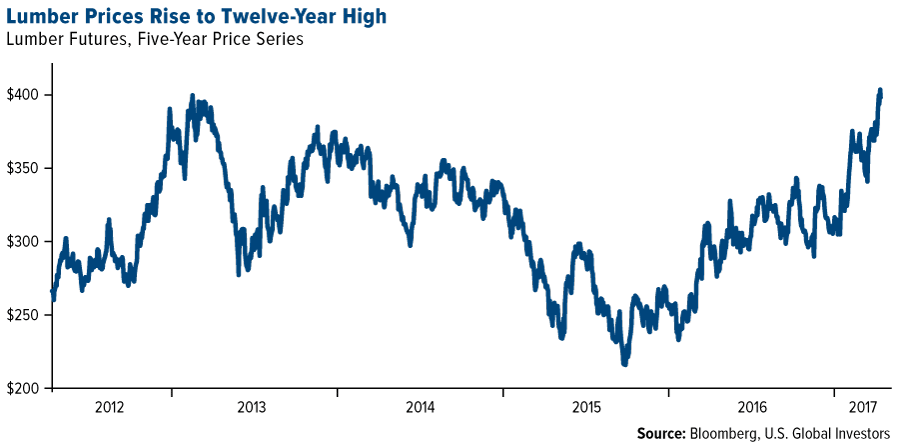

As if you need more proof that inflation is finally starting to pick up, lumber prices rose to a 12-year high this week, supported mainly by expectations that steep duties will soon be levied on cheap softwood imports from Canada. Lumber futures rose to nearly $415 per thousand board feet on Monday, a level unseen since March 2005, soon after homeownership peaked here in the U.S.

At issue is a mini-trade war between U.S. and Canadian loggers. For some time now, the American lumber industry has blamed its Canadian counterpart of unfairly dumping lumber in the U.S. that’s far below market value. Now, several factors are pushing timber prices higher. Chief among them are the likelihood of duties being raised at the Canadian border, possibly as early as next month; President Donald Trump’s calls to renegotiate NAFTA; and growing demand for new homes following the housing crisis as consumer optimism improves and millennial buyers finally seem eager to enter the market.

Shares of Canfor Corporation and Western Forest Products, Canada’s number two and number five lumber producers by annual output, have had a good three months, advancing 25.5 percent and 16.8 percent respectively as of April 12. Timberland-owner Weyerhaeuser has also impressed lately.

Gold Glimmers Brightly

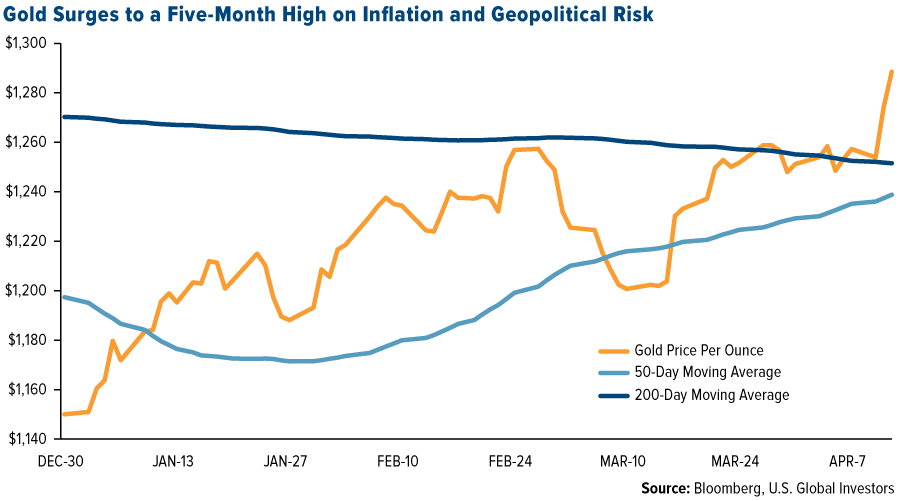

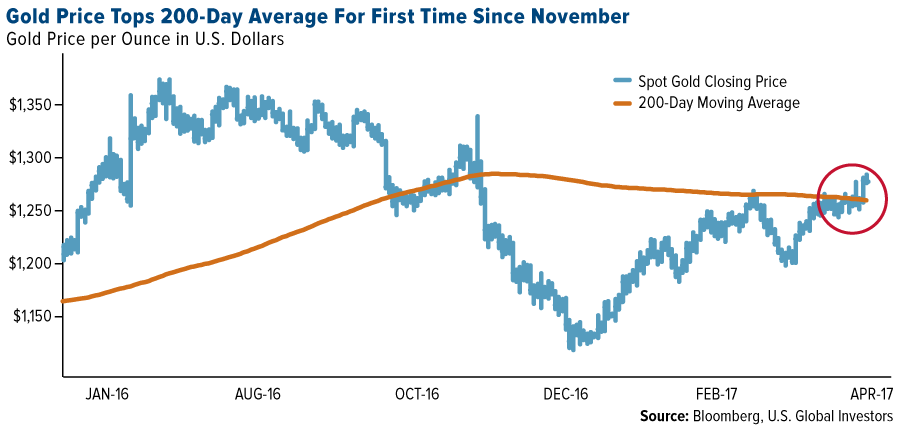

As I told Daniela Cambone during this week’s edition of Gold Game Film, this is all very constructive for the price of gold, which has historically been used as a hedge during periods of rising inflation. The yellow metal closed above $1,270 an ounce this week for the first time since soon after the November presidential election. A “golden cross” has not yet occurred, with the 50-day moving average still below the 200-day, but such a move appears likely in the next few trading sessions if upward momentum can be sustained.

Fueled also by geopolitical tensions associated with Syria, Russia and North Korea, gold demand is on the rise, with Tuesday’s trading volumes on gold calls surging 10 times Monday’s amount on the New York Mercantile Exchange. As I already shared with you, investor sentiment of gold during last week’s European Gold Forum was particularly strong. A poll taken during the conference showed that 85 percent of attendees were bullish on the metal, with a forecast of $1,495 by year’s end.

With the U.S. ramping up military action overseas, including its dropping of a devastating bomb in Afghanistan today, many investors are lightening their risk assets in favor of “safe haven” instruments such as gold and Treasuries. The S&P 500 Index dropped below its 50-day moving average this week, signaling a slowdown in blue chip stocks. This is yet another example of the wisdom of crowds.

Financials were among the biggest laggards as investors have begun to question President Trump’s ability to deregulate the banking sector. After several disappointments and setbacks, including a failure to repeal and replace Obamacare, renewed military involvement in Syria and Afghanistan might provide a welcome boost to Trump’s sluggish job approval rating.

Gold also responded positively to recent comments by Trump on U.S. dollar strength and monetary policy. Specifically, he said the dollar is “getting too strong” and later supported a low interest rate policy, suggesting he might keep Janet Yellen as the Federal Reserve chair.

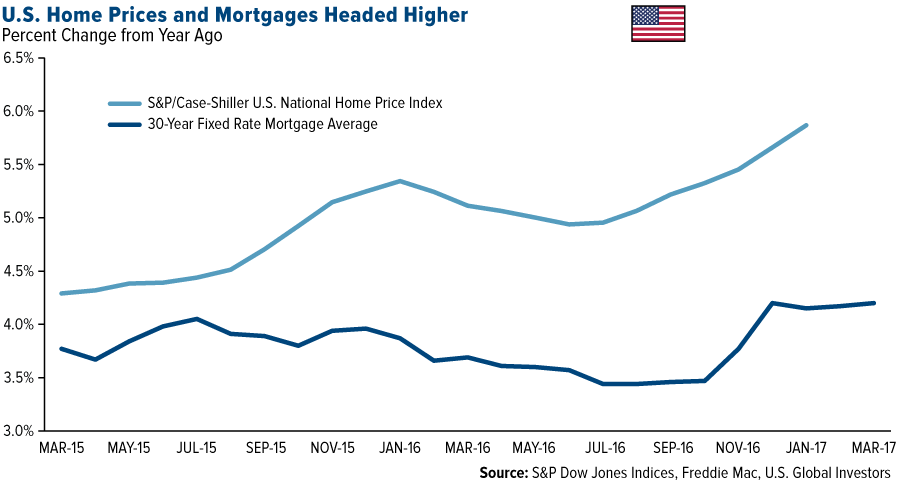

Millennial Homebuyers Finally Entering the Housing Market

April is New Homes Month, and to celebrate, the National Association of Home Builders (NAHB) shared some of the significant contributions housing provides to the U.S. economy. According to the Washington, D.C.-based group, “building 100 single-family homes in a typical metro area creates 297 full-time jobs and generates $28 million in wage and business income and $11.1 million in federal, state and local tax revenue.” The sector currently accounts for 15.6 percent of U.S. gross national product (GNP).

Indeed, housing has a phenomenal multiplier effect on the economy, as I’ve pointed out before, and I’m pleased to see its recovery after nearly a decade.

Not only is consumer confidence up, but homebuilder confidence, as measured by the NAHB, hit a 12-year high in March, supported by an improving economy and President Trump’s pledge to roll back strict regulations. In February, new housing starts hit 1.29 million units, beating market expectations of 1.26 million units.

Rising mortgage rates and home prices are also likely encouraging buyers to enter the market. With the 30-year rate having recently fallen to a fresh 2017 low, we might see an even stronger surge in mortgage applications.

Declines in homeownership among lower-income, nonwhite and young adults were especially dramatic following the housing crisis, as subprime lending, which many homeowners had previously relied on, all but dried up. Homeownership rates in the U.S. steadily fell to a 50-year low, which only lengthened the recovery time of the Great Recession. According to Rosen Consulting, a real estate consulting group, the U.S. economy would have been $300 billion larger in 2016 had the housing market fully returned to its long-term level of construction and homebuying.

Millennials, or those generally born between 1981 and 1998, have been the biggest holdouts, but we’re finally starting to see that change. The cohort—the largest group of homebuyers in the U.S. right now—represented around 45 percent of all new home loans in January of this year. It’s likely we’ll see this figure rise as more millennials become better established in their careers and tire of renting.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.01 percent. The S&P 500 Stock Index fell 1.21 percent, while the Nasdaq Composite fell 1.26 percent. The Russell 2000 small capitalization index lost 1.41 percent this week.

- The Hang Seng Composite lost 0.07 percent this week; while Taiwan was down 0.62 percent and the KOSPI fell 0.19 percent.

- The 10-year Treasury bond yield fell 10 basis points to 2.24 percent.

Domestic Equity Market

Strengths

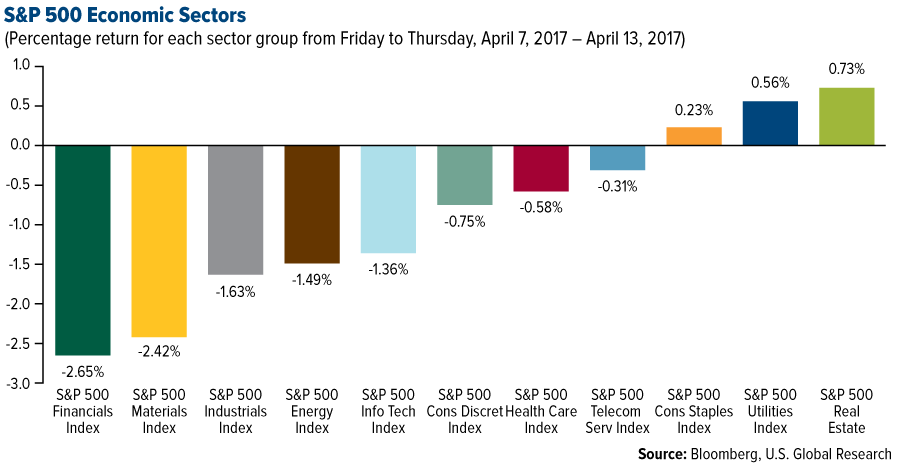

- Real estate was the best-performing sector of the week, increasing 0.73 percent compared to an overall decrease of 1.13 percent for the S&P 500 Index.

- Whole Foods Market was the best-performing stock for the week, increasing 9.30 percent.

- JPMorgan Chase reported first-quarter earnings and revenue that easily topped estimates, lifted by better-than-expected loan growth and trading sales.

Weaknesses

- Financials was the worst-performing sector for the week, falling 2.65 percent compared to an overall decrease of 1.13 percent for the S&P 500 Index.

- Fastenal was the worst-performing stock for the week, falling 9.34 percent.

- Snap slid below $20 after Instragram’s Snapchat clone said it has more users. The Facebook-owned Instagram announced on Thursday that Stories has more than 200 million daily users, ahead of the 161 million reported by Snapchat.

Opportunities

- BCA’s U.S. equity strategists are upgrading machinery stocks. The firm’s Global Capital Spending Indicator has climbed back into positive territory. That primarily reflects the firming in global purchasing manager’s indexes. When global output growth recovers, machinery demand tends to demonstrate its high beta characteristics. BCA’s global ex-U.S. machinery new orders proxy has jumped sharply in recent months, consistent with the global machinery exports proxy. While the previously strong U.S. dollar threatened to divert this demand to non-U.S. competitors, the playing field has leveled: U.S. machinery new orders have also accelerated.

- Despite rising interest rates, there is positive momentum for U.S. earnings per share growth this year due to improving pricing power and stronger global growth.

- The outlook for business sales has brightened with corporate pricing power recovering and the global economy improving. This is critical to absorbing the increase in labor costs and cushioning the profit margin squeeze. If the U.S. dollar were to weaken, especially if it occurs within the context of better economic growth abroad, then the revenue upside would increase.

Threats

- The rally in infrastructure stocks has stalled. Infrastructure stocks soared after Trump’s election win, with the S&P 500 Materials Index gaining nearly 13 percent before topping out at the beginning of March. However, all of these stocks have given up a portion of their post-election gains.

- A former Snapchat employee is accusing the social-media company of falsifying its growth metrics. Anthony Pompliano filed a lawsuit against the company in January, accusing Snapchat of firing him after he raised the issue with senior leadership.

- Trump told manufacturing CEOs during a White House event that he was going to release something “phenomenal in terms of tax” in two or three weeks. As of April 10, eight and a half weeks later, no tax plan has been released by the White House, and, based on reports, it doesn’t appear to be coming soon. The Associated Press’ Josh Boak and Stephen Ohlemacher report that administration officials have scrapped the outline for tax reform Trump released during the campaign and are writing a new plan. According to the report, the White House is writing a version of a tax plan rather than signing onto one from congressional lawmakers, as it did with health care. The American Health Care Act failed to pass the House last month, and the misstep has left analysts concerned about the future of Trump’s agenda. A failure to pass tax reform would likely cause a market selloff.

The Economy and Bond Market

Strengths

- Consumers have not been this bullish about the U.S. economy since 2000. The preliminary results of the University of Michigan’s April survey showed that the overall consumer sentiment index jumped to 98 from 96.9 in March, while the current economic conditions index rose to 115.2, a 17-year high.

- China’s trade data beat expectations. Exports surged by 16.4 percent in U.S. dollar terms as imports grew by 20.3 percent, making for a surplus of $23.93 billion in March. Economists were expecting a $10 billion surplus after February’s $9.15 billion deficit. As the second biggest economy, this is a positive sign of economic strength.

- Germany’s ZEW survey hits its highest level since August 2015. “The German economic situation has proved fairly robust in the first quarter,” ZEW’s president, Professor Achim Wambach, wrote in the release. “This is highlighted by the solid figures for growth in industrial production, the construction sector and retail sales from February.”

Weaknesses

- The U.S. created just 98,000 new jobs in March to mark the smallest gain in almost a year, a sign the labor market is not quite as strong as big hiring gains earlier in 2017 suggested.

- U.S. inflation at the wholesale level fell in March for the first time in seven months. The producer price index slipped 0.1 percent last month to mark the first decline since August, the government said Thursday. Economists surveyed by MarketWatch had predicted no change in the PPI.

- Small-business owner optimism declined in March as sales expectations and earnings came back to earth after a post-election surge. The National Federation of Independent Business said its monthly sentiment gauge fell 0.6 points to 104.7.

Opportunities

- The Leading Index will be released next Thursday. The expectation of continued growth would be a good sign of future economic resilience.

- The preliminary April Markit U.S. Manufacturing PMI will be released next Friday. Consensus is for continued strengthening, keeping the upward momentum in manufacturing strength.

- March housing starts will be released next Tuesday and are expected to continue showing growth in the housing market.

Threats

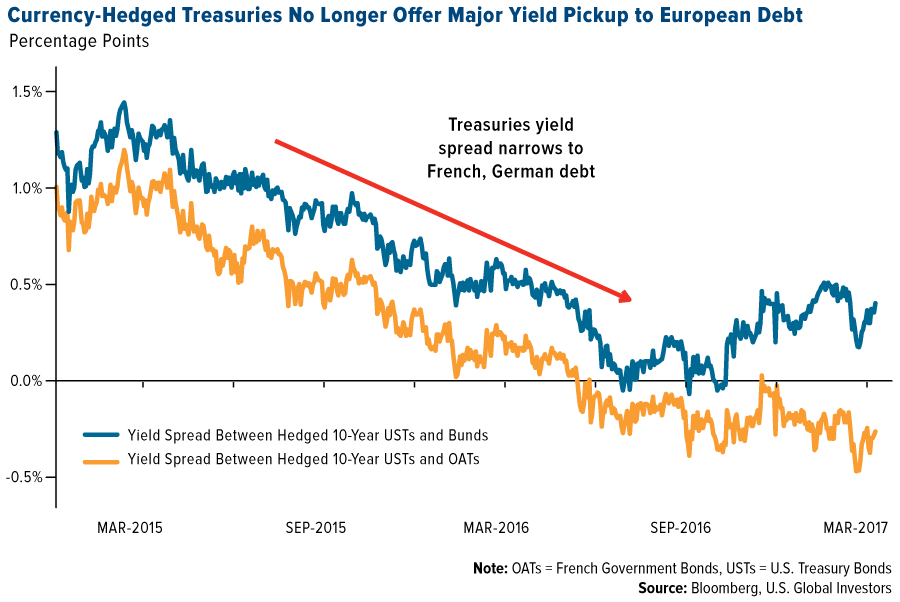

- As of late, many investors in the bond market are obsessed over what will happen when the Federal Reserve starts winding down its mammoth, crisis-era investments in U.S. government bonds. As much of a concern as this is, there is another enormous debt pile that could draw buyers away from Treasuries at just the wrong time. In overseas markets, more than $3 trillion of negative-yielding government bonds — which all but guarantee losses for buy-and-hold investors — have turned positive in recent months. And analysts say that number may grow over the next few years as brighter economic prospects and shifts in monetary policy lift trillions more out of sub-zero levels in Europe and Japan. Currently, after accounting for the cost to hedge against the dollar’s ups and downs — a common practice for those that invest abroad — 10-year Treasuries yield just 0.4 percentage points more than German bunds. The turnabout is even starker for French bonds. They yield almost 0.3 percentage points more than currency-adjusted Treasuries. As recently as two years ago, hedged U.S. notes offered a 1.2 percentage point pickup. For now, the unraveling of the reflation trade has helped to keep Treasury yields in check. But as the Fed lays the groundwork for unwinding its balance sheet, any pullback by foreigners could spell trouble.

- According to BCA, the disappointment for investors will stem not from the failure of the Trump administration and Congressional Republicans to cut taxes, but from the underwhelming effect that tax cuts end up having on the economy. The highly profitable companies that will benefit the most from lower corporate taxes are the ones who least need them. In many cases, these companies have plenty of cash and easy access to external financing. As a consequence, much of the tax cuts will simply be hoarded or used to finance equity buybacks or dividend payments. A large share of personal tax cuts will also be saved, given that they will mostly accrue to higher income earners.

- The weakening state of U.S. corporate balance sheets means credit spreads are at risk once monetary policy turns less accommodative, signaled by a flat yield curve.

Gold Market

This week spot gold closed at $1,287.88, up $33.43 per ounce, or 2.66 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 4.12 percent. Junior-tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index rose 1.26 percent. The U.S. Trade-Weighted Dollar Index finished the week lower by 0.60 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-11 | Zew Survey Current Situation | 77.5 | 80.1 | 77.3 |

| Apr-11 | Zew Survey Expectations | 14.8 | 19.5 | 12.8 |

| Apr-13 | Germany CPI YoY | 1.6% | 1.6% | 1.6% |

| Apr-13 | U.S. PPI Final Demand YoY | 2.4% | 2.3% | 2.2% |

| Apr-13 | U.S. Initial Jobless Claims | 245k | 234k | 235k |

| Apr-14 | U.S. CPI YoY | 2.6% | — | 2.7% |

| Apr-16 | China Retail Sales YoY | 9.7% | — | 10.9% |

| Apr-18 | U.S. Housing Starts | 1260k | — | 1288k |

| Apr-19 | Eurozone CPI Core YoY | 0.7% | — | 0.7% |

| Apr-20 | U.S. Initial Jobless Claims | — | — | 234k |

Strengths

- The best performing precious metal for the holiday-shortened week was silver, up 3.01 percent, followed by gold, up 2.66 percent as geopolitical risks surrounding Syria and North Korea sparked demand for haven assets. Gold settled above its 200-day average for the first time since November, reports Bloomberg.

- Indian gold imports surged nearly seven-fold, or 582 percent, in March from a year earlier, reports Bloomberg. Jewelers stocked up on the yellow metal in anticipation of a demand recovery during the wedding season that began this month, with shipments advancing to 120.8 metric tons since last year, the article continues.

- The U.K. Royal Mint’s gold sales jumped 20 percent during the first quarter of the year, reports Bloomberg, following month-on-month declines in January and February. In volume terms, March sales jumped 263 percent, while gold sold and stored by the mint under its Signature Gold program—which allows partial ownership of bars held in its vault—jumped 178 percent in March.

Weaknesses

- The worst-performing precious metal for the week was palladium, down 0.85 percent. Hedge funds had boosted their net-long position in the futures market to a two-year high in the prior week just as a report came out the following week that U.S. auto sales slumped in March.

- The London Bullion Market Association (LBMA) PM gold price was set nearly $15 below spot on Tuesday, reports Kitco News, once again putting the market’s transparency in the spotlight. Jeff Christian, managing director at CPM Group, says he sees this as the effect of poorly conceived regulations and a faulty price discovery mechanism. Because banks and financial institutions are backing away from becoming market makers, Christian says this has resulted in a sharp reduction in liquidity during the auction process, creating a large discrepancy in prices. “There is something wrong with the process. You have a working spot market and then you have to stop that to then go over to this auction,” he added.

- Gold’s rally steadied earlier in the week on the back of U.S. jobs data that is consistent with the economy growing at 2 percent this year. “The U.S. jobs data was weaker than expected and these provided good support to gold until investors digested the data,” Brian Lan, managing director of GoldSilver Central, said over email. Other news comes from Centerra Gold this week, which reported a fatality at its Kumtor mine in the Kyrgyz Republic. According to Bloomberg, on April 11 a vehicle mechanic was fatally injured while inspecting a light vehicle pickup truck in the field.

Opportunities

- President Donald Trump had a few notable remarks this week, the first being that he will not brand China a currency manipulator, as he previously promised as part of his election platform. As for the second, he thinks the U.S. dollar is too strong, making the U.S. noncompetitive globally as other countries continue to devalue their currencies. Although the dollar dropped after these currency remarks, gold jumped around $8 on the news, potentially setting the backdrop for further gains.

- This week’s quote of the week comes from Secretary of State Rex Tillerson on the matter of chemical weapons in Syria: “The Russians are either complicit or incompetent.” Tillerson seems to have found his voice after enduring criticism of being silent and sidelined in the Trump administration. He traveled to Moscow to deliver his message of disappointment to Russia for its inability to deliver and oversee Syria’s supposed removal of chemical weapons. And just to make sure that anyone thought “59 and done” Tomahawk missiles launched into Syria was where the Trump administration was stopping, it was revealed on Thursday that the U.S. dropped the massive “Mother of all Bombs,” the largest non-nuclear bomb in the world, on suspected terrorist camps in Afghanistan.

- According to BMO Capital Markets, there will be a massive rebalance trade around the GDXJ ETF rebalances in June 2017, including significant demand for around 18 potential new additions, as well as a large selling of existing GDXJ names. There are some huge flows around these gold names, with an average daily trading volume of eight days of volume. The ETF will need to sell $3 billion worth of its existing holdings to buy the new additions, which will create a massive funding trade significantly impacting existing names. On this note, don’t think you can front run the front runners. The brokers, which are Authorized Participants to create the shares for the ETF, will spend the next eight weeks going short and long the expected index changes, largely excluding any outside parties from getting a piece of the trade. Speculators who show up to trade on the rebalance date likely won’t get the price they expect. So over the next eight weeks, we may see some market impact from the pre-rebalance of the index, but keep in mind the GDXJ ETF is about suppling beta to investors. They need the most liquid names to deal in, but this will be a great opportunity to pick up some small-capitalization, high-quality growth names that deliver alpha to investors.

Threats

- The threat of a government shutdown is looming. Government funding expires on April 28, reports Bloomberg, giving Congress five days to “unveil, debate and pass an enormous spending bill, or trigger a government shutdown.” Paul Brace, a congressional expert at Rice University, is even quoted as saying: “It was so much easier when all you had to do was oppose Obama.” There is an exception, the article continues, with a bipartisan group of lawmakers who have been quietly negotiating an omnibus spending bill that would fund the government through the end of the fiscal year on September 30. The border wall decision remains a wild card if it’s included in the budget.

- Although the bond market seems to be focused on what will happen once the Fed whittles down its investments in U.S. government bonds, perhaps more attention should be paid to an even bigger debt pile that could draw buyers away from Treasuries at just the wrong time, writes Bloomberg. “In overseas markets, more than $3 trillion of negative-yielding government bonds—which all but guarantee losses for buy-and-hold investors—have turned positive in recent months,” the article continues. Consequences for the U.S. bond market could be great, as foreigners who previously poured lots of money into higher-yielding Treasuries may be less inclined to do so now that they have “more viable fixed-income options at home.”

- Goldman Sachs maintains its overweight recommendation on commodities but sees a short-term decline for gold, reports Bloomberg. The bank sees the yellow metal falling to $1,200 an ounce in three months, on improvement in hard U.S. growth data and subsequent increases in real rates. Similarly, BMI Research says that the Fed’s rhetoric on balance sheet contraction, together with a stronger dollar, and declining credit growth and inflation expectations, are negative for gold.

April 11, 2017No Trade War Between the U.S. and China… Yet |

April 10, 2017Amid Global Uncertainty, Pay Attention to this Manufacturing Index |

April 5, 2017Gold Finds Strong Support from Negative Real Rates |

Energy and Natural Resources Market

Strengths

- Lumber logged a 12-year high this week surpassing its recession lows, according to the Wall Street Journal. In July of last year the commodity started to signal bullishness on the back of speculation surrounding the Trump trade. Fast forward nine months and U.S. lumber prices have hit their highest since the start of the of the 2007 housing crash, marking increased optimism amongst consumer demand, supportive demographics, and a robust housing market. In addition to the robust fundamentals from the consumer level, President Trump’s desire to boost infrastructure spending and renegotiate NAFTA will likely continue to push up domestic lumber prices. A positive read-through for lumber prices.

- The best performing sector for the week was the S&P/TSX Composite Gold Sub Industry Index. The index rose 4.4 percent on the back of rising gold prices this week as geopolitical risks take center stage of global financial markets, with investors seeking safe-haven assets.

- Yara International ASA, a Norwegian chemical company, was the best performing stock this week finishing up 4.9 percent. The stock rose on the back of being upgraded to a buy from various analysts.

Weaknesses

- Iron ore was the worst performing commodity this week dropping a whopping 15.1 percent and entering official bear market territory. The mineral has been in free fall since the middle of March as Chinese ports and mills have reported record inventory levels and concerns surrounding China’s outlook for construction and infrastructure demand.

- The worst performing sector this week was the S&P Super Composite Steel Sub Industry Index. The index fell 7.3 percent on the back of falling iron ore prices and doubt surrounding global demand for the metal.

- The worst performing stock for the week was Alcoa Inc., one of the world’s largest producers of aluminum. The company fell 8.1 percent on the back of worry surrounding industrial demand in China.

Opportunities

- U.S. crude oil inventories registered their biggest weekly fall so far this year, according to the U.S. International Energy Agency (IEA). Inventories finally dropped by 2.2 million barrels last week, breaking the record high unbroken run of stock builds throughout the first quarter. In an article by the Wall Street Journal, Saudi Arabia has told OPEC officials that it wants to extend the current agreement to further cut production for another six months at the May meeting. A bullish read-through for crude oil prices.

- Fear creeps back into global markets this week driving gold prices higher, according to Bloomberg. Safe-haven assets such as gold are beginning to return to the forefront of investors’ radar screens as risk factors ranging from geopolitical uncertainty surrounding Syria, political upheaval in Europe, and complacency in equity markets is beginning to force investors to seek protection in the case of a major negative event. To add further energy to the commodities momentum, comments from President Trump stating that the dollar is “too strong” in attempt to weaken the currency, is also weighing on various participants. All of which could bode well for higher gold prices, a positive read-through for gold prices.

- Natural gas bulls are beginning to come out of hiding, according to a research note by Macquarie Bank. In the bank’s note, it argues that natural gas may enter a bull market on lack of production growth while real demand growth has started to pick up, underinvestment in storage facilities, and the reality surrounding retirement of coal plants. Although no one holds a crystal ball, all factors listed in the report point to a bullish situation for natural gas prices in the near future.

Threats

- Chinese growth drivers are losing steam, according to a research note released by Macquarie Bank. The current upswing in commodity prices has forced participants to question how long can the current up-cycle in commodities run as key data points such as the producer price index (PPI) and consumer price index (CPI) are starting to weaken. PPI may have peaked in the month of February at 7.8 percent versus 7.5 percent for March on a year-over-year basis, which suggests weaker pricing power from commodity producers. A negative read-through for commodity prices from the world’s driver of growth.

- Hedge funds have extended bearish agricultural bets to a level not seen in almost two years, according to the Financial Times. With favorable weather forecasts, increased planting lift expectations of bumper harvests, and increasing evidence of oversupply across corn, soybeans and wheat, bearish positions outweigh bullish positions by 99,000 lots, according to this week’s data release from the Commodity Futures Trading Commission. Grains across Iowa are piled on runways, parking lots, and fields as the world deals with oversupply of agricultural commodities. A negative read-through from the grain complex.

- The U.S. Producer Price Index (PPI) came in lower than expected by the consensus this week, down 0.1 percent versus consensus expectations of up 0.1 percent, according to Bloomberg data. The main drag on the data point was a lack of pressure in the service sector which points to sluggish consumer demand. A negative read-through from the world’s largest consumer of goods.

China Region

Strengths

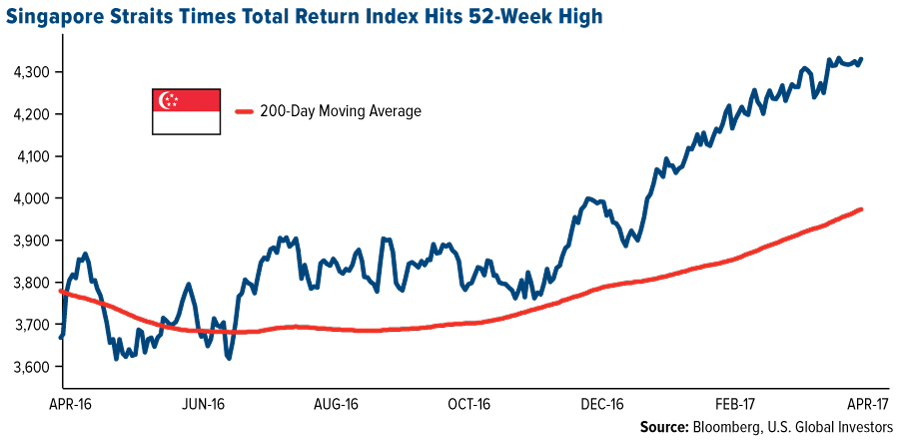

- Singapore’s Straits Times (Total Return) Index continues to bump up on its recent 52 week highs.

- The top stock in the Hang Seng Composite Index (HSCI) this week was Beijing Capital International Airport Co. Ltd. (694 HK), which rose 17.34 percent in that time. A recent Goldman Sachs note points out this jump is likely due to a “potentially strong result of its duty free tender.” The stock put in new 52 week highs on Wednesday and Thursday.

- March year-over-year imports and exports both beat in China this week. Imports came in up 20.3 percent, ahead of analysts’ expectations for a gain of only 15.5 percent, while exports came in up 16.4 percent, handily beating expectations for a 4.3 percent print.

Weaknesses

- Malaysia’s Industrial Production for the February period came in up 4.7 percent year-over-year, lighter than analysts’ expectations for a gain of 6.1 percent.

- The Philippines’ year-over-year exports dropped to an 11.0 percent gain for the February period, down from January’s 22.5 percent pace and shy of analysts’ expectations for a 19.4 percent print.

- February year-over-year retail sales in Singapore dropped 2.5 percent, missing expectations for a gain of 1.9 percent and down from January’s positive print of 2.0 percent.

Opportunities

- Bidding for the first two sections of Thailand’s rail line project with China may take place by August, reports Bloomberg, citing Thailand’s Transport Minister.

- U.S. President Donald Trump announced late this week that he will not seek to label China a “currency manipulator,” simultaneously contradicting campaign promises while easing a source of potential tension between the U.S. and China. “They’re not currency manipulators,” Trump stated.

- Next week we get a number of data out of China, including retail sales, industrial production, and new and aggregate financing, but investors will pay particularly close attention to next week’s first-quarter GDP number (survey expectations for which were recently raised to an anticipated 6.8 percent). We shall see.

Threats

- North Korea continues to hold attention. Trump called the pariah state a “problem” that “will be taken care of,” but, following his meetings with Chinese President Xi Jinping last weekend, he has also expressed optimism (“great confidence,” in fact) that China will help pressure North Korea. In the meantime, as Saturday marks the 105th anniversary of the birth of Kim Il-Sung, there is some speculation that the weekend may be cause for further missile tests.

- China’s first-quarter auto sales dropped for the first time in 17 years, Bloomberg reports, likely due at least in part to the Korean boycott and the increased sales tax this year.

- Hong Kong’s government is once again seeking to clamp down on homebuyers in the world’s least-affordable city, instituting new rules to prevent the purchase of multiple properties in a single contract and thereby skirt stamp duty rules.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 1.55 percent. Moody’s revised gross domestic product growth up to 2.6 percent from 2.2 percent in 2017. According to the rating agency, the Turkish government undertook substantial fiscal stimulus and the central bank relaxed credit terms to overcome the expected loss of confidence following the failed coup attempt; this reversed the decline in household spending.

- The Turkish lira was the best performing currency this week, gaining 2 percent against the dollar. The currency gained as Turks prepare to vote on constitutional changes this weekend that will give President Recep Tayyip Erdogan executive powers.

- The industrial sector was the best performing sector among eastern European markets this week.

Weaknesses

- Russia was the worst performing country this week, losing 3.7 percent. During a G7 meeting in Italy, Britain and America proposed new sanctions against Russia following the chemical attack in Syria, but failed to win immediate support from European allies. Russian equites look disconnected from Brent crude oil, selling off due to increasing political tension between Russia and the U.S. over its strikes in Syria. Brent gained 1 percent in the past five days.

- The Hungarian forint was the worst performing currency this week, losing 75 basis points against the dollar. The European Commission threatened Hungary with legal action over its move against a university and foreign-sponsored non-governmental organizations.

- The consumer staples sector was the worst performing sector among eastern European markets this week.

Opportunities

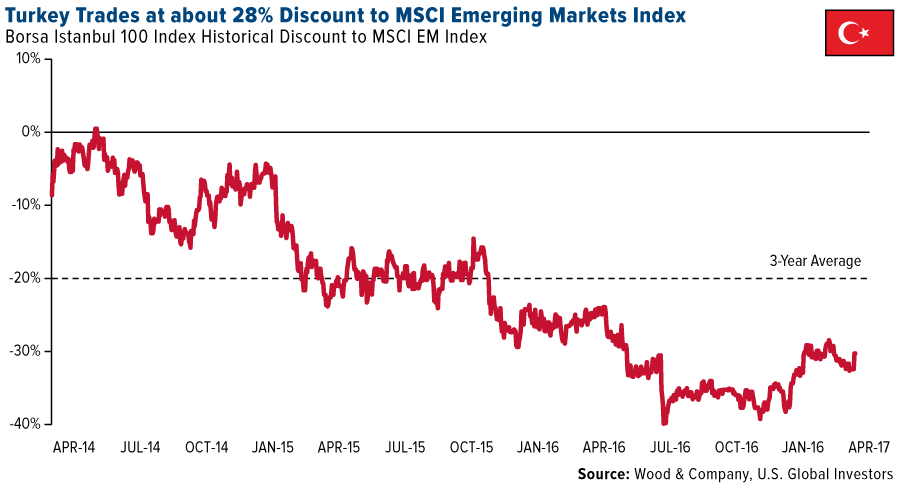

- Turkey will head to the polls this Sunday to vote on executive presidency. Based on Wood & Company research, a “Yes” outcome should be positive for the markers in the short term as the referendum will be out of the way and some uncertainty will be removed from the market. Turkey trades at about 30 percent discount to MSCI Emerging Markets, versus a three-year average trading discount of 20 percent. There is arguably room for a rally in the markets as long as global risk appetite remains strong.

- Preliminary April purchasing managers’ index (PMI) data for the eurozone will be released next week, and expectation is that once again we will see readings well above the 50 level that separates growth from contraction. March Manufacturing PMI was recorded at 56.2, Service 56, and Composite 56.4.

- There is geopolitical noise in Russia but economic fundamentals should be supportive for the ruble going forward, according to Jason Schenker of Prestige Economics LLC in Austin, Texas. The ruble weakened the most in the month last Friday after tension increased between Russia and the U.S. over its strikes in Syria, but such weakness is only short-term, he said. The global economic recovery will support oil and metal prices, giving a boost to Russian growth. Schenker sees the ruble strengthening to 55 against the dollar by the end of the second quarter and to 52 by the end of this year. It traded at 56.9 on Wednesday.

Threats

- Euro-area industrial output shrank 0.3 percent in February from the previous month, versus the predicted 0.1 percent gain. January’s reading was revised down from 0.9 percent to 0.3 percent. The year-over-year number came in at 1.2 percent, less than the expected 1.9 percent.

- Staff level agreement between Greece and its creditors could be reached within April/May and a comprehensive deal by June. The market will likely react positively once the final agreement is made, but most importantly Greece needs to gain market access, or Greek bonds must be included in the quantitative easing program. The current bailout program ends in summer of 2018, and if Greek sovereign yields do not fall below 4-5 percent by the end of this year, this could imply that Greece may not gain market access and the discussions over a potential fourth bailout agreement would begin.

- Hungarian President Janos Ader signed into law a measure cracking down on foreign universities that sparked one of the biggest rallies against Prime Minister Viktor Orban’s government by protesters demanding he respect democratic norms. The new rule is aimied at shutting down Central European University, founded in 1991 by Hungarian-born investor George Soros who promotes human rights and government transparency. Critics say that the bill mimics a 2012 law in Russia that was the first step in an exodus of U.S.-based and other non-governmental organizations there.