venture with Western Potash Corp for a new mine in Saskatchewan.”

Dr. Didar Singh, current Secretary General of the FICCI (Federation of Indian Chambers of Commerce & Industry) and former Secretary to Government of India in the Ministry of Overseas Indian Affairs, emphasized in his article for the Deccan Herald that Canada is in a unique position to play a “significant role in aiding India generate enough food for its populace… through its supply of pulses and fertilizer.”

He noted that “India after all imports a major share of its potash requirements from Canadian entities like the Potash Corp./Saskatchewan Inc. (TSE:POT) (NYSE:POT) which is incidentally the world’s largest producer of potash.”

R.G. Rajan, Chairman of Rashtriya Chemicals & Fertilizers Ltd (NSE:RCF) (BOM:524230) (India’s second-biggest state-run producer of fertilizers) announced already in 2012 that it “plans to buy into potash mines in countries including Canada to secure supplies”, or as Bloomberg put it:

“Owning stakes in potash deposits overseas may help the Mumbai-based company shield many of India’s 235 million farmers from rising costs when the annual monsoon is deficient, as the past years have shown that a lack of rain is threatening to crimp agricultural output… India is a large importer of potash with no domestic supplies. It is logical to secure supply of potash particularly if the acquirer thinks that potash prices will rise more than generally expected.”

So who would be the most obvious candidate to acquire Western Potash Corp. (TSE:WPX) or to enter into a strategic partnership to build a mine at Milestone?

The answer to this question is not simple, as there are multiple parties around the globe probably having a real interest, especially at current low market prices and valuations.

To start with, sovereign wealth funds (SWFs) in India, Brazil, Middle East and Asia all would have an interest in getting involved and seeing Milestone going into production as it is their mandate to ensure security of supply for their countries food production.

There are political motives behind the motivation of SWFs to feed their respective populations – they want security of supply more than there is a concern over price.

China BlueChemical

At first glance, Western Potash appears well-suited to a Chinese end user. Such speculation is fuelled by the fact that the company received an indirect $33 million financial infusion in 2013 from a consortium led by China’s largest state-owned fertilizer producer, China BlueChemical Ltd. (HKG:3983) (OTCMKTS:CBLUF).

This strategic investment was accompanied by the signing of an off-take agreement. This means that China BlueChemical – a subsidiary of China National Offshore Oil Corporation (CNOOC) – will be sold potash for at least 20 years, assuming it secures financing for the $2.9 billion needed to build a mine at Milestone.

However, the Chinese are not the only players on the world stage with deep pockets and a hunger for potash. In fact, China BlueChemical’s involvement with Western Potash may not be the catalyst for the recent pronounced uptick in the company’s share price.

Though the share price has since settled down, the rumor mill continues to suggest that Western Potash is being courted by at least another power player.

John Costigan, an official company spokesperson for Western Potash, declined to comment on such speculation. So too did David Ovington, Rio Tinto plc (ADR) (NYSE:RIO) (LON:RIO)’s London-based investor relations spokesperson.

However, my research suggests to me that there are several possible suitors, some of which are actively developing their own potash projects in Saskatchewan among the world’s richest and most prolific potash fields. They include the global mining heavyweights Potash Corp. of Saskatchewan, BHP Billiton, Rio Tinto, Vale Inco and the German fertilizer producer K+S.

These companies would not want to see a new potash mine being developed and advancing to one of the world’s lowest cost producers as it would mean losing considerable market share, especially during current times of low market prices and increased supply from Russia.

K+S

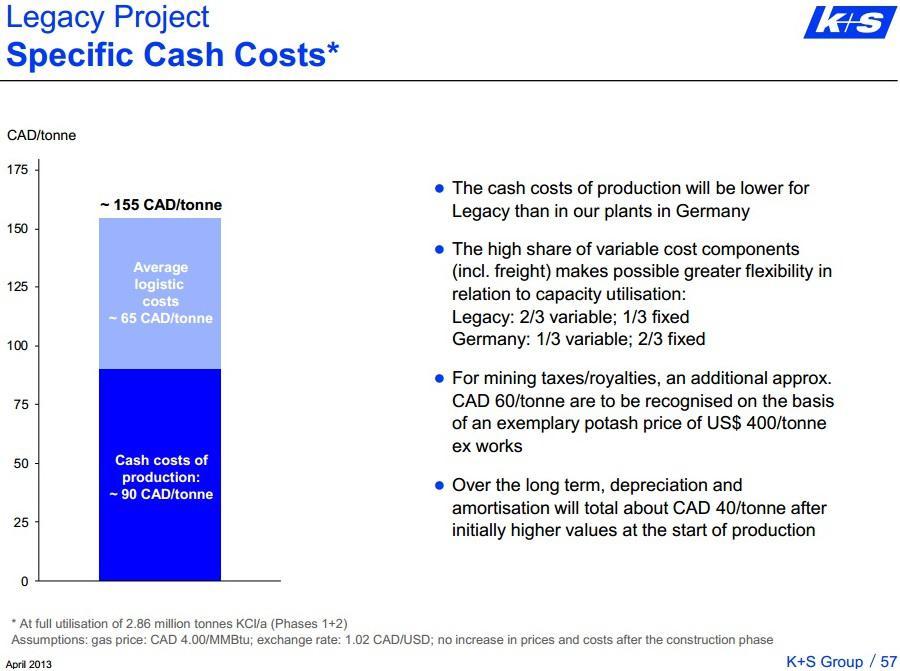

According to K+S, the acquisition of the Legacy Potash Project in Saskatchewan was an “important strategic step”. This is mainly due to the fact that K+S’s mines are typical high-cost operations, whereas in 2016 Legacy will be one of the few potash mines of the world that can glory in itself of being among “lowest-cost”. Without Legacy, K+S would face serious concerns of staying profitable in a potash market that is as depressed as today.

Despite its seemingly high price, the $434 million acquisition of Legacy has erased a lot of pressure from K+S as their average cash costs of production will be decreased substantially.

In our Initiating Coverage piece on Western Potash, we presented the extreme similarities between Legacy and Milestone. Considering that K+S paid more than $400 million for Legacy and that Western Potash’s market capitalization stands at around $100 million today, the market would perceive a take-over as a relative bargain, especially when considering that other major competitors have a strong interest in taking Western Potash out as well.

There are distinct advantages for K+S developing Milestone into a mine while Legacy is being put into production successfully in the next 2 years, as this would bring a doubling of good effects for K+S’s share price within a relatively short period of time (or intentionally at a later time when strategically needed which would make Milestone a powerful ace up K+S’s sleeve.

Potash Corp. of Saskatchewan

In order to remain the world’s largest fertilizer company by capacity and to keep its ties strong with India, acquisitions of undeveloped potash deposits represent best practice. With operations and business interests in 7 countries, Canadian operations supply around 20% of the company’s global capacity. As per its corporate vision to “play a key role in the global food solution while building long-term value for all stakeholders”, the mission to keep that vision alive must be only through acquisitions.

According to Potash Corp.: “In particular, we emphasize relationships with entities near our operations to the extent they meet our requirements.”

BHP Billiton

In late 2010, Aussie mining giant BHP Billiton Limited (ADR) (NYSE:BHP) tried to take over Potash Corp. in a $38 billion deal. After it was forced to pull out of the deal, BHP complained that it made “unparalleled promises” on jobs and investments, including commitments to spend $370 million on infrastructure mainly in Saskatchewan.

Despite the rejection, BHP said it would still develop its Jansen Potash Project into new potash mine in Saskatchewan, however the benefits of a second potash mine (e.g. Milestone) being developed in the same region and, more or less, at the same time are obvious as terms like “synergies” and “economies of scale” are well-received key words in the board rooms of any one of the top-3 largest mining companies in the world, besides Rio Tinto and Vale.

Rio Tinto

In my opinion, the real stand-out candidate is the diversified mining giant Rio Tinto. By way of background, all of these big-league miners have been aggressively muscling their way into Saskatchewan’s very profitable potash mining business over the past few years. This is because of the long-term prospect for heightened global potash demand. Especially against a backdrop of rising crop prices and an additional 75-80 million mouths to feed each year. Hence, there’s a growing urgency to maximize crop yields with the aid of potash-based fertilizers.

Furthermore, it’s worth noting that Saskatchewan boasts about half of the world’s potash reserves and produces about a third of global output. It’s also a politically safe environment to work in. Hence, it has lots of appeal to major mining companies that see a bright future in potash.

So, why would it be a good fit for Rio Tinto to acquire Western Potash or at least team-up with the small Vancouver-based company to advance Milestone into production?

First of all, Milestone is technically de-risked. So the commercial viability of a future mine has already been demonstrated. And Western Potash already holds all the necessary governmental environmental approvals in its hands. The company has also solved all of the logistics required to transport its potash to overseas buyers.

All of this means that there are no meaningful hurdles left that could jeopardize the building of a mine – except for financing. This is not the case for Rio Tinto’s adjoining Regina Potash Project, which is at a much earlier developmental stage and which has many potential obstacles to overcome before a mining decision can be made. Milestone is a multi-billion dollar asset that can be cost-efficiently commercialized in as little as three years.

All told, the acquisition of Milestone would significantly speed-up Rio Tinto’s timeline to commercial production. It would also mitigate any risks that might de-rail the mining giant’s plans to become a prolific potash producer in the heart of Saskatchewan.

Next, it’s worth noting that Western Potash is developing a solution-extraction mine. This mining methodology translates into much lower capital expenditures and operating costs than conventional potash mines.

For instance, let’s consider water, which is the lifeblood of a solution-extraction potash mine. That’s because a large amount of water is required to flush deeply-buried potash to the surface, rather than mechanically excavating it. It is important to realize that Milestone actually adjoins Rio Tinto’s Regina Potash Project. But unlike its upscale neighbour, Western Potash has access to a virtually unlimited supply of water that won’t drain any nearby aquifers.

Conversely, Rio Tinto may yet face legal action from First Nations people (aboriginal Indians) if it goes ahead with plans to use the nearby Buffalo Pound Lake for its water source. This is a reservoir that First Nations people, urban populations (including the cities of Regina and Moosejaw), and other stakeholders rely upon for potable water and for irrigation purposes.

Most significantly, Western Potash has strong “green” credentials, by which is meant that it has signed an agreement to pay the nearby city of Regina to redirect much of its treated sewage water to the company’s Milestone project site. Currently, this effluent is deposited into the nearby Wascana River.

Not only does this agreement benefit the environment, but it also offers the company a strategic long-term water supply for its solution-extraction mining requirements. In so doing, Milestone will be the first potash solution mine in the world to use treated effluent – rather than fresh water – to extract this salt-based mineral.

We assessed that the importance of the following reality may not be overstated: If Rio Tinto can acquire Western Potash or at least partner-up with the aspiring miner to jointly develop their adjoining projects, this would help solve Rio Tinto’s water access issues. It would also offer a key competitive advantage by allowing these two potash projects to merge as one massive consolidated asset. In turn, this would make for a very scalable and especially long mine life.

It would also be an arrangement that would suit Rio Tinto’s corporate mandate to be a conscientious steward of the environment. According to John Costigan, this ground-breaking use of waste water will serve as an example of how trendsetting 21st century mining companies are giving the industry an image makeover that benefits everyone. “It’s more than a win/win for all the parties involved. It’s also a big win for the environment,” he says. “We hope that this agreement provides proof that economic and environmental sustainability in our industry is not only achievable with a little creative thinking, but it can also pay big dividends for all stakeholders.”

As a fringe benefit, the Wascana River will also be revitalized by Western Potash’s diversion of waste water to its mine site. This promises to mitigate all the pollution-related algae in the river that’s caused by the inflow of treated effluent. Obviously, wildlife stands to gain, too, especially since summer algae blooms can sometimes be toxic. All of this should be music to the ears of such an image-conscious multinational corporation as Rio Tinto.

In summary, the odds in favor of a lucrative potash mine being commissioned at Milestone are very strong. And that offers the opportunity for Rio Tinto, and others, to fast-track its entry into the lucrative potash mining industry by way of an outright acquisition of Western Potash or a joint venture partnership.

Either way, Western Potash shareholders would stand to benefit considerably. For instance, a buy-out would allow them to cash-out at prospectively much higher prices. Or a joint venture would presumably allow them to see the intrinsic value of their share holdings appreciate exponentially over the next several years.

Once again, the catalyst for this ideal scenario would involve Rio Tinto, or others, providing the necessary funding to make Milestone a low-cost, high-margin mining operation with a decades-long future.

Live chart (15min delayed)

Live chart (15min delayed)

The above represents an excerpt of the research update #1 which can be viewed as a PDF in English and German.

Beware that there are risks associated with Western Potash Corp. – namely financing. Further risks we identified can be read at the end of our last article on Western Potash Corp. titled “Primed To Build A World-Class Potash Mine“.

The mentioned companies represent just a few of the candidates that would be motivated to buy or partner with Western Potash. Rockstone will continue to monitor the situation and research candidates as this opportunity grows.

Neither Rockstone Research Ltd. nor the author was not paid or remunerated by any of the companies mentioned herein to produce or publish this content. However, the author holds shares of Western Potash Corp. and therefore would financially benefit from volume and price appreciation. Please read the full disclaimer within the below mentioned PDF and on rockstone-research.com