Written by Evan Bleker Website

Small retail investors have a real advantage over the pros.

Unfortunately, this advantage is forfeited in order to play a game that’s stacked against them.

Retail Investors: Why Play a Hard Game?

I see it all the time.

Blog posts or stock forums usually focus on well known large cap stocks and popular issues that are in the public eye.

The majority of posters are small retail investors, investors with tiny personal portfolios, who have gotten caught up in the pursuit of hunting big game. There are countless posts about Apple, one of the world’s top tech companies, or online super-retailer Amazon.com.

Digging down into the portfolio of an average retail investor I’m sure you would find the same thing.

A list of large, well run, well known companies usually purchased because of a favorable future outlook. The problem with this strategy is that many large institutional investors are also hunting big game but they’re using better hunting equipment.

The average mutual fund has far more resources at its disposal to identify and research medium or large cap stocks than a small private investor could ever have.

A mutual fund can attract the top minds from the top business schools and place them behind a $10,000 Bloomberg terminal which constantly spits out accurate and timely financial data.

That analyst can then spend hours pouring over the financial data, go over additional industry reports, and even talk to management or suppliers to get a strong sense of what the company is worth and how it will likely do in the future.

The Wall Street pros are smart and well funded with far more time available to research investment ideas than you or I.

One Critical Advantage the Small Retail Investor Has

With so much brains and technology on Wall Street, how can a small investor hope to compete?

Emotional temperament?

Many top traders and professional investors have honed the emotional intelligence needed to do well in investing.

Graham & Dodd?

There are enough investors on Wall Street who have studied all the old masters to almost render your Graham and Dodd advantage null and void.

Rather than strategy or temperament, the most significant advantage that small investors have over the Wall Street crowd is that they’re not subject to institutional constraints.

Chief among these is the freedom to invest in small, out of the way, companies.

I’m not talking about “small” $500 million companies, I’m talking about the same size companies I send to investors who have signed up for free net net stock ideas – tiny companies trading at market caps of $50 million or less.

Mutual funds and hedge funds face serious constraints.

Aside from being forced into specific investment styles or sectors, or even needing to keep up with the market indexes quarter over quarter, one of the biggest problems professional money managers suffer from is obesity.

Fund managers can’t buy just any stock they want to – they’ve stuffed themselves far too full of investment assets for that.

In 2011 the average mutual fund had just shy of $1 billion under management.

Most mutual funds don’t want to own more than 10% of the outstanding shares of any one company because of the regulatory issues and the possibility of spooking management who might fear a hostile takeover. On top of that, the fund manager can run into serious problems trying to find the market liquidity to buy or sell large chunks of a company.

For these reasons, the typical money manager keeps his positions small relative to the size of his portfolio and this has serious consequences for his investment universe.

If the average manager in 2011 wanted to hold no more than 100 positions, he would have to buy shares in firms that were at least $100 million in market cap. But, how many managers can have 100 great ideas, let alone shortlist and select 100 promising investments?

To keep things more manageable, a fund manager might opt for 25 to 50 stocks, which would mean shrinking his universe of potential investments to companies worth $200-400 million or more.

Things get even worse for larger established funds.

Funds with $20 billion under management would be limited to firms worth $2 billion or more if they wanted to hold 100 positions.

That same fund would need to invest in firms with market caps of $4 billion or more if it wanted to keep its portfolio a manageable 50 investments. Looking at the table below, with only 400 companies that have a market cap of $4 billion or greater, you can see how a larger portfolio can act as a huge disadvantage.

…or, conversely, how a smaller portfolio can be a huge asset.

The $1 billion fund has, on the other hand, nearly 5 000 stocks to chose from, depending on how it wants to carve up its portfolio. That’s an awful lot of investment opportunities, but that number doesn’t look as impressive compared to the 14 000 mutual funds out there.

That’s nearly 3 mutual funds for every stock!

Things get much better for small retail investors. At market caps below $100 million, retail investors face next to no competition from professional money managers.

Dip down even further and the competition approximates zero.

Fund managers just can’t touch tiny stocks. The only competition that retail investors are likely to face is from other retail investors – many of which are unsophisticated investors. The bottom of the market can get very, very, inefficient.

Small Companies Have Mighty Returns

And that’s just one reason why investing in tiny companies really pays for small retail investors.

The other reason has to do with population returns.

It’s been known for decades now that tiny companies, as a group, outperform larger companies when it comes to growth.

That’s really no surprise. At a certain size companies start experiencing the opposite of “economy of scale”.

They become bloated and bureaucratic.

It becomes harder for them to adjust to changing market conditions or capitalize on significant opportunities. These tendencies might be one of the reasons it becomes much harder to double sales at $50 billion than it was to double sales at $50 million.

To add to the difficulty, larger firms can end up butting up against the limits of their chosen market or, at least, might have exhausted the pool of easily obtainable customers, making it much more difficult to grow sales.

Every market has people who are dissatisfied with a competitor and wants a change. These customers might be the easiest to grab but the more satisfied the customer is with a competitor’s offering the harder it is to convince these customers to give your company a chance.

Eventually the firm has to actually start growing the market itself.

It’s not just growth stocks that do better when they’re smaller. All sorts of classic value strategies perform better with smaller market caps.

In one study, taken from Tweedy Browne’s What Has Worked in Investing, Tweedy shows the effect that company size has on stocks grouped in terms of price-to-earnings valuation.

As you can see, portfolios of smaller companies with low PE ratios clearly outperform portfolios of larger firms trading at low price-to-earning ratios.

At each rung, as the average market cap shrinks, returns grow.

This alone should be enough to make classic Benjamin Graham investors rethink the size of the firms they’re looking at.

As a net net stock investor, though, I’m primarily concerned with how firm size affects the returns of net net stocks.

Does the same pattern exist?

Do portfolio returns increase as the average market cap shrinks?

To be able to buy high performing net net stocks at all you have to look at micro cap and nano cap stocks. Net net stocks just don’t exist within the small, medium, or large cap universes – at least not in any meaningful numbers – so value investors are forced into small stocks if they want to take advantage of Benjamin Graham’s most profitable investment strategy.

As it turns out, size even plays a crucial role within the pool of NCAV candidates itself.

Looking at all NCAV stocks trading at 75% of NCAV or less, Vanstraceele and Allaeys (2010) found a sharp drop in returns as the average market cap in their portfolio grew in size.

Keep in mind that while absolute returns seem low, the market returned an average loss of 3.13% during the same period. Once again NCAV stocks thumped the market.

How Market Cap Affects Annual Yearly NCAV Returns

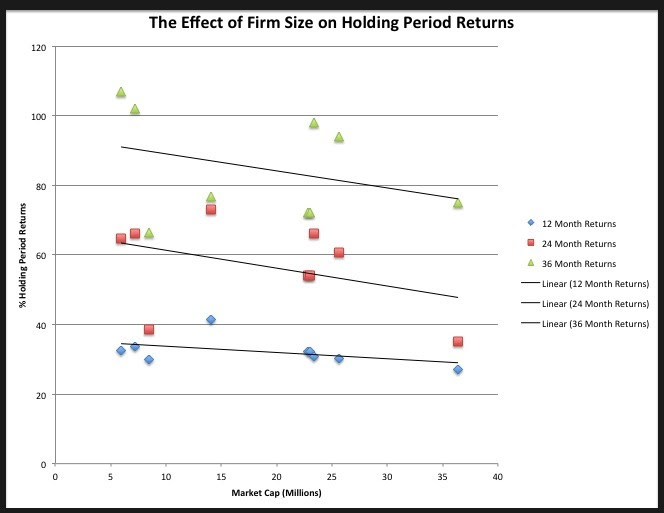

How Market Cap Affects Annual Yearly NCAV ReturnsIn one of my favorite papers titled, Net Current Asset Value, Financial Distress Risk, And Overreaction, net net stocks are broken down even further – this time below the $40 million market cap level.

The study looked at stocks trading at 67% of NCAV or less between 1971 and 2007. While the effect of market cap size isn’t nearly as pronounced as it was in Vanstraceele and Allaeys’ study, there is still a solid trend with the smallest firms meaningfully outperforming the larger firms.

The Effect of Firm Size on Holding Period Returns 1971-2007

The Effect of Firm Size on Holding Period Returns 1971-2007Go Small If You Want the Best Returns

While small retail investors may not have access to the same resources that large institutional investors have, I’m not at all sure this matters.

Small investors constantly do themselves a disservice by investing in medium or large cap companies, thereby locking horns with a massive herd of professional money.

This is a bad way to invest.

If small retail investors want the best possible returns when picking their own stocks, then they owe it to themselves to invest in small stocks.

Doing so means searching for great investment opportunities where they’re most likely to be, capitalizing on favorable population returns, and embracing the biggest advantage that small retail investors have over the pros.

So, what’s the smallest stock that you are currently invested in?