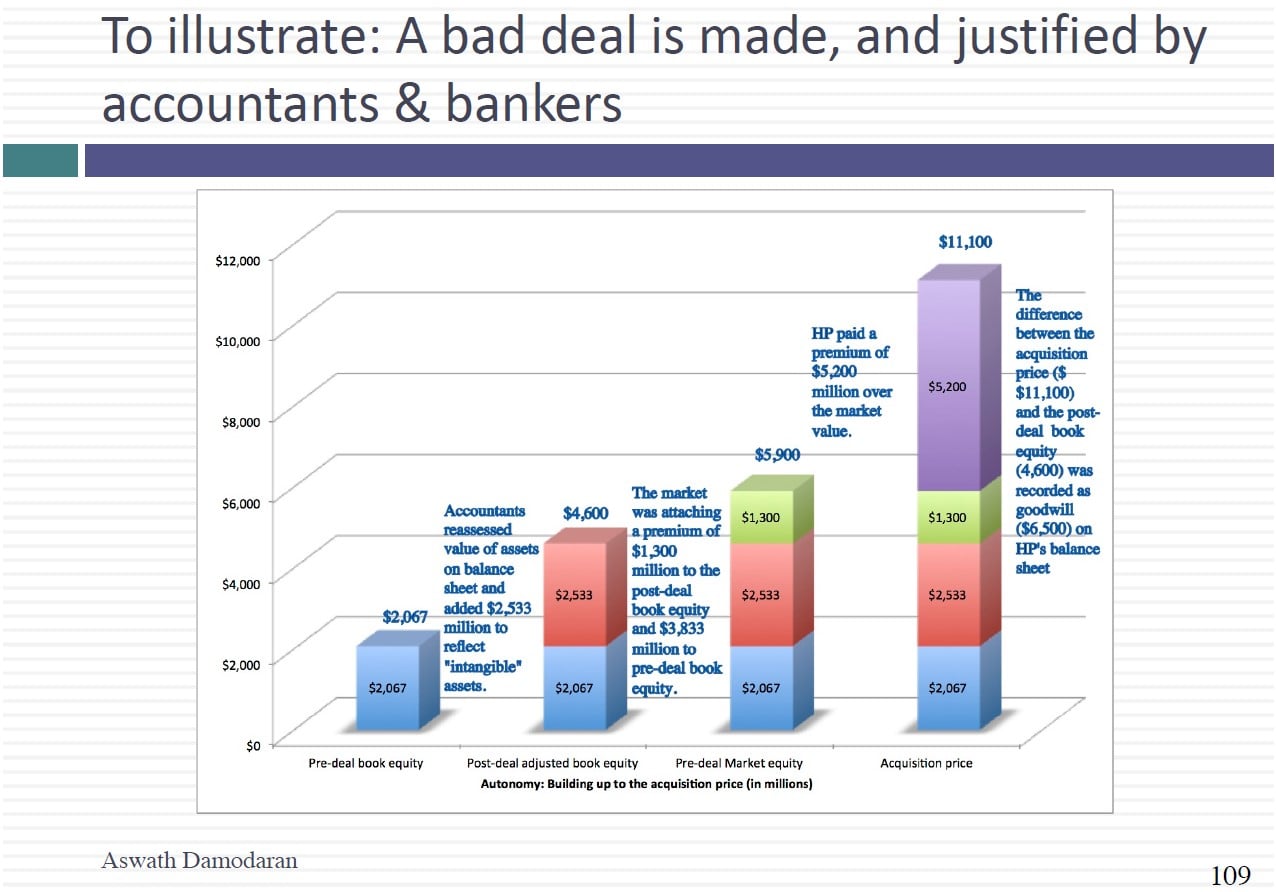

Acquisitions are exciting and fun to be part of but they are not great value creators and in this sessions, I tried to look at some of the reasons. While the mechanical reasons, using the wrong discount rate or valuing synergy & control right, are relatively easy to fix, the underlying problems of hubris, ego and over confidence are much more difficult to navigate. There are ways to succeed, though, and that is to go where the odds are best: small targets, preferably privately held or subsidiaries of public companies, with cost cutting as your primary synergy benefit. If you get a chance, take a look at a big M&A deal and see if you can break it down into its components. I did get briefly into the InBev/SABMiller merger in class but if you want something more extensive, I am going to offer you the blog post that I did on it when it happened: http://aswathdamodaran.blogspot.com/

Slides: http://www.stern.nyu.edu/

Session 24: Acquisition Valuation

Q1 hedge fund letters, conference, scoops etc

Transcript

So today we're going to actually talk about acquisition valuation and rather than have a start of the class. Yes I'm going to have a test that runs all the way through the session. I know whether you got a chance to look at the questions but even if you didn't. Not a big deal because the numbers are actually so simple you could probably answer them as we go along. So I'm going to play to essentially take you through an acquisition and use the acquisition to illustrate some of the estimation the valuation issues. As somebody once asked me to teach and I'm in a class and I said What would I teach after the first 30 minutes I'd run out of stuff to say because we look at how many class is all about institutional detail about the process of our money because the valuation of an MBA is no different than value any other company. So yes what we're going to do we're going to start with a very simple company it's a potential target company let's value the target company as a standalone company for us. I promise you the numbers would be so simple you don't have to pull out the calculator and I'll deliver on my promise. So here's what the numbers look like. This company is expected to have revenues of one hundred million next year. Operating income of 20 million in an after tax operating income of 12 million.

So that's going to be next year's numbers. Assume this company can generate this operating income every year forever. And there's no growth. So it's basically twelve million every year in perpetuity. It's all equity funded.

And it's cost of equity is 20 percent so it's value the company. Sixty right. What do you do. You took the OK. So how come we didn't have to subtract our net CapEx and change in working capital don't we have to do that.

I mean you're not allowed to just discount operating income after taxes. What in this problem allows you to treat the after tax operating income as your cash flow. There is no growth. That is the Key Club. You have no growth then you don't need to reinvest. If I put a growth rate in there. Then what else would I need to give you for you to devalue the company. I'd need to give you the return on capital this company owns in perpetuity because without it you're going to be lost. But without growth you're saying well you know what. I can just. So there is a net CapEx and a change what can happen in this case because the growth is zero. I'm assuming those numbers are zero. Twelve million enough. So 60 million everybody agree with that. So because we don't agree with that everything else after this is going to be complete chaos. So we've got the 60 million. So here's the first thing I'm going to try. I'm a deal maker. You're an acquiring company. I'm going to try to get you to buy the target company let's say if you bite so you're a very safe acquiring company. In fact your cost of equity is only 10 percent. You're in a much safer business. I come to you at the target company same target company with valued a page ago.

What's a valued target company to you still at 60 see the question I'm posing for you right. When you value the target company whose cost of equity should you use and we kind of dealt with this very early in this class we're going to revisit it so the right answer is 60 everybody agree. So let me play devil's advocate because half of all acquisitions you know the acquiring company's cost of equity is to vary the target company you're going to run into one of those guys or girls six months from now you're gonna be in this argument about hey you know I learned in my valuation class we should use the target company and the person to want to push back and say I'll play the devil's advocate. I am raising the capital as the acquiring company my cost of equity is 10 percent why shouldn't I use my 10 percent as my discount. Because that's going to give me value twice as large right. 120 million so leave me through the intuition the logic as to why I should not use my cost of equity to value the target company.

You want to try. Why shouldn't I use the cost of equity.

Well I'll raise the capital. You know the market so the market I don't even know. I may even have the capital already. So let's raise the capital. Why shouldn't I use my cost of equity is what I raise the capital at as my discount rate to value the target company. In fact we're going to corporate finance one to one right in capital budgeting. You know the discount rate for a project should be it should reflect the risk of the project not the risk of the company taking the project. You know how often that rule is violated every single day. You know why. Because companies think of a corporate cost of capital a corporate hurdle rate. And the minute you say that then what do you assume. Well that's what it costs me to raise money why shouldn't I use it in every project.

But lead me to what would happen if I decide to use as a safe company might cost of equity to value target companies. What's going to happen if.

Or I'll pay more that it's not even that it's more expensive I'll pay more and I'll do this only for rescue companies are are for companies which types of companies are going to keep looking cheap to me the riskier the company so I'm going to be by a risk.