Stanphyl Capital letter to investors for the month of June 2019, discussing the core points of their Tesla short thesis.

Friends and Fellow Investors:

Q1 hedge fund letters, conference, scoops etc

For June 2019 the fund was down approximately 11.5% net of all fees and expenses. By way of comparison, the S&P 500 was up approximately 7.0% while the Russell 2000 was up approximately 7.1%. Year-to-date 2019 the fund is up approximately 17.5% while the S&P 500 is up approximately 18.5% and the Russell 2000 is up approximately 17.0%. Since inception on June 1, 2011 the fund is up approximately 93.3% net while the S&P 500 is up approximately 159.2% and the Russell 2000 is up approximately 106.7%. Since inception the fund has compounded at approximately 8.5% net annually vs 12.5% for the S&P 500 and 9.4% for the Russell 2000. (The S&P and Russell performances are based on their “Total Returns” indices which include reinvested dividends.) As always, investors will receive the fund’s exact performance figures from its outside administrator within a week or two and please note that individual partners’ returns will vary in accordance with their high-water marks.

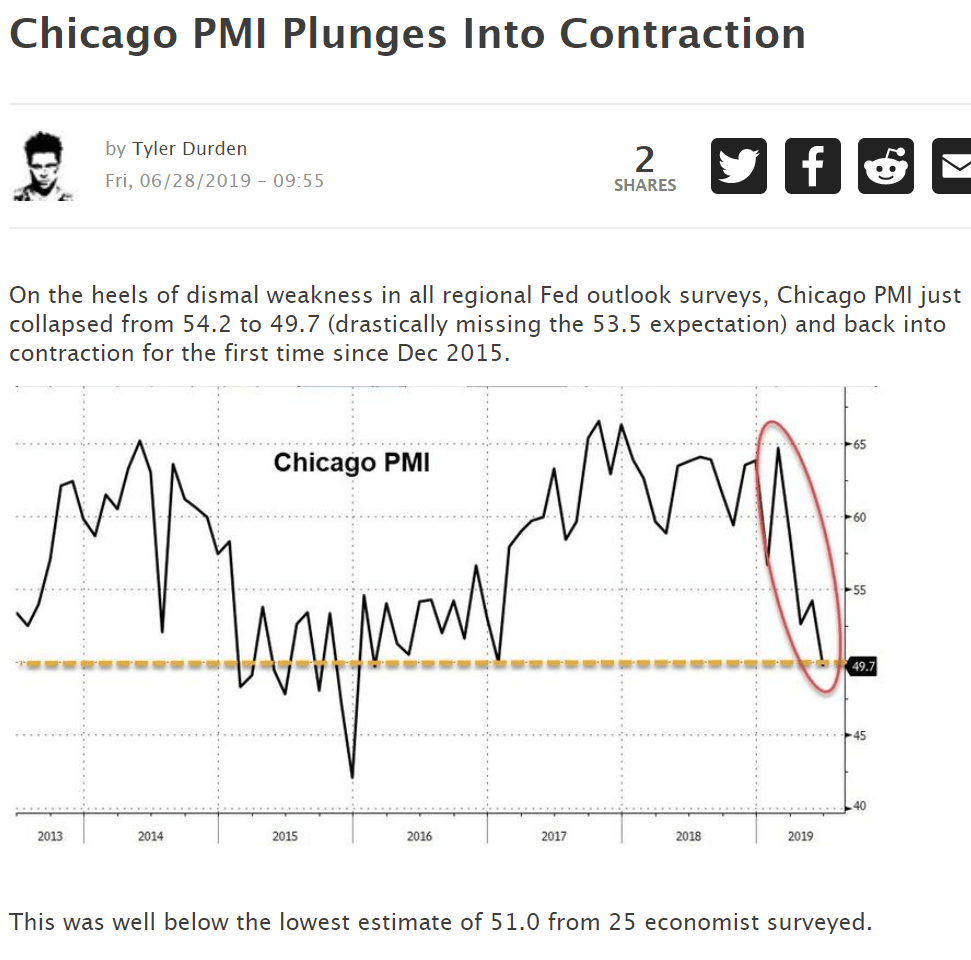

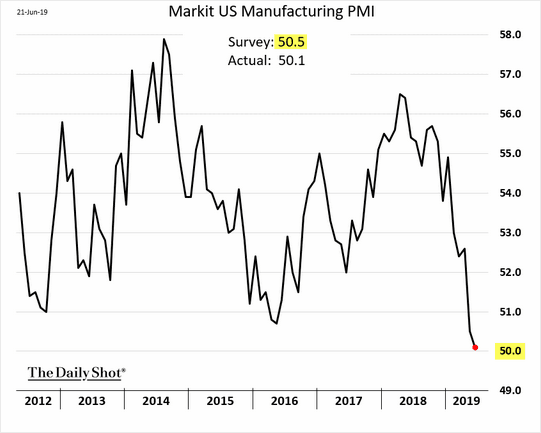

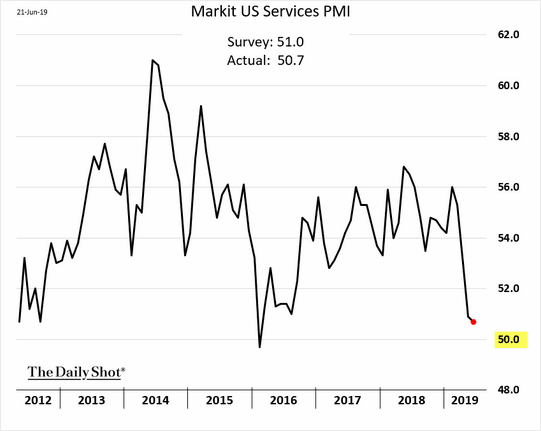

Our terrific May performance was almost completely unwound in June as our myriad short positions (the fund is currently very net short) reversed themselves. Despite this setback we remain very net short as I continue to believe we’re entering a bear market for U.S. stocks. In fact, although the S&P 500 set a nominal new high this month the individual stocks and Russell 2000 index we’re short are all well below their 52-week highs, and there’s ample evidence the U.S. economic slowdown is worsening:

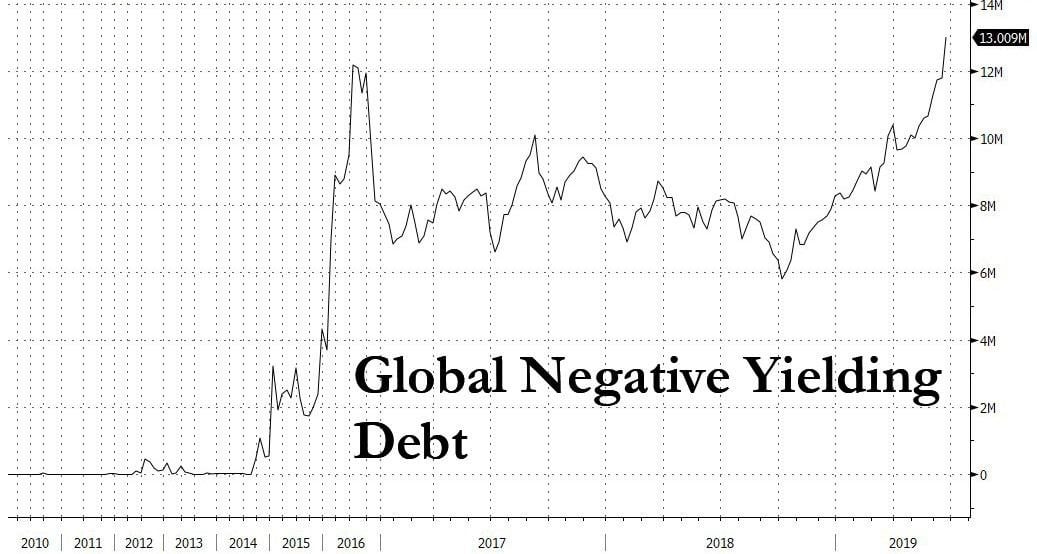

…while global negative yielding debt (a sign of a massive looming economic slowdown) has broached the insane level of $13 trillion:

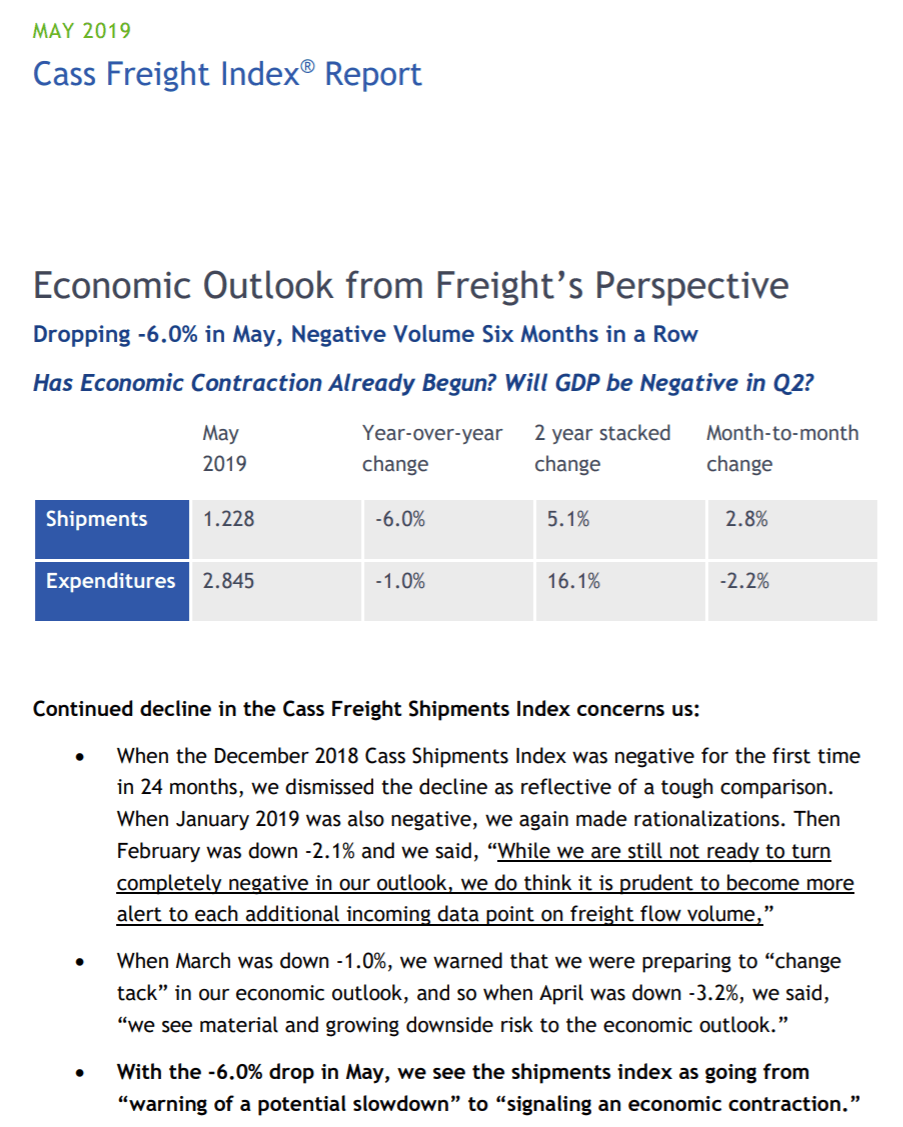

And have a look at how ugly U.S. rail traffic is.

Although the world’s economic problems are exacerbated by Trump’s tariffs, they’re not caused by them; the cause is too much debt combined with satiated consumption following a 10-year economic expansion. Meanwhile the Fed’s ongoing (until October) balance sheet contraction combined with a lack of European QE and a drastic reduction in Japanese QE will allow the deflation of the economic and asset bubbles those money-printing policies created, and the Fed’s anticipated rate cuts later this year will do little to prevent that.

Also, keep in mind that much of the U.S. bull market’s rise came from corporate buybacks, and those tend to slow drastically when the economy does. As the looming recession unfolds and those buyers disappear, look out below.

Seeking the most overvalued of all stock indices, we thus remain short the Russell 2000 (IWM), which has a trailing twelve-month GAAP PE ratio of 35 on what I believe are peak earnings, while 35% of its constituents lose money.

Elsewhere in the fund’s short positions…

We remain short stock and call options in Tesla, Inc. (TSLA), which I consider to be the biggest single stock bubble in this whole bubble market. The core points of our Tesla short thesis are:

- Tesla has no “moat” of any kind; i.e., nothing meaningfully proprietary in terms of electric car design or technology, while existing automakers—unlike Tesla—have a decades-long “experience moat” of knowing how to mass-produce, distribute and service high-quality cars consistently and profitably.

- Tesla is now a “busted growth story”; demand for its existing models has peaked and it will have to raise billions of dollars to produce new ones in a soon-to-be saturated market.

- Tesla is losing a ton of money with a terrible balance sheet while confronting massive competition in every aspect of its business.

- Elon Musk is extremely untrustworthy.

Tesla’s Q2 guidance is to sell 90-100,000 cars and while my own current guess is lower, at around 86,000 to perhaps as high as 88,000, due to 2019’s massive price-slashing (approximately six “official” cuts so far this year plus huge discounting on top of that), whatever the delivery number is, it will occur at by far Tesla’s lowest ASP ever.

Tesla reported a disastrous Q1, with a GAAP loss of $702 million (over $900 million excluding regulatory credit sales) on just 63,000 deliveries. My guess is that due to Q2’s much lower ASPs, it will have an average of around $4000/car in reduced gross profit on those first 63,000 cars (i.e., minus $252 million) while collecting only around $6000/car in incremental gross profit on the additional 23,000 Q2 cars sold (i.e., $138 million). Thus, all else being equal Tesla would lose an additional net of $114 million (-$252 million + $138 million) in Q2 vs Q1’s $702 million; i.e., an astounding loss of $840 million. However, the copmpany may be able to book some additional emissions credits and recognize some non-cash deferred Autopilot revenue, as well as avoid some one-time write-downs from Q1. So even if it comes up with $340 million of non-repeating Q2 cost reduction/revenue recognition vs. Q1, Tesla will still lose around $500 million GAAP in the quarter.

Whatever Q2 loss Tesla prints would be at least $100 million greater if the company were providing adequate customer service. Twitter is filled with complaints from aggrieved owners (some of them rather famous) who can’t reach anyone to fix their myriad problems within a reasonable timeframe. Although this is resulting in true brand destruction, due to the high cost of batteries Teslas are inherently unprofitable, and thus improving the ownership experience would only increase the losses. In other words, Tesla is truly a non-viable business.

The party’s over, folks. With no profitable growth, massive ongoing losses and tens of billions of dollars in debt and purchase obligations, the equity in Tesla will prove worthless, either quickly or—following a series of increasingly ugly capital raises—slowly. And yet as the stock is currently still over $200/share, I shall continue…

With most of the pent-up demand for cheaper models fulfilled in Q2 along with an $1875 cut in the U.S. tax credit on July 1, I expect a large slide in Q3 & Q4 deliveries, with Tesla showing declines both sequentially and year-over-year vs. Q3 and Q4 2018. (Things would be even worse in Q3 if Tesla didn’t have several years of the UK’s right-hand-drive Model 3 backlog to fill, which it plans to do in the quarter.) Thus full-year Tesla deliveries will be only around 300,000 vs. guidance of 360,000 to 400,000 and the full-year GAAP loss will be egregiously bad—most likely well over $2 billion.

And for those of you looking for a resumption of growth from Tesla’s (supposedly) upcoming Model Y, by the time it’s available in late 2020 or 2021 (if Tesla is still in business), it will face superior competition from the much nicer Audi Q4 e-tron, BMW iX3, Mercedes EQB and Volvo XC40, while less expensive and available now are the excellent new all-electric Hyundai Kona and Kia Niro, extremely well reviewed small crossovers with an EPA range of 258 miles for the Hyundai and 238 miles for the Kia, at prices of under $30,000 inclusive of the $7500 U.S. tax credit. Meanwhile, the Model 3 sedan will have terrific direct competition in 2020 from Volvo’s beautiful new Polestar 2.

And if you think China will be the saving grace for Tesla, I have bad news for you: not only is the competition there for EV market share becoming a vicious dogfight (see all the links below) but Beijing is now switching its subsidies to hydrogen fueled cars, which it perceives as better than EVs.

Early in May $TSLA did an ugly convertible debt and equity deal to plug a hole in a very leaky bucket, netting approximately $2.3 billion which—on the back of my envelope—means it will still be completely out of cash by year-end, and thus will have raise more money in Q3 with its back against the wall on terms that are even uglier.

Meanwhile, Tesla has the most executive departures (and semi-departures) I’ve ever seen from any company, a dubious achievement that continued in full-force in June with the exit of its much heralded head of production; here’s the astounding full list of escapees. These people aren’t leaving because things are going great (or even passably) at Tesla; rather, they’re likely leaving because Musk is either an outright crook or the world’s biggest jerk to work for (or both). Could the business (if not the stock price) be saved in its present form if he left? Nope, it’s too late. Even if Musk steps down in favor of someone who knows what he’s doing, emerging competitive factors (outlined in great detail below) and Tesla’s balance sheet make the company too late to “fix” without major financial and operational restructuring.

In May Consumer Reports completely eviscerated the safety of Tesla’s so-called “Autopilot” system; in fact, Teslas have far more pro rata (i.e., relative to the number sold) deadly incidents than other comparable new luxury cars; here’s a link to those that have been made public. Meanwhile Consumer Report’s annual auto reliability survey ranks Tesla 27th out of 28 brands and the number of lawsuits of all types against the company continues to escalate-- there are now well over 600!

So here is Tesla’s competition in cars (note: these links are regularly updated)…

- The Audi e-tron: Electric Has Gone Audi

- Audi e-tron Sportback comes early 2020

- AUDI E-TRON GT FIRST DRIVE: LOOK OUT, TESLA (available 2020)

- Audi's Q4 e-tron previews entry-level EV for 2021

- Porsche Electric Taycan Launches Late 2019

- Porsche Taycan Cross Turismo to launch in 2020 after Taycan Sedan

- The next generation of the Porsche Macan will be electric

- THE AWARD-WINNING ALL-ELECTRIC JAGUAR I‑PACE

- THE NEW ALL-ELECTRIC JAGUAR I‑PACE

- Jaguar Land Rover readies electric XJ and Range Rover

- VW Names 2020 Fully Electric Hatchback ID 3, starts taking deposits in Europe

- VW Group to launch 70 pure electric cars over the next decade

- Mercedes EQC Electric SUV Available Mid-to-Late 2019

- Mercedes EQB Small SUV to boost brand's electric line-up

- Mercedes to launch more than 10 all-electric models by 2022

- 258-Mile Hyundai Kona electric is available now for under $40,000

- 239-Mile Kia Niro EV is Available Now For Under $40,000

- Kia Soul (available mid-2019) EV’s Range Jumps to 243 Miles

- Kia Europe to have six pure electric models by 2022

- Chevrolet Bolt Offers 238 Miles On A Single Charge

GM is transforming Cadillac into an electric brand - Nissan LEAF e+ with 226-mile range is available now

- Nissan Leaf-based SUV coming in 2020

- The 2020 Volvo Polestar 2 Is Priced to Beat Tesla’s Best-Selling Model 3

- Volvo XC40 full-electric variant to debut later this year

- BMW iX3 electric crossover goes on sale in 2020

- New BMW i4: Tesla-rivalling coupe seen winter testing

- BMW is accelerating electrification plans – 23 electrified models by 2023

- Ford’s Mustang-inspired electric performance SUV arrives in 2020 with >300-mile range

- Ford Accelerates Its Electric-Vehicle Push With $500 Million Stake in Rivian

- Rivian (electric pick-up truck maker) Announces $700M Investment Round Led By Amazon

- Toyota to market over 10 battery EV models in early 2020s

- Renault upgrades Zoe electric car as competition intensifies

- Peugeot 208 to electrify Europe's small-car market

- Peugeot to offer EV version of new 2008 small crossover

- Toyota and Subaru Agree to Jointly Develop BEV-dedicated Platform and BEV SUV

- Mazda counts on EVs to reach EU CO2 goal

- Infiniti will go mostly electric by 2021

- DS 3 Crossback will give PSA's upscale brand an electric boost

- Smart Will Electrify Its Entire Line-up By 2020

- SEAT will launch 6 electric and hybrid models and develop a new platform for electric vehicles

- Opel sees electric Corsa as key EV entry

- Opel/Vauxhall will launch electric SUV and van in 2020

- 2019 Skoda e-Citigo confirmed as brand's first all-electric model

- Skoda planning range of hot all-electric eRS models

- New Citroen C4 Cactus to be first electrified Citroen in 2020

- MG E-Motion confirms new EV sports car on the way by 2020

- Fiat Chrysler bets on electrification for Alfa, Jeep and Maserati

- Rolls-Royce is preparing electric Phantom for 2022

- Honda will offer full-EV or hybrid tech on every European model by 2025

- Bentley mulls electric car to help reduce carbon footprint

- Korando will lead SsangYong's push into electrification

- Dyson electric car: new patents show mould-breaking design

- Lucid Motors closes $1 billion deal with Saudi Arabia to fund electric car production

- Borgward BXi7 Electric SUV Flies Under The Radar

- Detroit Electric promises 3 cars in 3 years

- Two new electric cars from Mahindra in India by 2019; Global Tesla rival e-car soon

- Saab asset owner NEVS plans electric car production

- EV startup Canoo will only sell cars on a subscription basis

And in China…

- VW, China spearhead $300 billion global drive to electrify cars

- Audi Q2L e-tron debuts at Auto Shanghai

- Audi will build Q4 e-tron in China

- Audi China to roll out 12 locally-produced models in total by 2022

- BYD launches EV535, all-electric SUV

- BYD Song MAX BEV version with 500km range to hit market in 2019

- 2019 BYD Yuan EV360 goes on sale with prices starting RMB89,900 after subsidy

- BYD e2 all-electric crossover rolls off production line in Changsha

- Top of Form

- Bottom of Form

- Daimler & BYD launch new DENZA electric vehicle for the Chinese market

- BAIC and Daimler to Build $1.9 Billion China Plant

- BAIC brings EX5 Electric SUV to market

- BAIC BJEV, Magna ready to pour RMB2 bln in all-electric PV manufacturing JV

- Daimler to Start EQC Electric SUV Production in China in 2019

- Daimler and BMW to cooperate on affordable electric car in China

- BMW will develop and produce electric Mini in China

- GM China raises new-energy vehicle target to 20 models through 2023

- Buick Rolls Out First Electric Car for China

- Nissan & Dongfeng to invest $9.5 billion in China to boost electric vehicles

- Toyota partners with China's CATL to power electric ambitions

- Toyota unveils first electric SUVs at Shanghai motor show

- Nio’s ES8 Electric Crossover debuts with half the Tesla Model X’s price tag

- Nio begins deliveries of new ES6 electric crossover in China (at 1/2 the price of Tesla X)

- This is NIO’s Tesla Model 3 and Polestar 2 rival

- GAC NIO unveils new NEV offshoot dubbed HYCAN

- GAC NE to roll out 12 new models for Aion series, including solar-powered models

- Ford ramps up electric vehicle push in China

- Jaguar Land Rover's Chinese arm invests £800m in EV production

- SAIC building factory in China for EVs from Roewe and MG

- Renault and Brilliance Automotive to build 3 new electric light commercial vehicles for China

- Honda launches new all-electric Everus VE-1 for ~$25,000 in China

- Honda to roll out over 20 electric models in China by 2025

- Geely all-new BEV sedan Jihe A starts at RMB150,000

- Geely unveils GE11 compact BEV

- New Geely Emgrand GSe crossover has EV range up to 400km

- Geely launches new electric car brand 'Geometry'

- Changan New Energy to launch three NEV platforms by 2020

- Mazda and Changan Auto join hands on electric vehicles

- Xpeng Motors G3 Electric SUV Launches in China

- Xpeng Motors premiers the P7 intelligent electric coupe

- WM Motors/Weltmeister EX5 Electric SUV Launched On The Chinese Car Market

- Chery Breaks Ground on $240M EV Factory in China

- Chery's second EV plant open in Dezhou

- Seres launches production SF5 sleek 684HP electric crossover with 300 miles of range

- Byton M-Byte electric SUV tackles cold-weather testing, nears production

- DearCC Launches ENOVATE Electric SUV

- Guangzhou Auto To Launch Four New Electric Cars By 2020

- Great Wall Launches New EV Brand (ORA) In China

- Singulato iS6 Electric SUV Debuts With 249-Mile Range

- Singulato, BAIC partner to promote smart new energy vehicles

- Hongqi launches E-HS3 BEV SUV with AWD option, 390km range and 0-100kh/h in 5.9 seconds

- FAW (Hongqi) to roll out 15 electric models by 2025

- JAC Motors releases new product planning, including many NEVs

- Seat to make purely electric cars with JAC VW in China

- ICONIQ to build electric cars in Zhaoqing with total investment of RMB 16 billion

- Quianu Motor aims to grab share of US electric vehicle market

- Hozon Kicks Off Mass Production With All-Electric Neta N01

- EV maker Bordrin skips flash, keeps real-car focus

- Aiways U5 long-range electric SUV

- All-electric NEVS 9-3 sedans (nee Saab) being built in China

- Youxia Motors raises $1.25 billion to start 2019 EV production

- CHJ Automotive buys Lifan for shortcut to EV production

- Infiniti to launch Chinese-built EV in 2022

- Zotye Auto to roll out 10 plus NEV models by 2020

- Wanxiang Gets China Electric Vehicle Permit to Make Karma Cars

- Qoros Auto's new owner plans to be an EV power

- JMC (Jianling Motor Corp.) Starts New EV Brand In China

- Thunder Power Chinese EV manufacturer clinches deal with Belgian investment fund

- Leapmotor raises RMB2.5 billion for Series A round to build electric cars

- Continental, Didi sign deal on developing EVs for China

Here’s Tesla’s competition in autonomous driving…

- Consumer Reports finds Tesla's Navigate on Autopilot is far less competent than a human driver

- Navigant Ranks Tesla Last Among Automakers & Suppliers for Automated Driving

- Tesla has a self-driving strategy other companies abandoned years ago

- Waymo and Lyft partner to scale self-driving robotaxi service in Phoenix

- Jaguar and Waymo announce an electric, fully autonomous car

- Renault, Nissan partner with Waymo for self-driving vehicles

- Fiat Chrysler partners with Aurora to develop self-driving commercial vans

- Hyundai and Kia Invest in Aurora

- Cadillac Super Cruise™ Sets the Standard for Hands-Free Highway Driving

- Honda Joins with Cruise and General Motors to Build New Autonomous Vehicle

- SoftBank Vision Fund to Invest $2.25 Billion in GM Cruise

- Ford and VW near self-driving deal

- VW taps Baidu's Apollo platform to develop self-driving cars in China

- An Overview of Audi Piloted Driving

- Daimler, BMW deepen cooperation with self-driving venture

- Mercedes plans advanced self-driving tech for next S class

- Daimler's heavy trucks start self-driving some of the way

- SoftBank, Toyota's self-driving car venture adds Mazda, Suzuki, Subaru Corp, Isuzu Daihatsu

- Volvo, Nvidia expand autonomous driving collaboration

- Continental & NVIDIA Partner to Enable Production of Artificial Intelligence Self-Driving Cars

- Intel’s Mobileye has 2 million cars (VW, BMW & Nissan) on roads building HD maps

- Nissan and Mobileye to generate, share, and utilize vision data for crowdsourced mapping

- Magna joins the BMW Group, Intel and Mobileye platform as an Integrator for AVs

- Uber unveils next-generation Volvo self-driving car

- Toyota to join Baidu's open-source self-driving platform

- Baidu, WM Motor announce strategic partnership for L3, L4 autonomous driving solutions

- Baidu plans to mass produce Level 4 self-driving cars with BAIC by 2021

- Volvo, Baidu to co-develop EVs with Level 4 autonomy for China

- Geely selects Volvo, Veoneer joint venture as autonomous tech supplier

- Huawei looks to self-driving cars in bid to broaden AI focus

- BYD partners with Huawei for autonomous driving

- Lyft, Magna in Deal to Develop Hardware, Software for Self-Driving Cars

- Deutsche Post to Deploy Test Fleet Of Fully Autonomous Delivery Trucks

- Byton cooperating with Aurora on autonomous vehicles

- ZF autonomous EV venture names first customer

- Magna’s new MAX4 self-driving platform offers autonomy up to Level 4

- Groupe PSA’s safe and intuitive autonomous car tested by the general public

- Apple acquires self-driving startup Drive.ai

- Tencent, Changan Auto Announce Autonomous-Vehicle Joint Venture

- Self-driving startup Momenta ready to launch fully automated driving solution in Q3 2019

- JD.com Delivers on Self-Driving Electric Trucks

- NAVYA Unveils First Fully Autonomous Taxi

- Fujitsu and HERE to partner on advanced mobility services and autonomous driving

- Lucid Chooses Mobileye as Partner for Autonomous Vehicle Technology

- First Look Inside Zoox’s Autonomous Taxi

- Nuro’s Robot Delivery Vans Are Arriving Before Self-Driving Cars

Here’s Tesla’s competition in car batteries…

- LG Chem targets electric car battery sales of $6.3 billion in 2020

- LG Chem to build $1.8 bln EV battery plant in China

- Samsung SDI Unveils Innovative Battery Products at 2018 Detroit Motor Show

- SK Innovation to boost EV battery production capacity more than tenfold by 2022

- New Toshiba EV Battery Allows 320km Charge in 6 Minutes

- Daimler starts building electric car batteries in Tuscaloosa – one of 8 battery factories

- Panasonic Opens New Automotive Lithium-Ion Battery Factory in Dalian, China

- Panasonic forms battery partnership with Toyota

- CATL’s Chinese battery factory will be bigger than Tesla’s Gigafactory

- CATL to set up battery cell manufacturing in Germany

- BYD to quadruple car battery output with lithium site plants

- GM inaugurates battery assembly plant in Shanghai

- VW, BMW invest in Swedish battery cell producer Northvolt

- Volkswagen building battery cell plant in Germany

- VW Wants to One-Up Tesla With a Next-Generation Battery

- Toyota accelerates target for EV with solid-state battery to 2020

- PSA to assemble batteries for hybrid, electric cars in Slovakia

- Honda Partners on General Motors' Next Gen Battery Development

- Energy Absolute Plots Asian Project Rivaling Musk's Gigafactory

- France's Saft plans production of next-gen lithium ion batteries from 2020

- FREYR AS to build a 32 GWh battery facility in Norway

- Chinese Battery Maker to Open Factory Next to Swedish EV Plant

- Sokon aims to be global provider of battery, electric motor, electric control systems

- BMW Group invests 200 million euros in Battery Cell Competence Centre

- BMW Brilliance Automotive opens battery factory in Shenyang

- BMW announces partnership with solid-state battery company

- Hyundai Motor developing solid-state EV batteries

- Wanxiang is playing to win, even if it takes generations

- UK provides millions to help build more electric vehicle batteries

- Rimac is going to mass produce batteries and electric motors for OEMs

- Elon Musk Has A New Battery Rival (Romeo Power) Packed With His Ex-Employees

- Evergrande acquires Cenat battery production

- Bracing for EV shift, NGK Spark Plug ignites all solid-state battery quest

- ProLogium Technology Will Produce First Next Generation Lithium Ceramic Battery For EVs

Here’s Tesla’s competition in charging networks…

- Electrify America: Our Plan

- EVgo Installing First 350 kW Ultra Fast Public Charging Station In The US

- Tritium’s First 350-kW DC Fast Chargers Coming To U.S.

- Porsche plans network of 500 fast chargers for U.S.

- ChargePoint To Equip Mercedes Dealerships With 150kw Charging Stations For EQC

- Recargo Ultrafast West Coast Charging

- GM and Bechtel plan to build thousands of electric car charging stations across the US

- BMW, Daimler, Ford, VW, Audi & Porsche form IONITY European 350kw Charging Network

- E.ON to have 10,000 150KW TO 350KW EV charging points across Europe by 2020

- Volkswagen plans 36,000 charging points for electric cars throughout Europe

- Enel kicks off the E-VIA FLEX-E project for the installation of European ultra-fast charging stations

- Europe’s Allego “Ultra E” ultra-fast charging network now operational

- Allego & Fortum Launch MEGA-E High Power Charging network for Europe’s Metropolitan areas

- ChargePoint Secures $240 Million in Additional Funding; $500 million raised in total

- UK's Podpoint installing 150kW EV rapid chargers this year; 350kW by 2020

- UK National Grid plans 350kW EV charge point network

- BP Chargemaster’s 150kW UK network to allow 30min electric car charging at 50 sites this year

- Fastned building 150kw-350kw chargers in Europe

- Deutsche Telekom to build electric car charging network in Germany

- ABB powers e-mobility with launch of first 150-350 kW high power charger

- Shell buys European electric vehicle charging pioneer NewMotion

- Total planning EV charging points at its French stations

- VW Is Setting Up Electric Car Charging Stations in China

And here’s Tesla’s competition in storage batteries…

- Panasonic

- Samsung

- LG

- BYD

- AES + Siemens (Fluence)

- GE

- Bosch

- Mitsubishi Hitachi

- NEC

- Toshiba

- ABB

- Saft

- Johnson Contols

- EnerSys

- SOLARWATT

- Schneider Electric

- sonnenBatterie (acquired by Shell)

- Kyocera

- Kokam

- Sharp

- Eaton

- Nissan

- Tesvolt

- Kreisel

- Leclanche

- Lockheed Martin

- EOS Energy Storage

- ESS

- UET

- electrIQ Power

- Belectric

- Stem

- ENGIE

- Exergonix

- Redflow

- Renault

- Fluidic Energy

- Primus Power

- Simpliphi Power

- redT Energy Storage

- Murata

- Bluestorage

- Adara

- Blue Planet

- Clean Energy Storage Inc.

- Tabuchi Electric

- Younicos

- Orison

- Moixa

- Powin Energy

- Nidec

- Powervault

- Schmid

- 24M

- Ecoult

- Innolith

- LithiumWerks

- Natron Energy

Yet despite all that deep-pocketed competition, perhaps you want to buy shares of Tesla because you believe in its management team. Really???

- Elon Musk Settles SEC Fraud Charges

- Elon Musk, June 2009: “Tesla will cross over into profitability next month”

- Tesla SEC Correspondence Shows A Pattern Of Inaccurate, Incomplete & Misleading Disclosures

- Tesla: Check Your Full Self-Driving Snake Oil Expiration Date

- As Musk Hyped and Happy-Talked Investors, Tesla Kept Quiet About a Year-Long SEC Probe

- The Truth Is Catching Up With Tesla

- With Misleading Messages And Customer NDAs, Tesla Performs Stealth Recall

- Who You Gonna Believe? Elon Musk's Words Or Your Own Lying Eyes?

- How Tesla and Elon Musk Exaggerated Safety Claims About Autopilot and Cars

- When Is Enough Enough With Elon Musk?

- Musk Talked Merger With SolarCity CEO Before Tesla Stock Sale

- Tesla Continues To Mislead Consumers

- Tesla Misses The Point With Fortune Autopilot Story

- Tesla Timeline Shows Musk's Morality Is Highly Convenient

- Tesla Scares Customers With Worthless NDAs, The Daily Kanban Talks To Lawyers

- Tesla: O, What A Tangled Web We Weave When First We Practice To Deceive

- I Put 20 Refundable Deposits On The Tesla Model 3

- Tesla's Financial Shenanigans

- Tesla: A Failure To Communicate

- Can You Really Trust Tesla?

- Elon Musk Appears To Have Misled Investors On Tesla's Most Recent Conference Call

- Understanding Tesla’s Potemkin Swap Station

So in summary, Tesla is losing a massive amount of money even before it faces a huge onslaught of competition (and things will only get worse once it does), while its market cap equals that of Ford and is over 70% of GM’s despite selling fewer than 300,000 cars a year while Ford and GM make billions of dollars selling 6 million and 8.4 million vehicles respectively. Thus this cash-burning Musk vanity project is worth vastly less than its over $50 billion enterprise value and—thanks to roughly $34 billion in debt, purchase and lease obligations—may eventually be worth “zero.”

Elsewhere among our short positions…

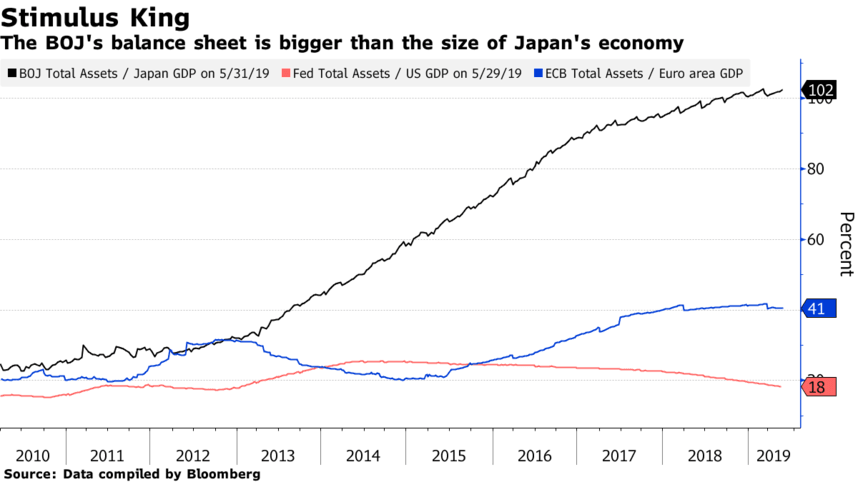

We continue (since late 2012) to hold a short position in the Japanese yen via the Proshares UltraShort Yen ETF (ticker: YCS) as Japan (despite having substantially tapered its QE) continues to print over 3% of its monetary base per year after quadrupling that base since early 2013. In 2018 the BOJ bought approximately 67% of JGB issuance and in 2019 it anticipates buying 70%! In fact, the BOJ’s balance sheet is now larger than the entire Japanese economy:

…and it owns nearly 78% (!) of the country’s ETFs by market value.

Just the interest on Japan’s debt consumes 8.9% of its 2019 budget despite the fact that it pays a blended rate of less than 1%. What happens when Japan gets the 2% inflation it’s looking for and those rates average, say, 3%? Interest on the debt alone would consume nearly 27% of the budget and Japan would have to default! But on the way to that 3% rate the BOJ will try to cap those rates by printing increasingly larger amounts of money to buy more of that debt, thereby sending the yen into its death spiral.

When we first entered this position USD/JPY was around 79; it’s currently in the 107s and long-term I think it’s headed a lot higher—ultimately back to the 250s of the 1980s or perhaps even the 300s of the ‘70s before a default and reset occur.

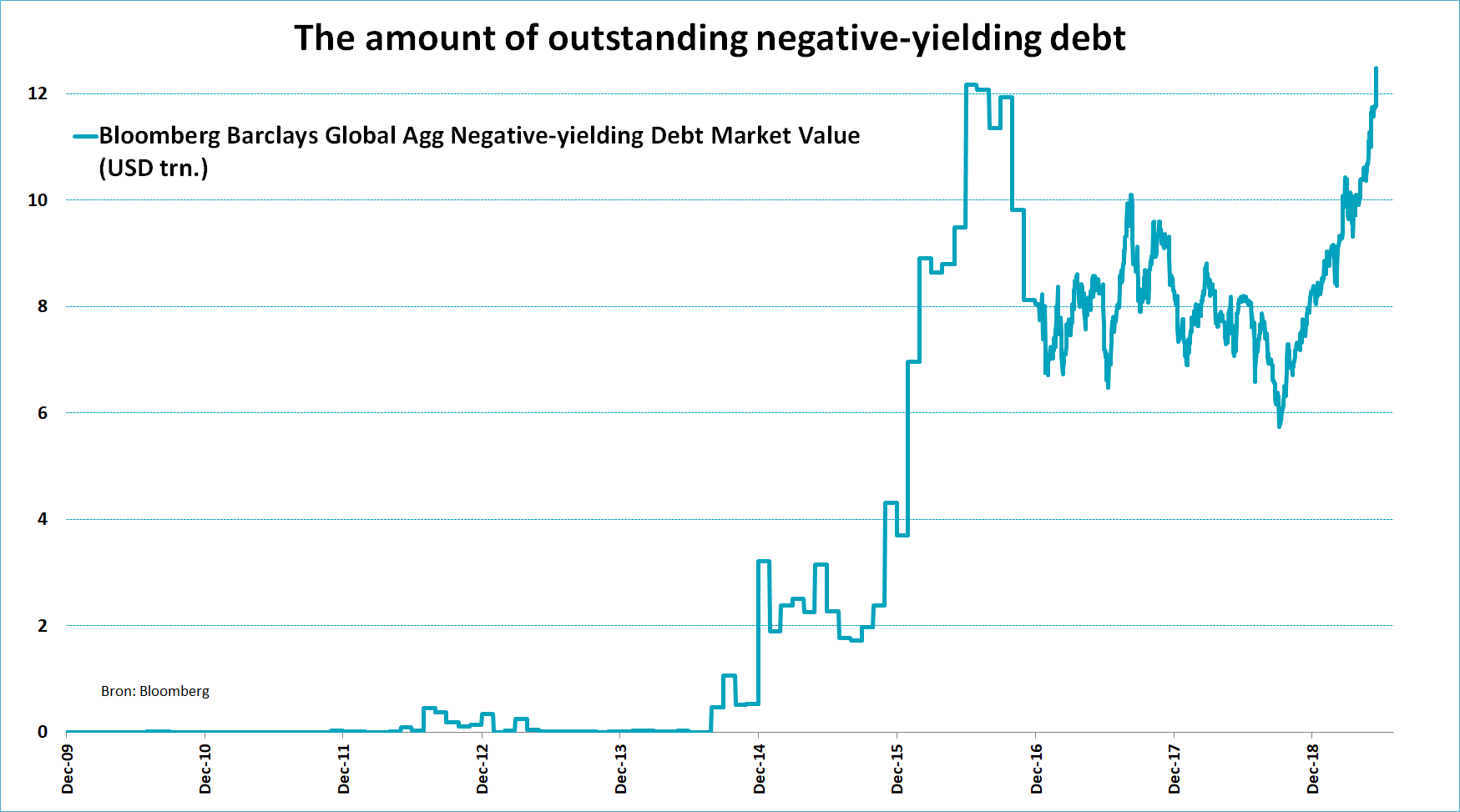

We continue to hold a short position in the Vanguard Total International Bond ETF (ticker: BNDX), comprised of dollar-hedged non-US investment grade debt (over 80% government) with a ridiculously low “SEC yield” of 0.67% at an average effective maturity of 9.6 years. As I’ve written since putting on this position in July 2016, I believe this ETF is a great way to short what may be the biggest asset bubble in history, as with Eurozone inflation now printing 1.2% annually these are long-term bonds with significantly negative real yields. In mid-December the ECB halted quantitative easing, thereby removing the biggest source of support for those bonds’ bubble prices. Currently the net borrow cost for BNDX provides us with a positive rebate of nearly 2% a year (more than covering the yield we pay out) and as I see around 5% potential downside to this position (vs. our basis, plus the cost of carry) vs. at least 20% (unlevered) upside, I think it’s a terrific place to sit and wait for the inevitable denouement of this insanity—over $12 trillion of negative-yielding debt:

We also have relatively small short positions in Netflix (NFLX) due to its egregious valuation within the context of increasing cash burn and competition (particularly from Disney), Square (SQ) due to its egregious valuation and a stock-dumping CEO who so effusively praises (and enables) Elon Musk that I suspect he’s equally untrustworthy (and indeed in June the company fired its auditor), Carvana (CVNA) due to a laughable business model with escalating losses and a founder with a sketchy past who’s dumping stock steadily and Wayfair (W), an egregiously bad on-line furniture business with yet another stock-dumping CEO.

And now for the fund’s long positions…

We continue to own Aviat Networks, Inc. (ticker: AVNW), a designer and manufacturer of point-to-point microwave systems for telecom companies, which in June reported an interesting deal to be the exclusive North American distributor for NEC’s microwave products. In May Aviat reported a lousy Q3 for FY 2019 (with revenue down 13% year-over-year), but guided to a very strong Q4 (ending June 30th) with revenue and income up substantially year-over-year. For all of FY 2019 the company cut guidance to $246-$251 million of revenue (a $4 million reduction from previous guidance) and non-GAAP EBITDA of $11-$12 million (a $1 million reduction), and because of its approximately $330 million of U.S. NOLs, $10 million of U.S. tax credit carryforwards, $214 million in foreign NOLs and $2 million of foreign tax credit carryforwards, Aviat’s income will be tax-free for many years; thus, GAAP EBITDA less capex essentially equals “earnings.” So if the non-GAAP number will be $11.5 million and we take out $1.7 million in stock comp and $6 million in capex we get $3.8 million in earnings multiplied by, say, 14 = approximately $53 million; if we then add in approximately $29 million of expected year-end net cash and divide by 5.4 million shares we get an earning-based valuation of around $15/share. However, the real play here is as a buyout candidate; Aviat’s closest pure-play competitor, Ceragon (CRNT) sells at an EV of approximately 0.6x revenue, which for AVNW (based on the low end of 2019 guidance) would be 0.6 x $246 million =$148 million + $29 million net cash = $177 million. If we value Aviat’s massive NOLs at a modest $10 million (due to change-in-control diminution in their value), the company would be worth $187 million divided by 5.4 million shares = just under $35/share.

We continue to own Westell Technologies Inc. (WSTL), which in May reported a terrible FY 2019 Q4, with revenue down 12.5% year-over-year and a drop in gross margin from 45.5% to 37.6% and negative free cash flow of around $1.4 million. About the only good news here is that the company ended the quarter with $25.5 million in cash and no debt, and (as gleaned from the conference call) normalized FCF burn at Q4’s revenue level is “only” around $900,000. Westell now sells at an enterprise value of only around 0.1x (i.e., 10% of) revenue, so on that metric it’s clearly dirt cheap but the business needs to stabilize and grow. On the conference call management was confident that later this year there should be enough revenue growth to cut quarterly burn to around $500,000 but “break-even” now sounds like more of a “next year” possibility. Westell also suffers from a dual share class with voting control held by descendants of the founder; however, management has often stated that the controlling family is open to merging the two share classes, and the company is so cheap on an EV-to-revenue basis that if management can’t start generating meaningful profits it seems primed for a strategic buyer to acquire it. An acquisition price of just 0.8x run-rate revenue (on an EV basis) would be around $3.70/share.

We continue to own the PowerShares DB Agriculture ETF (ticker: DBA) as agricultural products remain the most beaten-down sector I can find that isn’t a “buggy whip” (something on the way to obsolescence) or cyclical from a demand standpoint. Additionally, if a trade deal with China is made the implications for U.S. ag products would be huge, and meanwhile disastrous weather in the farm belt may be an additional near-term catalyst.

Thanks and regards,

Mark Spiegel