Gold got a boost today on weaker-than-expected inflation and retail sales figures, which casts doubt on the Federal Reserve’s ability to continue normalizing interest rates this year.

Consumer prices rose slightly in June, at their slowest pace so far this year. The consumer price index (CPI), released today, showed the cost of living in America rising only 1.6 percent compared to the same month last year, significantly down from the most recent high of 2.8 percent in February and below the Fed’s target of 2 percent. Much of the decline was due to energy prices, which fell 1.6 percent from May.

As I’ve explained elsewhere, CPI is an important economic indicator for gold investors to track. The yellow metal has historically responded positively when inflation rises—and especially when it pushes the yield on a government bond into negative territory. Why lock your money up in a 2-year or 5-year Treasury that’s guaranteed to give you a negative yield?

|

But right now the gold Fear Trade is being supported by what some are calling turmoil in the Trump administration. This week the Russia collusion story took a new twist, with emails surfacing showing that Donald Trump Jr.; Jared Kushner, the president’s son-in-law and now-senior advisor; and former Trump campaign manager Paul Manafort all agreed to meet with a Russian lawyer last summer under the pretext that she had dirt on Hillary Clinton.

Whether or not this meeting is “collusion” is not for me to say, but the optics of it certainly look bad, and it threatens to undermine the president’s agenda even more. For the first time this week, an article of impeachment was formally introduced on the House floor that accuses Trump of obstructing justice. The article is unlikely to go very far in the Republican-controlled House, but it adds further uncertainty to Trump’s ability to achieve some of his goals, including tax reform and infrastructure spending. I’ll have more to say on this later

A Contrarian View of China

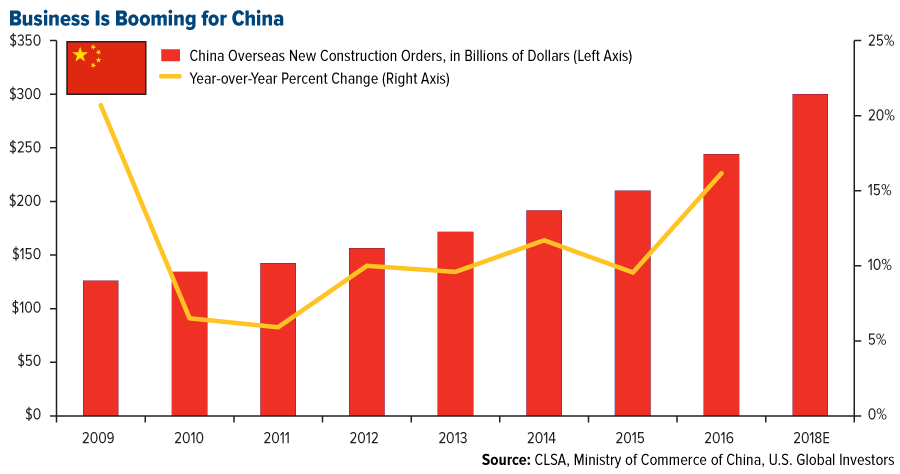

A new report this week from CLSA shows that Asian markets and Europe were the top performers during the first six months of the year. Korea took the top spot, surging more than 25 percent, followed closely by China.

Despite persistent negative “news” about China in the mainstream media, conditions in the world’s second-largest economy are improving. Consumption is up and household income remains strong. The number of high net worth individuals (HNWIs) in China—those with at least 10 million renminbi ($1.5 million) in investable income—rose to 1.6 million last year, about nine times the number only 10 years ago. It’s estimated we could see as many as 1.87 million Chinese HNWIs by the end of 2017.

According to CLSA, global trade is robust, with emerging markets, and particularly China, driving most of the acceleration this year. In the first three months of 2017, global trade grew 4 percent compared to the same period last year, its fastest pace since 2011.

“Indeed the early months of 2017 have seen China become easily the biggest single country driver of Asian trade growth,” writes Eric Fishwick, head of economic research at CLSA.

A lot of this growth can be attributed to Beijing’s monumental One Belt, One Road infrastructure project, which I’ve highlighted many times before. But according to Alexious Lee, CLSA’s head of China industrial research, a “more nationalist America” in the first six months of the year has likely given China more leverage to assume “a larger global, and especially regional, leadership role.”

This comports with what I said back in January, in a Frank Talk titled “China Sets the Stage to Replace the U.S. as Global Trade Leader.” With President Donald Trump having already withdrawn the U.S. from the Trans-Pacific Partnership (TPP) and promising to renegotiate or tear up other trade agreements—he recently tweeted that the U.S. has “made some of the worst Trade Deals in world history”—China has emerged, amazingly, as a champion of free trade, a position of power it will likely continue to capitalize on.

The country’s overseas construction orders have continued to expand, with agreements signed since 2013 valued at more than $600 billion.

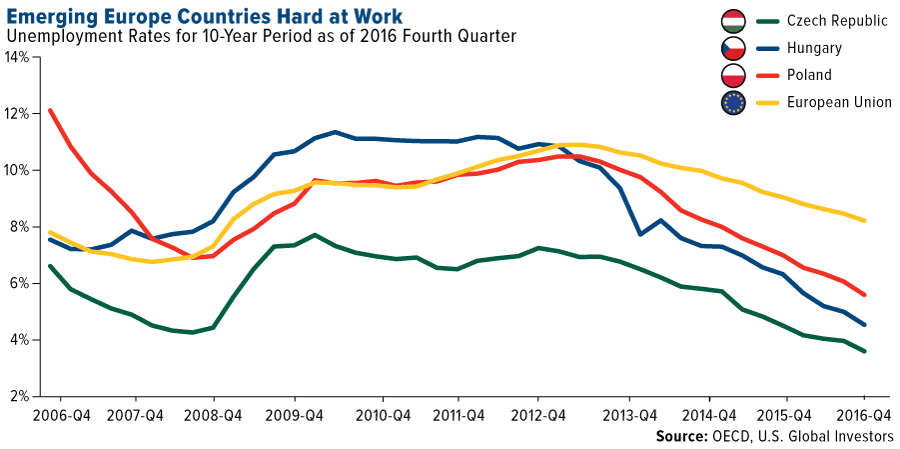

Emerging Europe Expected to Remain Strong

Another recent report, this one from Capital Economics, shows that the investment case for emerging Europe remains strong in 2017. Russia is expected to strengthen over the next 12 months, while Poland, Hungary, the Czech Republic and Slovakia are likely to remain attractive.

“Russia’s economy has pulled out of recession and growth in the coming quarters will be stronger than most anticipate,” the research firm writes, adding that its central bank’s loosening of monetary policy should support the recovery even further.

To be sure, the region faces strong headwinds, including a rapidly aging population and the loss of an estimated 20 million skilled workers to foreign markets over the past 25 years, according to a July 11 presentation from the International Monetary Fund (IMF).

But I believe that as conditions in central emerging Europe countries continue to improve, many of those workers will be returning home. Life in the region is not the same as it was 10 or 20 years ago, when good jobs might have been scarce. Firms are now growing at a healthy rate and hiring more workers. As you can see below, unemployment rates in Poland, Hungary and the Czech Republic have been falling steadily since at least 2012 and are now lower than the broader European Union.

This strength is reflected in emerging Europe’s capital markets. For the 12-month period as of July 12, Hungary’s Budapest Stock Exchange is up 38 percent. Poland’s WIG20 is up more than 43 percent. Meanwhile, the STOXX Europe 600 Index—which includes some of the largest Western European companies—has made gains of only 17 percent over the same period.

Markets Still Believe in Trump

As we all know, the mainstream media’s criticism and ire aren’t reserved for China alone. Ninety-nine percent of the media right now is against President Trump, for a number of reasons—some of them deserved, some of them not.

Markets, however, seem not to care what the media or polls have to say. The Dow Jones Industrial Average continues to hit new all-time highs. Even though it’s stalled a few times, the “Trump rally” appears to be in full-speed-ahead mode, more than eight months after the election.

Back in November, I wrote about one of my favorite books, James Surowiecki’s The Wisdom of Crowds, which argues that large groups of people will nearly always be smarter and better at making predictions than an “elite” few. Surowiecki’s ideas were vindicated last year when investors accurately predicted Trump’s election, with markets turning negative between July 31 and October 31.

For the same reason, I think it’s important we pay close attention to what markets are forecasting today.

The White House is under siege on multiple fronts, which, as I said, has been positive for gold’s Fear Trade. But equity investors also seem to like the direction Trump is taking, whether it’s pushing for tax reform and deregulation or shaking up the “beltway party,” composed of deeply entrenched D.C. lobbyists and career bureaucrats. Just this week, the president made waves for firing a number of bureaucrats at the Department of Veteran Affairs (VA), long plagued by scandal and controversy. Since he took office in January, Trump has told more than 500 VA workers “You’re fired!”

The Fundamentals of “Quantamental”

Of course, we look at so much more than government policy when making investment decisions. We take a blended approach of not only assessing fundamentals such as market share and returns on capital but also conducting quantitative analysis.

It’s this combination that some in the industry are calling “quantamental” investing. At first glance, “quantamental” might sound like nothing more than cute wordplay—not unlike “labsky,” “bullmation” and other clever names we give mixed-breed dogs—but it’s rapidly replacing traditional investment strategies at the institutional level.

Business Insider puts it in simple terms: “Quantamental managers combine the bottom-up stock-picking skills of fundamental investors with the use of computing power and big-data sets to test their hypotheses.”

See my Vancouver Investment Conference presentation, “What’s Driving Gold: The Invasion of the Quants,” to learn more about how we use quantitative analysis, machine learning and data mining.

Wall Street: The Birthplace of American Capitalism and Government

The concept of quantamentals helps explain our entry into smart-factor ETFs. As most of you already know, members of my team and I visited the New York Stock Exchange (NYSE) two weeks ago to mark the launch of our latest ETF.

While there, Doug Yones, head of exchange-traded products at the NYSE, gave us a short history lesson about the exchange and surrounding area.

Most investors are aware that the NYSE, which is celebrating its 225th anniversary this year, is the epicenter of capitalism—not just in the U.S. but also globally.

What many people might not realize is that on the site where the exchange now stands, Alexander Hamilton, the first U.S. treasury secretary, floated bonds to replace the debt the nascent country had incurred during the Revolutionary War.

Right next door to the NYSE is Federal Hall, where George Washington took his first oath of office in April 1789. The building today serves as a museum and memorial to the first U.S. president, whose statue now looks out over Wall Street and its passersby.

In this one single block of Wall Street, therefore, American capitalism and government were born. Here you can find the essential DNA of the American experiment, which, over the many years, has fostered our entrepreneurial spirit to form capital and to create new businesses and jobs. Growth, innovation and competition run through our veins, and that’s largely because of the events that unfolded centuries ago at the NYSE and Federal Hall.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.04 percent. The S&P 500 Stock Index rose 1.41 percent, while the Nasdaq Composite climbed 2.59 percent. The Russell 2000 small capitalization index gained 0.92 percent this week.

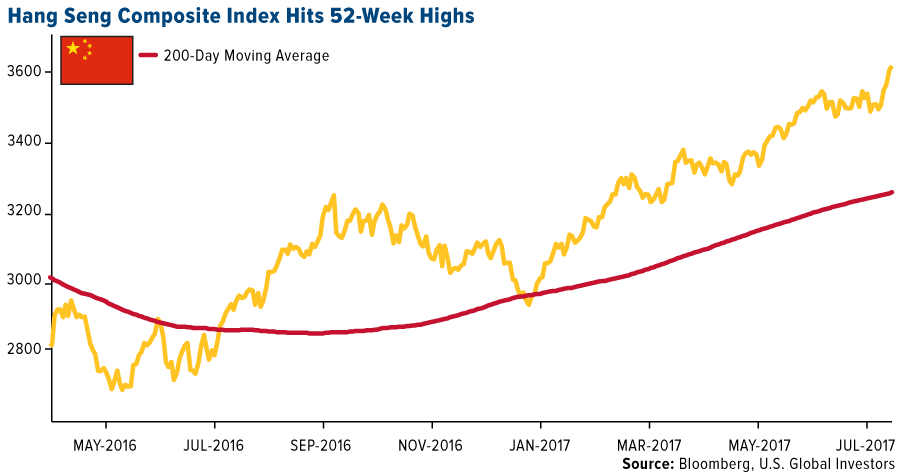

- The Hang Seng Composite gained 3.55 percent this week; while Taiwan was up 1.42 percent and the KOSPI rose 1.46 percent.

- The 10-year Treasury bond yield fell 5 basis points to 2.32 percent.

Domestic Equity Market

Strengths

- Information technology was the best performing sector for the week, increasing by 3.76 percent versus an overall increase of 1.41 percent for the S&P 500.

- NRG Energy was the best performing stock for the week rising 43.1 percent.

- NRG Energy plans to shed 50-100 percent of its renewable assets in a reversal of its diversification strategy. NRG expects to complete the divestment and realize $590 million in savings in SG&A (selling, general and administrative fees) and operating expenses by the end of 2018.

Weaknesses

- Telecommunications was the worst performing sector for the week, declining 1.02 percent versus an overall increase of 1.41 percent for the S&P 500.

- Michael Kors was the worst performing stock for the week declining 5.5 percent.

- The weakness in Michael Kors stems from the fact that there is a bidding war brewing for Jimmy Choo between Michael Kors, Hony Capital Management and CVC Capital Partners. Apparently Jab holding, which owns 70 percent of Jimmy Choo wants to exit the fashion industry and focus on food and coffee.

Opportunities

- For the first time in a few years the U.S. airlines are bringing in more revenue per mile they fly for each passenger. Programs like “basic economy,” premium ticket classes and customized services are extracting more revenue.

- The June NY Fed survey reports that inflation expectations fell slightly for the coming year, but there was an uptick for the three-year outlook. If we continue to see inflation tick down, some market participants will assume the Fed will raise rates slower than previously anticipated.

- Bearish on oil? The brokerage firm Goldman Sachs thinks oil prices can fall below $40 per barrel if there are no sustained declines in U.S. inventories and rig counts remain at current levels. Adding to further oversupply, and reinforcing bearish views, Nigeria and Libya have increased output while Russia continues to reduce their compliance with OPEC’s production reduction agreement.

Threats

- Federal Reserve CEO John Williams reiterated his tightening outlook for the second half of the year. He implied investors could see one more rate hike, along with the beginning of a balance sheet shrinkage program.

- Job openings missed expectations. Employers reported approximately 5.6 million openings versus expectations for nearly 6 million. The decline could indicate signs that business is slowing. On the positive side, total people quitting their jobs is up 2.2 percent. This is good for wage growth and proves the labor market is still tightening.

- Small Business Optimism is losing steam, coming in weaker than expected. Economists were forecasting a level of 104.4 and the NFIB reported 103.6; one of the largest declines since February 2016.

The Economy and Bond Market

Strengths

- The European Union’s official statistics agency said Industrial output was up 1.3 percent from April, and 4 percent from May 2016. The annual rate of increase was the fastest since August 2011, a fresh indication that the area’s economic recovery picked up in the second quarter.

- U.S. industrial production increased 0.4 in June versus estimates of a 0.3 percent gain. The nation’s industrial production has strengthened for five straight months amid robust domestic demand and stronger growth abroad. That’s the longest stretch of improvement since 2014.

- The IMF raised its growth forecast for Germany to 1.8 percent in 2017 and 1.6 percent in 2018, up from 1.6 percent and 1.5 percent, respectively.

Weaknesses

- Growth in China’s broad money supply slowed to a record low in June, signaling policy makers are following through on pledges to cut excessive borrowing. The deceleration in broad M2 money supply, following the slowest pickup on record last month, underlines the challenge for policy makers to keep the world’s second-biggest economy on track to meet growth targets. This could compel them to dial back efforts to contain leverage.

- U.S. retail sales unexpectedly dropped for a second month in June by 0.2 percent (forecast was for a 0.1 percent gain) after falling 0.1 percent the prior month (previously reported as a 0.3 percent drop). The figures suggest households remain cautious about spending and may provide less of a boost for the second-quarter economy after a weak start to the year.

- An overall measure of comfort dropped to 47 from 48.5 the prior week. A sudden downturn in American households’ optimism about the economy and less-favorable views of personal finances sent the Bloomberg Consumer Comfort Index reeling to its lowest point since January, a potentially adverse sign for spending, figures showed Thursday.

Opportunities

- The divergence between soft wage growth and low unemployment in the U.S. is likely to be resolved as the labor market continues to tighten, Goldman Sachs analysts Daan Struyven and Avisha Thakkar write in a July 12 note. Goldman models indicate that the economy is now at full employment. As labor market continues to tighten, wage growth is likely to accelerate, based on aggregate wage survey data.

- Although the baseline forecast sees inflation returning to the 2 percent target, Yellen noted that there was uncertainty as to when this will happen. Consequently, the Fed "intends to carefully monitor actual and expected progress toward our symmetric inflation goal." According to Yellen, "the federal funds rate would not have to rise all that much further to get to a neutral policy stance." The Fed is in wait-and-see mode when it comes to interest rates. The next rate hike should come at the December FOMC meeting if inflation rebounds in the second half of the year, as per BCA forecasts. Little change in the U.S. CPI in June signals inflation may take even longer to reach the Federal Reserve’s goal, a Labor Department report showed Friday. Weak CPI data and dovish Yellen pushed rate-hike odds below 50 percent. The producer price index increased a seasonally adjusted 0.1 percent in June from a month earlier, the Labor Department said Thursday. The month-over-month increase was slightly higher than economists expected, but overall, price pressures continue to remain soft in June.

- Beginning construction of homes in the U.S. jumped in June, indicating building is getting back on track after three months of declines, and economists predict the government to report.

Threats

- Canada joined the U.S. in raising interest rates on Wednesday, fueling speculation the world’s central bankers are heading into a tightening cycle. The central bank’s benchmark rate was raised to 0.75 percent, from 0.5 percent. It said future rate moves will be “guided” by the data, while downplaying recent sluggishness in inflation. Investors are looking at the decision as a possible harbinger of things to come globally, and are monitoring it for clues on the central bank’s resolve for withdrawing stimulus; with the prospect of central bank tightening triggering a selloff in government bond markets over the last two weeks.

- The IMF said central and Eastern Europe’s economic growth potential has halved in the past decade, and the rapid outflow of skilled workers is an increasing drag. This is leading some governments to question the benefits of European integration. The shortage of workers is inhibiting investment. It noted the increased political tension between the EU and the Eastern European member states, with the EU at loggerheads with Poland about rule of law issues and clashing with Hungary over refugees. Eastern European productivity has grown just 2.95 percent since 2010, just 48 basis points per annum, growing just 6 basis points in 2017. Perhaps confirming the IMF’s fears, Russian net capital outflows increased 71 percent year-over-year in the first six months of 2017 to $14.7 billion.

- Fed Chair Janet Yellen said President Trump’s 3 percent growth target would be “quite challenging.” Yellen said it would require a broad set of changes from tax reform to an improved education system. U.S. productivity has been flat since 2012, falling last year, while the growth of the population of working age has fallen 68 percent since 2000 and is forecast to fall a further 47 percent between 2015 and 2020 and then another 59 percent to 2025. With a rising dependency ratio also reducing the amount of capital, it is hard to see any growth.

Gold Market

This week spot gold closed at $1,228.6, up $15.51 per ounce, or 1.28 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.44 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index rose just 0.31 percent. The U.S. Trade-Weighted Dollar Index finished the week lower by 0.93 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jul-13 | Germany CPI YoY | 1.6% | 1.6% | 1.6% |

| Jul-13 | PPI Final Demand YoY | 1.9% | 2.0% | 2.4% |

| Jul-13 | Initial Jobless Claims | 245k | 247k | 250 |

| Jul-14 | CPI YoY | 1.7% | 1.6% | 1.9% |

| Jul-16 | China Retail Sales YoY | 10.6% | -- | 10.7% |

| Jul-17 | Eurozone CPI Core YoY | 1.1% | -- | 1.1% |

| Jul-18 | Germany ZEW Survey Current Situation | 88.0 | -- | 88.0 |

| Jul-18 | Germany ZEW Survey Expectation | 17.5 | -- | 18.6 |

| Jul-19 | Housing Starts | 1155k | -- | 1092k |

| Jul-20 | ECB Main Refinancing Rate | 0.000% | -- | 0.000% |

| Jul-20 | Initial Jobless Claims | 245k | -- | 247k |

Strengths

- The best performing precious metal for the week was silver, climbing up 2.35 percent with the changing sentiment toward precious metals. Gold notched its first weekly gain in a number of weeks on weaker-than-expected inflation and retail sales data. Federal Reserve Chair Janet Yellen took a decidedly dovish stance this week, signaling the Fed was in no hurry to tighten monetary policy with monthly consumer prices growth falling short of the Fed’s target 2 percent. The gold market responded positively, with gold futures jumping sharply above $1,220 after her testimony.

- June imports of gold in India more-than-doubled compared to the same month last year, Bloomberg reports, as consumers rushed to act before the country’s new tax law went into effect. Demand rose to 72 metric tons in June, up from 31.8 tons a year earlier. The downside here is that we may see a slowdown in consumption now that jewelers have already built up their stocks for the upcoming Diwali festival and wedding season. In the long-term, however, India—the world’s second-biggest consumer after China—is expected to see a huge boost in demand. The World Gold Council (WGC) estimates imports could rise to between 850 and 950 tons by 2020, up from between 650 and 750 today.

- Peter Grosskopf, CEO of Sprott, is bullish on gold, saying that the firm has “a good constructive long-term view that it is an asset that should be accumulated.” He added that gold “is vastly under-invested by most investors.” Now with gold prices having lost value recently on fears that the Federal Reserve will hike rates, Grosskopf sees this as a buying opportunity.

Weaknesses

- The worst performing precious metal for the week was gold, still up 1.26 percent. Bullion sales at Japan’s biggest retailer, Tanaka Kikinzoku Kogyo, fell a staggering 41 percent in the first half of 2017 compared to the same period last year, according to Bloomberg. Platinum bar sales disappointed as well, falling 53 percent. Tanaka reported that investors “refrained from aggressive trading” due to tighter U.S. monetary policy. Demand weakness also hit Japan’s southern neighbor Australia. The Perth Mint, the world’s number two gold refiner, recently saw sales of coins and bars fall to a five-year low. “With equities at near-record levels and greater economic confidence in the U.S. and throughout the world, there has been less interest in safe haven products,” remarked Neil Vance, the Perth Mint’s group manager of minted products.

- Hedge fund managers’ net-long positions on gold were trimmed in half last week compared to the previous week, the largest such reduction in two years. It was the fourth straight week of declines. Bullish bets on gold stood at 37,776 contracts for the week ended July 3, significantly down from 174,658 as recently as June 6, according to the Commodity Futures Trading Commission.

- Indian gold retailers were offering a discount on jewelry for the first time in over a month this week, a sign that demand is slipping. As discussed above, June was especially busy, as consumers loaded up on gold to avoid paying the 3 percent gold tax rate under the new Goods and Services Tax that went into effect July 1.

Opportunities

- Novo Resources signed a memorandum of understanding (MoU) with Sumitomo Corporation to further develop the Company’s Beatons Creek project, according to a July 7 news release. Sumitomo will provide assistance with preparation of Novo’s internal study, including basic engineering design work and other studies. Novo is also earning in to Artemis Resources Purdy Reward prospect as part of an overall $2 million farm-in and 50/50 joint venture on Artemis; conglomerate gold targets on its Karratha tenement package. Initial exploration activity at Purdy’s Reward involved a trenching program, with the first trial trench identifying in situ gold nuggets up to 4cm long in Archean conglomerates. Most recently, Novo put out a press release on July 12, sending the stock soaring 55.2 percent. The release was the first that the TSX has allowed a YouTube video to be attached to – the first video shows someone using a metal detector to find the signal of a nugget in the test pit, while the second video shows someone using an air chisel to pry out a rock containing several gold nuggets, writes Bob Moriarty for Streetwise Reports. Novo’s share price surged 58 percent upon the discovery of the gold nuggets.

- Nano One Materials announced it was issued a patent expanding its propriety position to include the improvements in battery performance. According to the press release, the addition of this patent builds on an already strong portfolio of intellectual property Nano One has assembled. The stock climbed nearly 40 percent post the news release. In late June, CEO of Nano One Dan Blondal announced that “commissioning of the pilot plant is complete and scaled-up production of lithium ion cathode materials that meet Nano One’s processing and battery capacity targets has been demonstrated,” according to a June 26 news release by the company. Blondal added that Nano One is now well positioned to execute its 2017 plans in bringing industrial interests to the table.

- Golden Predator Mining announced this week assay results for 23 reverse circulation drill holes completed at the 3 Aces Project. The company intersects 6.86 m of 20.15 grams per ton gold at the 3 Aces Project. In the July 10 press release, Golden Predator notes that “in addition to the already identified high-grade underground targets, the drilling results suggest a merging into a single gently dipping zone, providing a potential near surface bulk mineable.”

Threats

- South Africa’s Chamber of Mines released a statement noting that the Department of Minerals has agreed to suspend implementation of the new Mining Charter, reports JP Morgan’s Dominic O’Kane. This, pending the outcome of the interdict application brought by the Chamber of Mines. JP Morgan interprets this to be a minor positive for South African mining shares, since at the very least it delays implementation of Charter requirements. “We retain our view that SA exposed companies with ability to pursue corporate re-organizations are best positioned to mitigate SA sovereign risk, these include Anglo American and Gold Fields and Anglo Gold,” the research note reads.

- According to JP Morgan’s Chairman Jamie Dimon, the unwinding of quantitative easing might be more disruptive than you think, reports Bloomberg. Central banks are preparing to reverse massive asset purchases made after the financial crisis – the Fed, ECB and Bank of Japan bulked up their balance sheets to nearly $14 trillion, the article continues. An unwinding of this amount could influence a slew of markets. Dimon notes that all the main buyers of sovereign debt over the last 10 years will now be net sellers.

- Tanzanian President John Magufuli has signed into law new mining bills requiring the government to own at least 16 percent state in mining projects, reports The Daily Mail. On Monday, Magufuli said that no new mining licenses would be issued until Tanzania “put things in order.” The new laws raise royalties tax for gold, copper, silver and platinum exports and also give the government the right to tear up and renegotiate contracts for natural resources, the article continues.

Energy and Natural Resources Market

Strengths

- China economic data reported this week came in stronger than expected. Both exports and imports showed marked month-on-month improvements. Exports rose by 11.3 percent from a year earlier handsomely beating the economists’ forecast of a 9 percent rise. Similarly, imports rose 17.2 percent from a year earlier, significantly more than the 12.4 percent forecast by market participants. These two measures support a recent improvement in Chinese macro data that should be supportive for commodity prices.

- Crude prices rallied this week after data showed the largest crude inventory draw since at least September last year. Department of Energy data showed a weekly 7.6 million barrel crude draw which helped spark a rally in the commodity.

- Iron ore imports by China are set to break 2016 records this year. Year-to-date, Chinese buyers have imported 539 million tons of iron ore, a 9.3 percent rise over the same period last year. As a result, China is comfortably on pace to import more than 1 billion tons of ore this year.

Weaknesses

- Goldman Sachs believes crude prices may drop below $40 per barrel if OPEC fails to “shock and awe” the market. The bank’s commodity analysts suggest that OPEC must increase output cuts to lift investor sentiment and prevent prices from dropping below the $40 per barrel level. Caution is necessary now that speculative positioning is no longer stretched on the short side, meaning that the short sellers are currently on the sidelines and could begin to short sell crude should the OPEC narrative lose momentum.

- Canadian oil sands are joining U.S. shale in displacing OPEC as the global swing producer of crude oil. Major oil sands producers are running as much as 30 percent above capacity in 2017, adding supply to the global crude market at the same time OPEC attempts to limit its combined output. As a result, Canada is likely to become the second largest contributor to crude production growth over the next two years, thereby threatening the recovery in crude prices according to IHS Energy.

- The unrelenting rally in zinc prices stalled this week on bearish signals from stockpiles. Available inventories at the London Metals Exchange surged 41 percent on Friday, the most on record, after inventories earmarked for delivery were returned to warehouses.

Opportunities

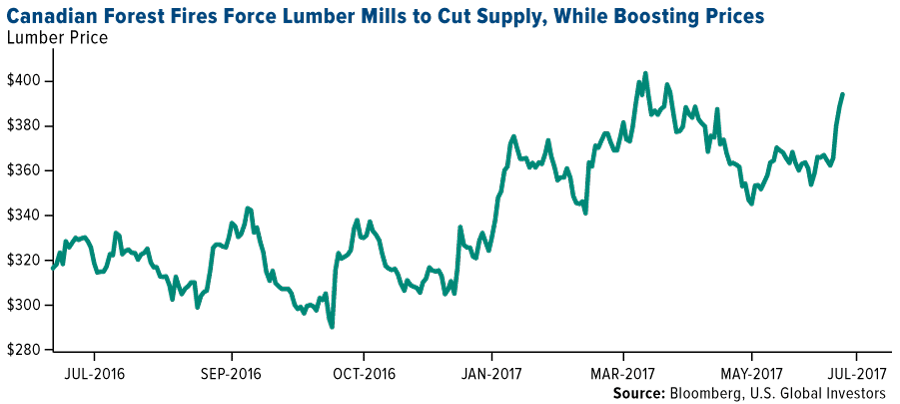

- Lumber prices rallied this week as more than 200 wildfires disrupted forestry operations in the province of British Columbia. Operations at Norbord and West Fraser Timber near Williams Lake, BC have been affected, suggesting that as much as 7 percent of BC’s annual output may see considerable downtime.

- China’s crude imports continue to increase with significant momentum. In June, the far east nation imported 8.79 million barrels of crude per day (mbpd), making it the largest crude importing nation for the second month in a row. Further to that, data shows Chinese crude imports year-to-date are tracking at 8.55 mbpd, a 13.8 percent increase over the same period last year.

- Saudi Arabia has announced it will lower its exports volumes for the remainder of the summer to satisfy peak domestic demand in the summer months. Although the Kingdom will not further curtail production, the removal of 600,000 barrels per day from the global seaborne market may cause near-term support for crude prices.

Threats

- OPEC producers are growing crude production despite agreement, warns the International Energy Agency (IEA). Global oil supply rose 720,000 barrels per day in June as Nigeria, Lybia and Saudi Arabia raised output. As a result, compliance with the production agreement has dropped to only 78 percent, after posting 90-plus percentage compliance in previous months.

- U.S. crude exports may quadruple by 2020 and outpace the export volumes of numerous OPEC producers, warns PIRA Energy, an influential energy consultant. The report suggests U.S. exports may reach 2.25 mbpd, a move that could drive the global oil market into a greater imbalance.

- Further copper production disruptions appear likely after workers at two of Antofagasta’s mines, Zaldivar and Centinela, voted in favor of striking. Despite the overall positive copper price reaction to the events, there has been a marked increase in strikes at base metals mines over the past nine months, leading to sizeable downtime and financial impact to the operators.

China Region

Strengths

- The Hang Seng Composite Index (HSCI) soared 3.55 percent to new 52-week highs amid one of Asia’s best weeks in months.

- The South Korean won had a particularly strong week, gaining about 1.86 percent since last week.

- Information technology was the strongest sector in the HSCI, climbing 5.04 percent for the week.

Weaknesses

- Malaysia’s FTSE Bursa Malaysia KLCI Index fell 27 basis points for the week.

- Standard & Poor’s cut the Philippines’ 2017 GDP growth forecast from March’s 6.6 percent down to a 6.4 percent.

- Materials was the worst-performing sector in the HSCI , falling 3.87 percent for the week.

Opportunities

- China’s iron ore stockpiles are at record highs, reports Bloomberg, with shipments on course to exceed last year’s record. The Asian economy has been pulling in greater volumes of the low-cost ore to meet resilient demand from mills, who have benefited from rising steel prices in the second quarter. The increase is aiding miners like BHP Billiton and Rio Tinto.

- Apple will establish its first data center in China, entirely driven by renewable energy, to speed up services and abide by laws that require global companies to store information within the country, reports Bloomberg. “The addition of this data center will allow us to improve the speed and reliability of our products and services while also complying with newly passed regulations,” the company said in its statement. “Apple has strong data privacy and security protections in place and no backdoors will be created into any of our systems.”

- Senior Chinese and U.S. government officials will meet in Washington next week, reports China Daily, to discuss economic and trade issues of mutual concern. President Xi Jinping and U.S. President Donald Trump met on the sidelines of the G20 Summit in Germany recently, agreeing to hold the economic dialogue on July 19, the article continues.

Threats

- Amid Chinese President Xi’s goal of “cyber-sovereignty,” the Chinese government has told telecommunication carriers to block individuals’ access to virtual private networks (VPNs) by February 1, reports Bloomberg. “China has one of the world’s most restrictive internet regimes, tightly policed by a coterie of government regulators intent on suppressing dissent to preserve social stability,” the article reads.

- China’s outbound investment tumbled in the first half of the year—from a record 2016 and thus very difficult comps—amid governmental curbs on foreign acquisitions. Outward direct investment fell to just over $48 billion in the first half of 2017.

- The U.S. is reportedly considering increased or additional sanctions against Chinese banks to place more pressure on China with respect to the North Korean threat.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 5 percent. Turkish equites are supported by positive momentum in global sentiment. Tomorrow, major public gatherings around the country will take place to remember victims of last year’s coup.

- The Turkish lira was the best performing currency this week, gaining 2.3 percent against the U.S. dollar. Emerging currencies surged after Janet Yellen delivered a speech which was regarded as dovish. According to Bloomberg, the probability of rate hikes this year declined to 43 percent from 55 percent last week.

- Real estate was the best performing sector among eastern European markets this week.

Weaknesses

- The Czech Republic was the worst relative performing country this week, gaining 70 basis points. Czech headline inflation eased to 2.3 percent year-over-year last month, from 2.4 percent year-over-year in May. The fall was driven almost entirely by weaker fuel inflation.

- The euro was the worst relative performing currency this week, gaining 60 basis points against the U.S. dollar. According to Reuters, the European Central Bank wants to keep its asset-purchases open-ended rather than setting a potentially distant date on which bond- buying will stop. This is to retain flexibility in case the outlook sours.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

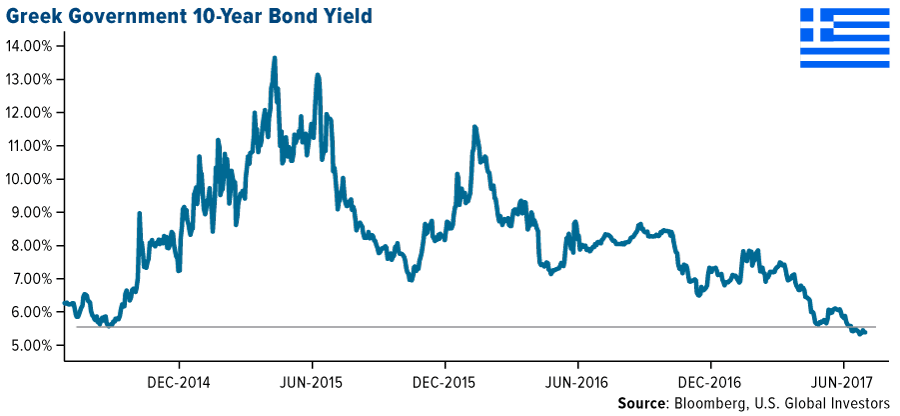

- With 10-year government yields coming down to the level last seen in the year 2014, the Greek government could be preparing for a sovereign bond issue later this month. If the bond issuance is successful, it will improve investors’ confidence in Greece’s ability to repay its debt and will be an important step toward ending the country’s dependence on official funding next year.

- Poland’s year-to-date budget balance seems to be much better than expected, mostly due to an increase in revenue from tax income and stronger earnings coming from National Bank of Poland. If the trends continue until the end of the year, Poland could end up with a much smaller deficit of around 1.5 percent of gross domestic product versus 2.9 percent last year.

- Eurozone industrial output was up 1.3 percent from April, and 4 percent from May 2016, rising at the fastest rate in nearly six years, supported by a large increase in the production of capital goods. That performance was stronger than expected, suggesting economic recovery picked up in the second quarter.

Threats

- Economic growth in the euro-area is strengthening, but inflation is still well below the ECB’s target of 2 percent. Headline inflation in the euro-area slowed further in June, rising by 1.3 percent on a year-over-year basis, according to a preliminary release. Final June inflation will be released next week.

- President Donald Trump’s eldest son may become a subject of investigation into Russia meddling in the 2016 campaign. Donald Trump Jr. met with a Russian woman who offered potentially damaging information on Hillary Clinton last year after his father had secured the Republican presidential nomination. News of this meeting began emerging last Saturday, a day after the U.S. president met face-to-face for the first time with Putin.

- In Poland, legislation was approved that gave parliament the rights to name judges to the judiciary council, which determines appointments to the nation’s 400 courts, shortens the panel’s term and gives the government control over appointing heads of courts. Poland and Hungary are the two nations that are under scrutiny for allegedly breaching the EU democratic norms. Germany is thinking about linking future EU funds to whether members uphold to the rule of law. Poland and Hungary are the biggest net recipients of EU funds.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| Russell 2000 | 1,428.82 | +12.98 | +0.92% |

| S&P Basic Materials | 346.31 | +6.90 | +2.03% |

| Nasdaq | 6,312.47 | +159.39 | +2.59% |

| Hang Seng Composite Index | 3,621.51 | +124.22 | +3.55% |

| S&P 500 | 2,459.27 | +34.09 | +1.41% |

| Gold Futures | 1,228.10 | +18.40 | +1.52% |

| Korean KOSPI Index | 2,414.63 | +34.76 | +1.46% |

| DJIA | 21,637.74 | +223.40 | +1.04% |

| S&P/TSX Global Gold Index | 188.25 | +2.47 | +1.33% |

| SS&P/TSX Venture Index | 757.55 | +2.33 | +0.31% |

| XAU | 80.80 | +3.30 | +4.26% |

| S&P Energy | 481.78 | +9.83 | +2.08% |

| Oil Futures | 46.62 | +2.39 | +5.40% |

| 10-Yr Treasury Bond | 2.33 | -0.06 | -2.39% |

| Natural Gas Futures | 2.98 | +0.12 | +4.02% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,414.63 | +41.99 | +1.77% |

| Hang Seng Composite Index | 3,621.51 | +101.90 | +2.90% |

| Nasdaq | 6,312.47 | +117.57 | +1.90% |

| XAU | 80.80 | -0.37 | -0.46% |

| S&P/TSX Global Gold Index | 188.25 | -11.94 | -5.96% |

| Gold Futures | 1,228.10 | -47.80 | -3.75% |

| S&P 500 | 2,459.27 | +21.35 | +0.88% |

| S&P Basic Materials | 346.31 | +5.38 | +1.58% |

| DJIA | 21,637.74 | +263.18 | +1.23% |

| Russell 2000 | 1,428.82 | +11.24 | +0.79% |

| SS&P/TSX Venture Index | 757.55 | -21.75 | -2.79% |

| Oil Futures | 46.62 | +1.89 | +4.23% |

| S&P Energy | 481.78 | -2.21 | -0.46% |

| Natural Gas Futures | 2.98 | +0.05 | +1.57% |

| 10-Yr Treasury Bond | 2.33 | +0.20 | +9.55% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,414.63 | +279.75 | +13.10% |

| Hang Seng Composite Index | 3,621.51 | +281.88 | +8.44% |

| Nasdaq | 6,312.47 | +507.32 | +8.74% |

| Natural Gas Futures | 2.98 | -0.25 | -7.69% |

| Gold Futures | 1,228.10 | -63.60 | -4.92% |

| S&P 500 | 2,459.27 | +130.32 | +5.60% |

| S&P Basic Materials | 346.31 | +24.54 | +7.63% |

| S&P/TSX Global Gold Index | 188.25 | -32.83 | -14.85% |

| XAU | 80.80 | -8.60 | -9.62% |

| DJIA | 21,637.74 | +1,184.49 | +5.79% |

| Russell 2000 | 1,428.82 | +83.57 | +6.21% |

| SS&P/TSX Venture Index | 757.55 | -77.07 | -9.23% |

| S&P Energy | 481.78 | -27.62 | -5.42% |

| Oil Futures | 46.62 | -6.56 | -12.34% |

| 10-Yr Treasury Bond | 2.33 | +0.09 | +4.07% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,379.87 | +19.73 | +0.84% |

| Hang Seng Composite Index | 3,497.29 | -36.11 | -1.02% |

| Nasdaq | 6,153.08 | -144.30 | -2.29% |

| XAU | 77.50 | -9.09 | -10.50% |

| S&P/TSX Global Gold Index | 185.73 | -31.98 | -14.69% |

| Gold Futures | 1,211.80 | -81.40 | -6.29% |

| S&P 500 | 2,425.18 | -7.96 | -0.33% |

| S&P Basic Materials | 339.41 | +3.10 | +0.92% |

| DJIA | 21,414.34 | +240.65 | +1.14% |

| Russell 2000 | 1,415.84 | +19.16 | +1.37% |

| SS&P/TSX Venture Index | 755.22 | -37.66 | -4.75% |

| Oil Futures | 44.35 | -1.37 | -3.00% |

| S&P Energy | 471.95 | -4.10 | -0.86% |

| Natural Gas Futures | 2.86 | -0.16 | -5.43% |

| 10-Yr Treasury Bond | 2.39 | +0.21 | +9.71% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,379.87 | +228.14 | +10.60% |

| Hang Seng Composite Index | 3,497.29 | +153.96 | +4.60% |

| Nasdaq | 6,153.08 | +275.27 | +4.68% |

| Natural Gas Futures | 2.86 | -0.41 | -12.42% |

| Gold Futures | 1,211.80 | -48.80 | -3.87% |

| S&P 500 | 2,425.18 | +69.64 | +2.96% |

| S&P Basic Materials | 339.41 | +9.67 | +2.93% |

| S&P/TSX Global Gold Index | 185.73 | -28.80 | -13.42% |

| XAU | 77.50 | -8.62 | -10.01% |

| DJIA | 21,414.34 | +758.24 | +3.67% |

| Russell 2000 | 1,415.84 | +51.27 | +3.76% |

| SS&P/TSX Venture Index | 755.22 | -69.05 | -8.38% |

| S&P Energy | 471.95 | -45.18 | -8.74% |

| Oil Futures | 44.35 | -7.89 | -15.10% |

| 10-Yr Treasury Bond | 2.39 | +0.00 | +0.08% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investHoldings may change daily.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of 03/31/2017:

BHP Billiton

Gold Fields Ltd

Novo Resources Corp

Nano One Materials Corp

Golden Predator Mining Corp