“Earnings don’t move the overall market; it’s the Federal Reserve Board… focus on the central banks and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.”

– Stan Druckenmiller

“As I look out over the coming years, I am convinced that we’ll see the blowing up of the biggest bubbles in history, including those of government debt and government promises, and not just in the U.S. but all over the world, leading to an eventual global crisis of biblical proportions – although it isn’t clear what the immediate cause of the crisis will be. Right now I am looking at Italy with intense focus.”

– John Mauldin

“Bull-markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.”

– Sir John Templeton

I’ve fielded a large number of investor questions recently around tax cuts and earnings. The idea is that tax cuts, for both corporations and individuals, will significantly improve corporate earnings and thus propel the market higher.

I attempt to answer that question inside today’s piece. The Stan Druckenmiller quote, one of the world’s greatest performing hedge fund managers, tips my hand but do read on. We’ll also look at what happens to equities in a rising rate environment and a fun chart you may like to share with your clients about an investor’s “emotional cycle.” If bull markets die in “euphoria,” I argue we are just not quite there yet.

But before you dive into the heart of this week’s On My Radar, a risk we’ve been talking about for some time, underfunded pensions, just took a big step forward.

The California Public Employees Retirement System, better known as CalPERS, this week stated that a 7.5% annual return is no longer realistic. Finally, amen, right on. And as my kids would say when they were young, “duh.”

What is CalPERS? It is an agency in the California executive branch that manages the pension and health benefits for more than 1.8 million California public employees, retirees, and their families. At $300 billion, it is the largest pension fund in the U.S.

You probably have a close friend that will always tell it to you straight. She or he will look you in the eye and tell it like it is. Sometimes we like the advice, sometimes it is really “tough love” and it hits us hard. But trust matters, honesty matters and we know that the toughest advice is often the best thing for us. Dig deep, reflect, stand up straight and step forward on a better path.

Let’s cheer this week’s “tough love” announcement from CalPERS, as reported in the WSJ, America’s Largest Pension Fund: A 7.5% Annual Return Is No Longer Realistic. Over coffee with Susan this morning, I explained (hopefully in plain English) what this means. I’ll try to write this in a way that you may share with your clients. This is big… really big.

Top officers of the largest U.S. pension fund want to lower their investment targets, a move that would trigger more pain for cash-strapped cities across California and set an increasingly cautious tone for those who manage retirement assets around the country.

Think about this: Promises were made to school teachers, fire fighters, police and other state employees. Work for a certain number of years and receive a monthly pension check for the rest of your life. Pension managers are considered experts at managing money and the largest plans, like CalPERS, attract the greatest talent. They strive to achieve a certain return over long periods of time. The lives of current retirees and future retirees are counting on the promises that have been made to them.

Money comes into the pension fund each month from current workers and money goes out of the fund to pay current retirees. The smart guys in charge have to crunch the numbers and generate returns so that the right amount of money is available to take care of today’s retirees and grow the pool of money in a way that takes care of tomorrow’s retirees. The state pays into the plan as well just as your employer or you, if you’re self-employed, might pay into a defined benefit plan or 401k (some percentage form of match). If you have a defined benefit plan, your plan must be fully funded in a way that makes sure the obligations can be met.

Kind of standard stuff except when the plan falls way behind the actuarial numbers calculated to fulfill the obligation. To meet those calculated numbers, an estimated return number is plugged into the spreadsheets and over many years that number was around 8%. But 8% hasn’t worked over the last 16 years and with bonds yielding just 2%, as I’ve written about frequently, there is no way to hit those return bogies over the coming seven to 10 years.

See here and here for forward probable returns or I’ll cut to the chase and tell you it’s 3% to 4% for stocks and 2% for bonds (we’ll call it now 2.50% after the recent rate spikes). Best case 4% not 7%, not 7.50%, not 8% as many plans are calculating today.

The problem is the “pig in the python.” Those damn baby boomers (to which at age 55 I am on the younger side of that generation). But we are many and the front end of the wave is hitting retirement age. The math is going the wrong way. Low returns, more retirees. CalPERS finds itself just 68% funded versus where they need to be to meet the contractual promises they’ve made. And 68%, while not good at all, is better than many.

If returns are weaker than the return assumptions suggested, then there is simply less money in the kitty available to meet the retirement payments. Eventually, something has to give and we are getting closer to that tipping point.

More from the WSJ:

Chief Investment Officer Ted Eliopoulos and two other executives with the California Public Employees’ Retirement System plan to propose next Tuesday that their board abandon a long-held goal of 7.5% annually, according to system spokesman Brad Pacheco. Reductions to 7.25% and 7% have been studied, according to new documents posted Tuesday.

California Governor Jerry Brown said in a statement to the Journal, “There’s no doubt CalPERS needs to start aligning its rate of return expectations with reality.”

A reduction in CalPERS’ return target to 7% or 7.25% would have real-life consequences for taxpayers and cities. It would likely trigger a painful increase in yearly pension bills for the towns, counties and school districts that participate in California’s state pension plan. Any loss in expected investment earnings must be made up with significantly higher annual contributions from public employers as well as the state.

If the assumed rate of return fell to 7%, the state and school districts participating in CalPERS would have to pay at least $15 billion more over the next 20 years, said spokeswoman Amy Morgan. That number doesn’t include cities and local agencies.

Can you imagine how many people are going to be affected? Here’s the bottom line. The pension system, across our great nation, is underfunded and in trouble. The choices will be to:

- raise taxes

- raise the contribution requirements on current state employees

- reduce the amount of the retirees monthly pension check

- or a combination of all three

That’s the direction we are heading. I’ve been writing for some time about the coming pension crisis. Well, the big guy just stepped up to the microphone. That small move from a 7.50% return assumption to a 7% return assumption leads to a massive increase in the money that will need to be injected into the plans to cover the retirement benefits that have been promised.

Imagine the ripple effect across states, to cities, to small towns. The pension boards are going to have to follow the big boys and reduce their return assumptions. Higher taxes are coming at the state and local level. That or the elected officials will lose the votes of millions of pissed off retirees.

More from the WSJ:

Lowering the assumed rate of return by just a quarter of a percentage point would likely increase annual CalPERS payments made by one town, Costa Mesa, Calif., by up to $8 million, said former Mayor Steve Mensinger, who left office Tuesday after losing a bid for another term. That would likely mean budget cuts for Costa Mesa, which already spends more than 20% of its $120 million operating budget on pensions, according to Mr. Mensinger.

A Costa Mesa spokesman said “we will be closely monitoring” what CalPERS’ board does and “will be analyzing their proposal when it is provided to us.”

A drop in CalPERS’ rate of return assumptions could also put pressure on other funds to be more aggressive about their reductions and concede that investment gains alone won’t be enough to fund hundreds of billions in liabilities.

Well, thank you, big guy. Appreciate the honesty. It hurts but it is a move in the right direction.

Pensions have long been criticized for using unrealistic investment assumptions, which proved costly during the last financial crisis. More than two-thirds of state retirement systems have trimmed their assumptions since 2008, according to an analysis of 127 plans by the National Association of State Retirement Administrators. The average target of 7.56% is the lowest since at least 1989. The peak was 8.1% in 2001.

I’ve been on multiple panels over the last few years, generally with smaller pension plan managers, who claim that hitting their 8% bogie is not a problem. I argued back with a simple “no way.” And dove into probable return assumptions. My advice was to get real.

Well, the big elephant in the room has been exposed. The big guy just rung the bell. Expect higher taxes on the state and local level. And expect emotions to rise.

My friend Danielle DiMartino Booth puts it this way:

Two weeks ago, Real Vision aired an interview conducted with me right after the elections were held. Many subjects were covered over the hour. But the one that struck the loudest chord with viewers was the issue of underfunded public pensions, which stands to reason given the headlines of late.

But the reaction from viewers was anything but expected. The bile, the contempt, the malicious back and forth in the comments between public and private sector workers stunned me speechless.

It was the teachers, firefighters and policemen vs. you name the line of work among those in the private sector. No side won in the event you’re holding your breath. And both made great points. Promises made should not be broken. Teaching our children, protecting our citizens from harm – noble, often thankless professions without question. By the same token, why should someone who has worked their entire life swallow a spike in their property taxes to foot the bill? It’s not as if the investments in their 401ks are not on the same vulnerable footing as those in pensions.

The outrage prompted a private conversation with a great friend who also happens to be the most insightful municipal bond strategist out there (a subtle way to say the following comments must remain anonymous).

The first order of business was a correction to my concern that Uncle Sam would be forced to bail out weak pensions in the end: “The federal government is most definitely NOT going to write checks to state and local government! If anything, the current lineup on the Hill wants to move more responsibility to the states (and they have no money anyhow).”

There’s no arguing with the no money part. But indulge the rest of the conversation as here’s where we get down to causality, to culpability.

“I would lay more blame on your friend, the Fed. [Danielle worked for many years at the Fed.] Remember that public pensions were funded in 2000 and prior to that, earning a seven-to-eight percent return on assets was no sweat.?For the last 15 years though, we’ve had nothing but volatility and low interest on fixed income, the place where conservative investors are supposed to go to deal with retirement investment.?This has clobbered long-term investors of all shapes and the feedback to the economy is not fully being taken into account (in my opinion).? If you are approaching retirement (read: baby boomers) and know you don’t have enough money in your 401k, you are not likely to run out and buy stuff.”

Few would dispute that Keynes’ Paradox of Thrift is alive and well. The ravages of the Fed’s low interest rate policy have forced an increasing number of Americans to save more to offset what they are not earning on their savings. The resulting decline in aggregate demand goes a long way to explaining the current economic recovery’s refusal to accelerate – even factoring in the third quarter’s 3.2-percent pace, current forecasts calling for 2.3-percent growth in the fourth quarter leave 2016 full year growth just shy of the two-percent mark.

But that’s the point of the Paradox. The millions of baby boomers retiring are going to cash, as they should to provide for this little thing called security. Still, the forced frugality sets an anything but virtuous cycle in motion, glaringly reflected in the economic health of the generations behind the boomers, an alarming number of whom still live with their parents. Bunking up remains altogether too common, which of course reflects mobility, or better said, the lack thereof.

The tie that binds the generations comes down to one word: debt. That’s where the Federal Reserve has inflicted the greatest damage.

Here is the link to Danielle’s Real Vision TV interview – Underfunded government pensions to the tune of $1.3 trillion, with a gap that just can’t be filled, is the ticking time bomb facing the US economy, which faces dramatic cuts in public services.

OK, we’ve got issues. The pension problem is real. Debt’s the biggest global issue. We remain near the beginning of secular (long-term) debt deleveraging cycle. We will watch for signs of a beautiful or an ugly deleveraging. I’m praying for beautiful.

Grab a coffee… click through and you’ll find a couple of charts showing what happened to equities in prior rising rate and inflation environments, Gundlach and Trade Signals. I appreciate the time you spend with me each week. I hope you find the information helpful.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Included in this week’s On My Radar:

- Investing in a Rising Interest Rate Environment

- Gundlach – The Tipping Point for Stocks and Bonds

- Free Money and Economic Growth

- Trade Signals – Summary of this Week’s Trade Signals by Asset Category (posted 12-14-2016)

Investing in a Rising Interest Rate Environment

What tends to happen to equities in a rising rate environment? With the Fed raising interest rates again this week, this is a question on many investor minds. My standard answer is the “two steps and a stumble” rule, which means that when the Fed raises the federal funds rate the first time, there is little impact on the equity markets but when they raise rates twice, that’s when the stumble begins.

Think about what Stan Druckenmiller said above, “Earnings don’t move the overall market; it’s the Federal Reserve Board… focus on the central banks and focus on the movement of liquidity…”

John Mauldin highlighted a section from a recent On My Radar post about valuations. You can find his piece titled, The Trump Rally Will Morph.

If you are not reading John’s weekly Thoughts from the Frontline, I highly recommend you do. It’s been a must-read of mine since I met him in 2000. He’s become a great friend… He’s really good!

I’m going to borrow from John and share a section as it ties in nicely to what is on my mind today – the Fed and rising interest rates. The section is titled, Something’s Gotta Give:

So far, we have seen compelling evidence from several sources and methodologies that US stocks are overvalued. Yet just in the last month we saw investors react to the US election by bidding the benchmarks up to new all-time highs. This implies they expect even higher prices next year. Can it happen?

Louis Gave of Gavekal took on that question in a lengthy and masterful presentation last week titled “Something’s Gotta Give” (article is behind paywall). He had more questions than answers.

The prime question, says Louis, is whether the US economy is a “coiled spring” ready to bounce higher based on the new political environment. We know changes are coming. Are they the kinds of changes that will help the economy, and therefore corporate earnings, grow enough to justify sharply increased stock prices in an already overvalued stock market?

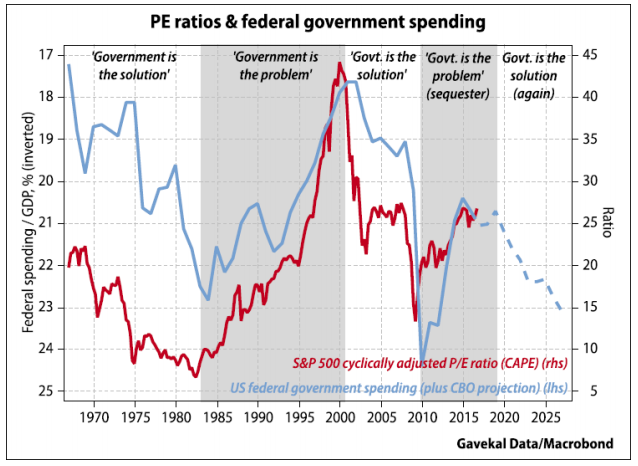

Louis doesn’t have a firm answer, but I think it’s fair to say he is dubious. I’ll share with you just two of his 63 slides. The first one concerns government spending. Part of the present rally comes from expectations that Trump and the Republican Congress will launch an infrastructure stimulus program and also raise defense spending. That’s not a sure thing. Even if it were, Louis points out that higher government spending historically correlates with lower P/E ratios.

Some people will dispute this. You can argue that the higher spending is a response to the lower growth that caused the low P/E ratio. But if you believe that government is by nature less efficient than the private sector, then higher government spending will mean more capital misallocation, which is not good for stock valuations. A second justification for the current rally is that new policies and perhaps delayed Federal Reserve tightening will mean higher inflation. People say this will be positive for stocks. With this chart Louis again says, “Not so fast”:

The vertical shaded areas are periods of rising inflation. Other than 1979–81, we see stocks falling in those periods, not rising. Louis says this is because inflation misallocates resources. Companies have to hold more inventory, spend more on payroll and benefits, and otherwise take their eyes off more important goals.

Of course, the Trump administration will do more than just raise spending. Trump intends to reduce taxes, roll back excessive regulation, and otherwise make the US more business-friendly. He will go about it differently than other Republicans would. His intervention in the Carrier outsourcing indicates that this is not going to be a conventional GOP White House. We’ll see how well his approach works, and whether other changes can outweigh the drag caused by higher spending and inflation.

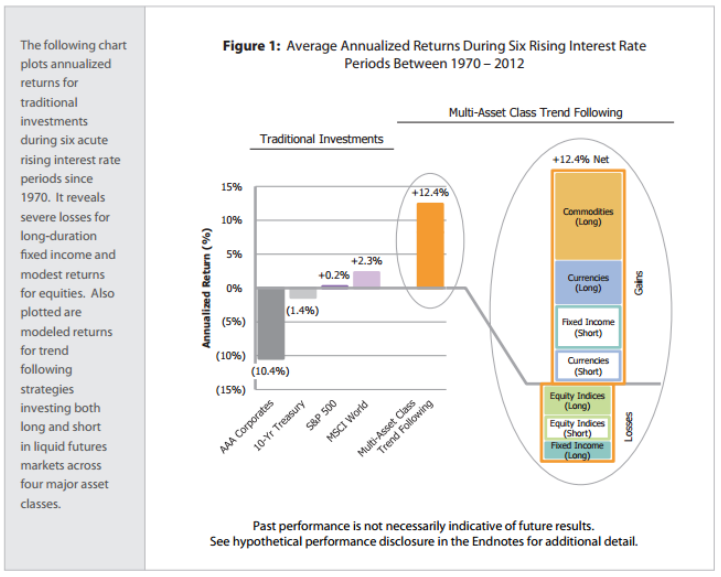

Investing in a Rising-Interest-Rate World. My friends at Welton Investment put out very thoughtful and useful papers, and I always make a point to read them. They are chock-full of useful charts and historical insights. In the latest one they offer some cautions to the recent euphoria of the Trump Rally (see more later). It turns out that equity returns are not all that durable in rising-interest-rate environments. Of course, one could argue that a 25-basispoint increase from already low rates every six months or so does not really correspond to any historical interest-rate increase cycle, but that’s a topic for another letter. Here is a chart that shows average returns during the last six rising-interest-rate environments:

Source: Mauldin Economics

OK, that will get you thinking. I see stagnation (low growth and rising inflation) in our future.

Gundlach – The Tipping Point for Stocks and Bonds

Jeffery Gundlach’s live December 13, 2016 webcast titled, Drain The Swamp (slide deck here).

Following in bullet point format are highlights:

- Gundlach predicts trouble for the equity, corporate and junk-bond markets if the yield on the 10-year Treasury bond goes above 3% in 2017.

- Even the housing market would suffer. That rate increase would translate to a 30% increase in mortgage payments for homeowners from the July levels, according to Gundlach.

- This would hurt real estate sales, he said, since there is “no way” the median income would rise by nearly 30%.

- Corporate bonds, as measured by the ETF LQD, have done poorly since the market bottom on July 8, returning -5.4%, but the junk-bond ETF JNK “massively” outperformed, returning 3.6% since that date.

- But he said if the 10-year bond, which closed at 2.46% on the day he spoke, goes above 3%, then junk bonds would “fall into a black hole of illiquidity.”

- Investment-grade corporate bonds are already “as overvalued as it gets,” he said, and are threatened by excessive leverage in the corporate sectors.

- A push above 3% would cause investors to rethink their equity holdings and shift allocations to bonds.

- Financial services – specifically banks – would suffer because their dividend yields would be significantly less than 3%.

- Gundlach said that “3% is a really big number on the 10-year. It won’t happen soon, but it may happen in 2017.”

On the Trump win:

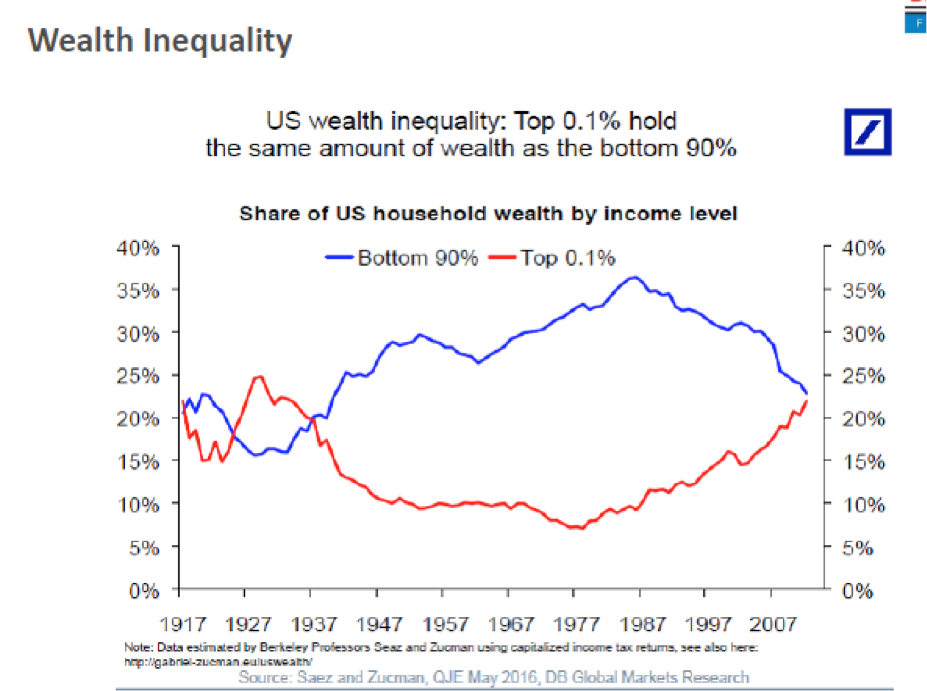

- Gundlach said that the election results could be summarized in this chart:

- Over the last 30 years, the share of wealth for the bottom 90%, by income level, has gone from 35% to 22%, while the share for the top 0.1% went from 5% to the same 22%.

- The bottom 90% have as much wealth as the top 0.1%.

Gundlach compared the economy that Trump will inherit to what Reagan faced when he took office in 1982:

- In both cases, GDP growth was slow, but Reagan faced much higher inflation and bond yields.

- Stock market P/E ratios were in single digits for Reagan, but Trump will take office with a multiple of approximately 20.

- Debt-to-GDP was a mere 31% in 1982, versus the 105%.

- He added, “People have fallen asleep on this topic since 2011,” when government shutdowns were a common topic of conversation.

- Trump’s policies threaten to push debt levels higher, as he will need to fund his infrastructure initiatives and plans for increased defense spending.

- “There is a lot of debt in the economy and it will be hard to get a debt-based boom,” Gundlach said.

- Manufacturing jobs are down 27% since NAFTA was signed in 1993, Gundlach said, and he doubts that Trump can bring back those jobs.

- “A lot of those jobs have been lost to robots,” he said, or will be lost to innovations such as driverless cars.

- Trump has said he will attack the trade deficit, but Gundlach was skeptical he would make much progress toward that goal, since China is our biggest trading partner and it is unlikely we can increase exports enough to offset Chinese imports.

- Gundlach said that Trump’s plan to decrease the corporate tax rate may have a limited impact on the deficit, since those taxes are only 11% of federal revenues; the bulk of federal tax revenue comes from individuals, he said.

- Trump has talked about building a stronger defense, but that too may not have a big effect on GDP growth. Defense spending has been incredibly stable since 1970 on an inflation-adjusted basis, Gundlach said, but only about 3% of GDP, plus or minus 1.5%, has been allocated to defense.

- Net interest is an incredibly small part of federal spending, Gundlach said, and hasn’t grown in the past 15 years on an absolute basis.

- But Gundlach has predicted that 10-year rates would go to 6% in the next four to five years, about the time of the next presidential election, and he said that level of rates “would be a problem.”

- See infrastructure spending.

- More aggressive spending is “what Trump campaigned on,” Gundlach said. “That will lead to another leg up on debt, which is not friendly for bonds.”

- The market has warmed up to that idea. Gundlach said that 10-year rates have risen from 1.72% to 2.53% since Trump’s victory. (It hit a 2.62% yield yesterday.)

- Gundlach predicted an equity sell-off around inauguration day. But he added that he doesn’t expect a recession, although one often occurs in the first year of a new president’s term.

The global markets and Fed policy

- Conditions in Europe reflect instability and the risk of a fracture in the European Union (EU).

- Gundlach cited polls showing that European citizens gave a mixed review on whether they have a favorable view of the EU, although in some countries, such as France, the view is very unfavorable.

- With elections coming in 2017, Gundlach said he would closely monitor developments in France.

- Sovereign debt yields in Europe are up 60 basis points since July, he said, and spreads have widened from 1.5 to 1.9%.

- Spreads in Italy are a clear indicator of the likelihood of it leaving the EU, he said, but he did not predict if or when that would happen.

- Italian bond yields are lower than those in the U.S. and Gundlach said he can’t imagine why anyone would own Italian bonds.

- Bond yields are rising globally, he said, and noted that yields in Japan are now positive.

- He is not sure past is prologue, but Gundlach said that in prior rate cycles the Fed has tightened until “something broke,” and then there was a “massive reversal.”

- The question is what level of the Fed funds rate will cause something to break. People are used to very low rates, he said.

- Don’t think that if rates rise there will be a positive stock market based on an expectation of economic growth, Gundlach warned.

On Inflation

- Inflation is rising, he said, but it is not driven by food or energy prices. Instead shelter and other “sticky” things are pushing inflation higher. If food and energy prices spike, Gundlach said inflation could be over 3%.

The overarching question

- The big uncertainty for investors is the long-term trend in interest rates. Is the 35-year bull market in bonds over or will the current spike in rates be a temporary phenomenon?

- Gundlach did not give a precise answer to that question. A lot depends on if and when the 10-year yield reaches 3%.

- But he was clear about the reasons behind the general trend in rates.

- Global yields are on the rise because markets have realized a belief that “negative-interest rates are with us forever” has lost out to a recognition that they don’t work, he said.

- In regards to negative rates, he said, “You can’t keep doing the thing that doesn’t work.

- We’re moving on to fiscal stimulus.”

“Free Money” – Do Larger Federal Budget Deficits Stimulate Spending? Depends on Where the Funding Comes From, By Paul Kasriel

I’ve hit you with a lot of information today. Print out this section and come back to it from time to time. I think this is what we are likely to see in our near future. Free money (print and spend) except this time the money is going to go into the economy and not get parked at the banks. And we are going to see Trump tax cuts. Nothing is certain but I see both as highly probable.

If you missed this Outside the Box from John Mauldin, I share it with you next. But first take a second to reheat that coffee or go for a second cup.

John introduces Paul’s piece:

In the true spirit of stepping outside the box, today’s OTB is a counterintuitive argument against the concept that fiscal deficits and/or infrastructure spending constitute effective economic stimulus. It comes from Paul Kasriel, who was one of my favorite reads when he was at Northern Trust, and I am glad he continues to write in “retirement.” He always has a way of looking at things from different angles than everybody else does.

Paul is a self-confessed reformed Keynesian. He likens his own longtime tendency to revert to Keynesian macro analysis to the damnable difficulty of fixing a faulty golf grip: “If you start out playing golf with an incorrect grip, you will have a tendency to revert to it on the golf course even after hours of practicing at the driving range with a correct grip.” But as he struggled with his unfortunate tendency over the years, Paul was forever reminded of a question a fellow student asked him when Paul delivered his very first homily on the wonders of Keynesianism to an undergraduate political science class: “Where does the government get the funds to pay for the increased spending or tax cuts?”

As Paul himself notes, the post-election US stock market rally has been due in part to the expectation that the Trump administration will enact simulative fiscal policies, which in turn will jumpstart growth. Paul begs to differ. He tells us that after some years out in the real world, he realized that tracing through where government gets the funds to finance tax cuts and increased spending is the most important issue in assessing the potential effects of simulative fiscal policy. And, to cut to the chase, his conclusion was and remains that “Tax-rate cuts and increased government spending do not have a significant positive cyclical effect on economic growth and employment unless the government receives the funding for such out of “thin air.” (emphasis mine)

“Thin air.” You know, that stuff they bottle at the Federal Reserve, slap a fancy label on, and sell by the boatload. Or that emerges – POOF! – from banks as they create credit.

Paul engages us in a thought experiment to make his case, and I think I’ll just step aside and let him lead the thinking. He got me thinking, that’s for sure.

John Mauldin, Editor, Outside the Box

The letter got me thinking and I found myself nodding my head in agreement. Tax cuts and free money. We may likely get them both.

Click on Do Larger Federal Budget Deficits Stimulate Spending? Depends on Where the Funding Comes From, by Paul Kasriel

It’s worth the read.

Trade Signals – Summary of this Week’s Trade Signals by Asset Category (posted 12-14-2016)

S&P 500 Index — 2,271 (12-14-16)

Equity Markets: The overall trend remains bullish as measured by the CMG NDR Large Cap Momentum Index (a trend-based indicator), the 13/34-Week Moving Average Trend and Volume Demand (more buyers than sellers). Don’t Fight the Fed or the Tape (Trend) is neutral.

Investor Sentiment: Investor sentiment is an indicator designed to highlight short-term swings in investor psychology. Current readings show excessive optimism. The objective is to identify trading extremes that may be used for trading or hedging purposes. Current readings suggest it is a time to hedge. More is explained when you click through to the charts below.

Fixed Income: We’ve done a great job at avoiding the large declines that have hit the bond market. The Zweig Bond Model (ZBM) moved to a sell signal on October 12, 2016 and remains in a sell today. The sell-off in high grade bonds has increased. The yield on the 10-year Treasury has moved from 1.37% in July 2016 to 2.42% today (having peaked at 2.51% recently). The CMG Managed High Yield Bond Program remains in a buy signal. The trends in HY funds and ETFs is bullish.

CMG Opportunistic All Asset Strategy. Here is what we are currently seeing:

- Across equity asset classes, the strongest relative strength is in Small Caps, Financials (Regional Banks), Mid-Caps and Technology.

- The portfolio is 92% positioned in equities and 8% in “MINT” (a short-term bond fund ETF). It can move to 100% fixed income or 100% equities.

- See the allocation pie chart below. You can follow the daily, weekly, monthly and annual performance of the CMG Tactical All Asset Index here.

Posted each Wednesday, Trade Signals looks at several of my favorite stock, investor sentiment and bond market indicators. It is my weekly risk management dashboard, designed to keep me better in sync with the major technical trends. I hope you find the information helpful in your work.

Click here for the most recent Trade Signals blog.

Concluding Thought and Personal Note

“Where you want to be is always in control, never wishing, always trading, and always, first and foremost protecting your butt.”

“I believe the very best money is made at the market turns.

Everyone says you get killed trying to pick tops and bottoms and you make all your money by playing the trend in the middle.

Well, for twelve years, I have been missing the meat in the middle but I have made a lot of money at tops and bottoms.”

“At the end of the day, the most important thing is how good are you at risk control.”

“The whole trick in investing is: “How do I keep from losing everything?”

— Paul Tudor Jones

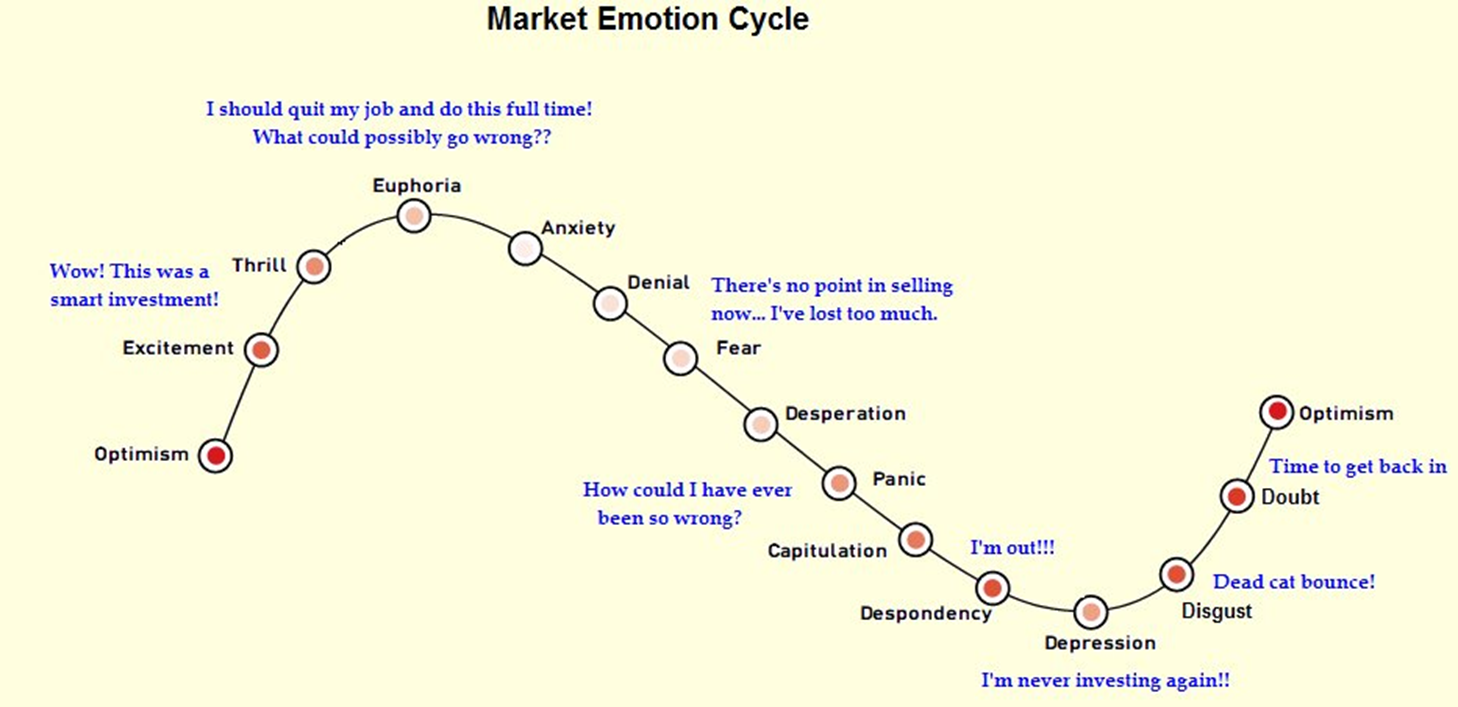

Euphoria? I just don’t think we are there yet. Take a close look at the next chart. I think we are somewhere between “optimism” and “thrill”… but that is just a best guess.

Keep Sir John’s sage advice front of mind, “Bull-markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.”

I like Mauldin’s “diversify to trading strategies idea.” However, I openly disclose that I am biased as I’ve been a trend-following momentum investor since the early 1990s.

Why always such a focus on risk? It is my belief that the most important investment lesson is to understand how math compounds over time. To this end, I wrote a piece titled, The Merciless Math of Loss. I hope you find it helpful and share it with your kids.

Valuations are high and forward returns low. We find ourselves in the debt bubble of all bubbles — here there and everywhere. It chokes growth. I believe Ray Dalio has it right, we are in a secular debt deleveraging cycle. They happen maybe once in a generation.

BTW, Google “How The Economic Machine Works” by Dalio. Share that one with your kids as well.

It is going to be interesting to watch how this plays out. Risk remains high. Stocks likely have further to run, however, it is prudent to hedge that equity exposure (and/or use Paul Tudor Jones 200-day moving average rule to “control-losses”, tactically trade bond exposure (due to the ultra-low rates and risk of loss) and diversify to a handful of trading strategies.

I fly to Denver tomorrow evening and praying I get a four-wheel drive rental. The car rental company says it’s a 90% probability. My head of research and I will land and drive immediately to Vail for a day of skiing before a few meetings on Monday, December 19. Snow is in the forecast and I am really excited to ski. Hopefully, many feet of snow. If you’ve ever powder skied, it’s like floating on a cloud. Wish we could bottle up that feeling and sell it to the world.

I’ll be in Colorado on January 8-11 attending an industry event with a handful of peers. OK, it is a sponsored event from one of our business partners – back to Vail. I know… but why not live. The Inside ETFs 2017 Conference in Hollywood, Florida is up next on January 22-25. I will be presenting on gold (which is in a confirmed downtrend – I’ll share a few ideas on how to trade gold). If you are planning on attending, please let me know. I’d love to grab a coffee or better yet a good beer with you.

Yesterday was my father’s birthday. He’d be 81 today. Prostate cancer took him nearly six years ago. I miss him and sure wish he was here. Happy birthday, Pop! I’ll be taking a ski run or two with you in mind on Sunday – let it snow!

Wishing you and those you love most a wonderful weekend!