“You diversify. You have a whole bunch of uncorrelated investment bets.

And then you understand it (the situation) as best you can.”

— Ray Dalio

I had a long talk with an advisor client this week about portfolio construction, the economy, the debt cycle and what to do. I’m sure you are having similar conversations with your clients. In the “what you can do” category, I shared with my friend that the best advice, at least to me, is summarized in Ray Dalio’s quote above.

On Monday, I was on Fox Business Network’s “Countdown to the Closing Bell” with Liz Claman. As I walked onto the set, there was a video of a ballplayer rounding third base who starts to stumble as he crosses home plate and then flops to the ground. The comical flop was replayed a few times as Liz announced, “Stay tuned, our next guest thinks the market may be headed for a flop.” Ugh, I thought to myself. Here is the short interview:

[drizzle]I remember my college soccer coach, Walter Bahr, hammering into us the idea that soccer is a game of opposites. Fake left to move right. If the flow is moving this way, look to see what has opened up over there. Perhaps that is why the great Sir John Templeton’s sage words continue to ring in my head today. I met him early in my career and he told me, and millions since:

“The secret to my success is that I buy when everyone else is selling and I sell when everyone else is buying. …Do that and you will be one of the best brokers in the business.”

Of course, he warned, it is far easier said than done. Same with soccer. What seems logical and easy is really not so easy to execute.

I met Sir John at the Union League in Philadelphia in 1985. Thinking back to that time, investors had just entered the greatest of all bull markets. Except none of us knew it.

Few investors were interested in stocks. Mutual funds charged 6% commissions and it cost about 2% to get into and 2% to get out of a stock trade. Buy-and-hold was an unpopular concept. Then, investors put money in real estate and gold.

Front of mind was the 1966 to 1982 long-term bear market. Front of mind was Paul Volker, inflation and interest rates in the mid-teens. Everyone knew you had to be a stock trader if you were to have any success in the equity markets. I sold a lot of municipal bonds. I remember my manager making me sell the Merrill Lynch Basic Value Fund. A rough “cold call” to make. Frankly, I could have/should have put my clients into a 30-year zero coupon Treasury bond yielding 16% and called it a day.

Today, the common belief is that low-fee passive investing is the way to go. Today, money is flooding into bond funds and ETFs at record pace to earn record low yields. We humans are herd beings. Investing is a game of opposites. It’s time to fake left and move right.

Think too about this: In the early 1970s everyone flocked to the “Nifty Fifty” stocks (the 50 popular large-cap stocks on the NYSE). It was tech in the late 1990s. Remember how displaced the value managers felt from 1995 to 2000? It was the place to be from 2000 to 2010. It is fixed income and passive investing today. Hot for now. The trend will change.

If you didn’t get a chance to read last week’s OMR, “Are We at the End of a Long-Term Debt Cycle?” you can find it here. I’m pretty critical about what I write, but this is one piece I wrote that I felt good about when I reread it the next morning. And the number of positive comments, always appreciated, were higher than normal (please know I appreciate the negative ones as well).

Show that OMR to your clients, if you feel it’s appropriate. The idea is not to go to a place of fear, the idea is to remind them of the current state, defend diversification (when they call you upset their diversified portfolio isn’t beating the S&P) and prepare them for opportunity.

To that end, last Monday I also did an interview with TheStreet’s Gregg Greenberg. I shared a few stock ideas – four stocks on my personal best ideas shopping list. Not a recommendation for you to buy or sell any security! It is my intention to buy them in my personal account when the next recession creates the next great buying opportunity.

The Fed, the global central bankers and our elected officials may be able to hold hands and fix this global debt mess, but I have my doubts. Big doubts. With valuations at the second highest level in history and bond yields near 5,000-year lows, risk is high. The asymmetric risk is to the downside.

My two cents: Diversify to trend following based trading strategies, make sure they have the ability to raise cash, consider managed futures based mutual funds, tactically trade your fixed income and hedge the equity exposure you plan on holding for years to come.

Optimism, fear, optimism, fear. Don’t bite on the fear and be aware and watch out for excessive optimism. Remember that investing is a game of opposites. We all survived the 2008 crisis, but many investors got run over. And it took years just to get back to even. We will all survive the next one, but I suspect it will be equally painful, financially, if you’re not properly positioned when the recession hits.

A unique challenge this time is that 75 percent of the money in the self-directed hands of pre-retirees and retirees by the year 2020, that’s a big number and this age demographic, which includes me, just doesn’t have the time to overcome the next -50% for stocks and -10% to -30% or more for bond funds (should rates and default levels rise). Much of that money that’s been herding into passive buy-and-hold will likely herd back out, if past crisis history is any guide, at the wrong time. But don’t see fear. See opportunity. Stay patient and prepared.

Grab a coffee. I hope you find this week’s post helpful. The last two OMR’s have talked about the long-term debt. I believe it is the significant headwind we face. As CMG’s Brian Schreiner said to me this week, “The math doesn’t allow for a soft landing.” Read on and please let me know what you think.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Included in this week’s On My Radar:

- The Math Doesn’t Allow for a Soft Landing

- Three Charts of Interest

- Trade Signals – Little Movement in Equity Market, Equity Trend Remains Bullish, Sentiment Favorable (10-26-2016)

The Math Doesn’t Allow for a Soft Landing

My colleague Brian Schreiner reminded me of the testimony Laurence Kotlikoff, Professor of Economics at Boston University, gave to the Senate Budget Committee in early 2015. You’ll find the link below. Brian’s comment to me is that the math doesn’t allow for a soft landing. I continue to believe it will take a crisis to get the political engine moving and even then… will they act for themselves or set their compass to do right. Doing right involves some short-term pain – that won’t square with their desire to be re-elected.

Here is a cut-to-the-chase summary (you’ll find the full link below and I recommend you read it).

Kotlikoff starts: Let me get right to the point. Our country is broke. It’s not broke in 75 years or 50 years or 25 years or 10 years. It’s broke today. Indeed, it may well be in worse fiscal shape than any developed country, including Greece.

This declaration of national insolvency will, no doubt, shock those of you who use the officially reported federal debt as the measuring stick for what our country owes. After all, federal debt in the hands of the public is only 74 percent of the GDP. Yes, this is double the debt-to-GDP ratio recorded a decade ago. But it’s still a far cry from Italy’s 135 debt-to-GDP ratio or Greece’s 175 percent ratio.

Unfortunately, the federal debt is not an economic measure of anything, including our nation’s fiscal position. Instead, the federal debt and its annual change, the deficit, are purely linguistic constructs that reflect how you members of Congress choose to label government receipts and payments.

A few highlights:

- What economics tells us is that we can’t choose what to put on the books. All government obligations and all government receipts, no matter what they are called, need to be properly valued in the present taking into account their likelihood of payment by and to the government.

- Congress’ economically arbitrary decisions as to what to put on and what to keep off the books have not been innocent.

- Spending six decades raising or extending transfer payments and cutting or limiting taxes helped members of Congress get re-elected. But it has placed our children and grandchildren under a fiscal Sword of Damocles that gravely endangers their economic futures.

Kotlikoff then goes on to put all Federal obligations on the books:

- The U.S. fiscal gap currently stands at $210 trillion. This figure is my own calculation based on the Congressional Budget Office’s July 2014 75-year Alternative Fiscal Scenario (AFS) projection.

- Constructing the infinite-horizon fiscal gap from the CBO’s AFS projection takes less than five minutes.

The U.S. Fiscal Gap

- The size of the U.S. fiscal gap — $210 trillion — is massive. It’s 16 times larger than official U.S. debt, which indicates precisely how useless official debt is for understanding our nation’s true fiscal position.

- U.S. GDP currently stands at $18 trillion. Hence, the fiscal gap represents almost 12 years of GDP.

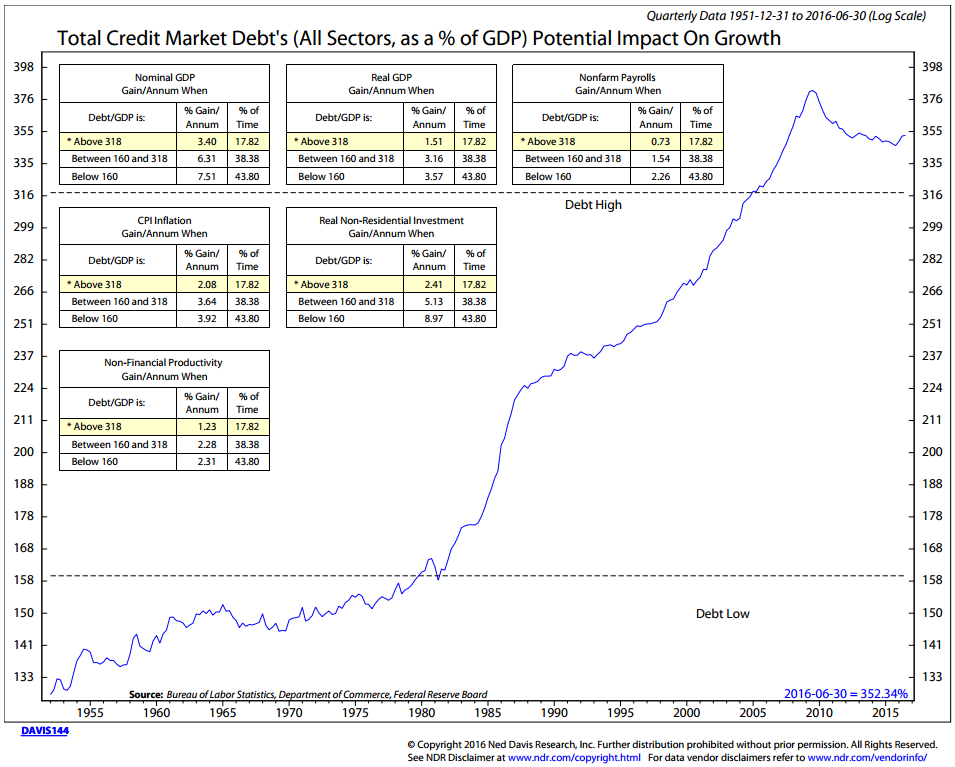

I recently showed that Total Credit Market Debts in the U.S. to be 352.34% of GDP. Total debt to growth. Here is another look at that chart:

Source: Ned Davis Research

Kotlikoff is basically saying that the situation is far worse. We must consider other debts we promised to pay like social security and Medicare. No one in Congress wants to touch this issue.

So it looks something like this:

The total debts are $210 trillion and not the $18 trillion or so in outstanding government bonds. They are not counting all the debt for which we are truly on the hook.

So take GDP (our nation’s growth) of roughly $18 trillion and divide that into $210 trillion in debt and you get a debt-to-GDP ratio of 1166%.

You get the picture. Debt remains our most significant economic challenge. We may indeed be at the end of a long-term debt cycle.

We need to save more, default, restructure the debt or a combination of all three. We’ll get out of this mess one way or another and I believe Brian may be right, “The math doesn’t allow for a soft landing.”

Click here for Professor Kotlikoff’s testimony “America’s Fiscal Insolvency and Its Generational Consequences,” Senate Budget Committee (February 25, 2015).

Charts of Interest

A few charts I came across this week that I found interesting:

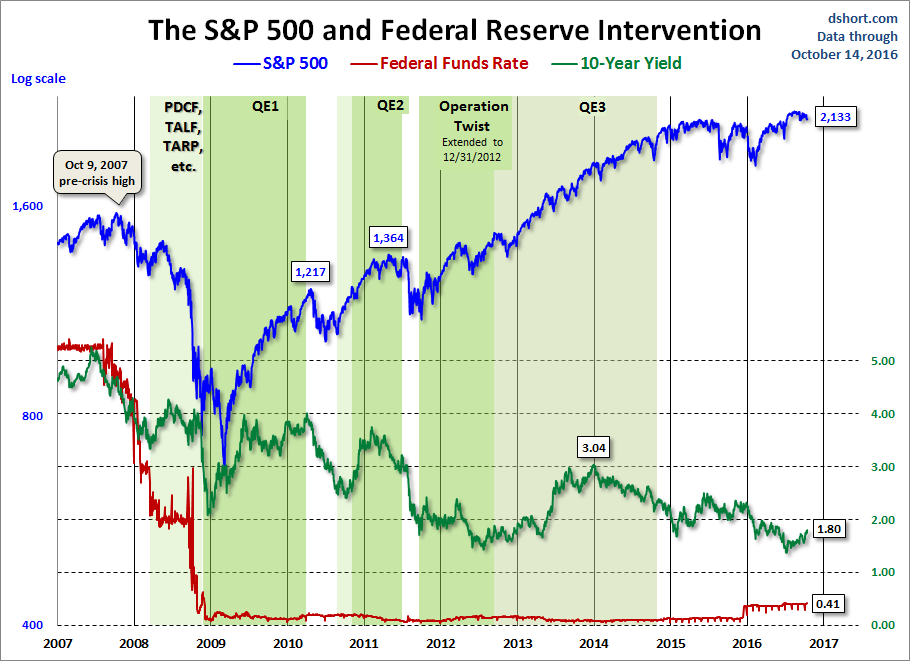

Chart 1: QE impact on the market. Note the challenges in the non-QE periods. It’s “All about that Fed.”

Source: dshort.com

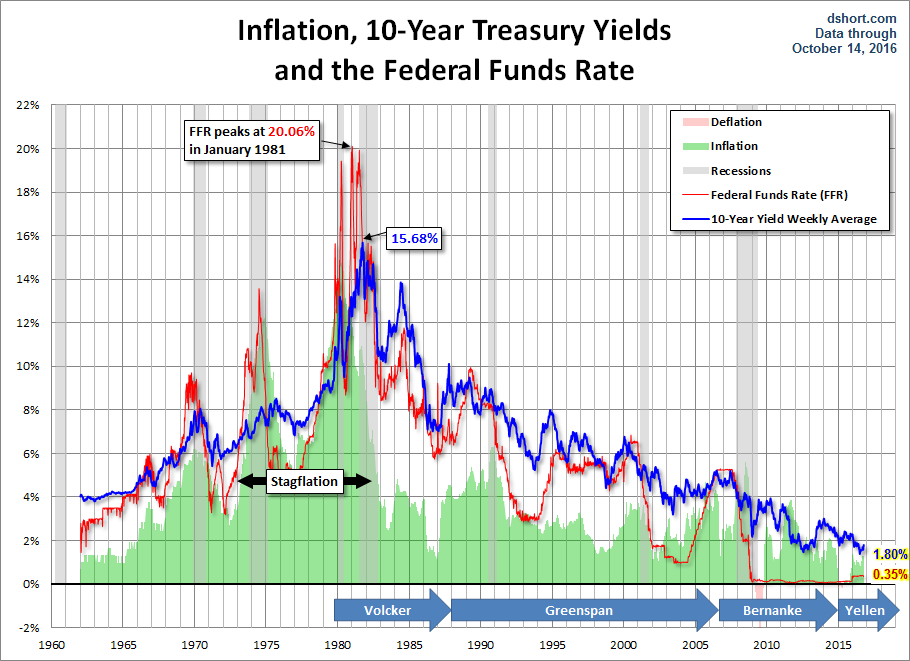

Chart 2: A Long-Term Perspective on Inflation and 10-Year Treasury Yields

Source: dshort.com

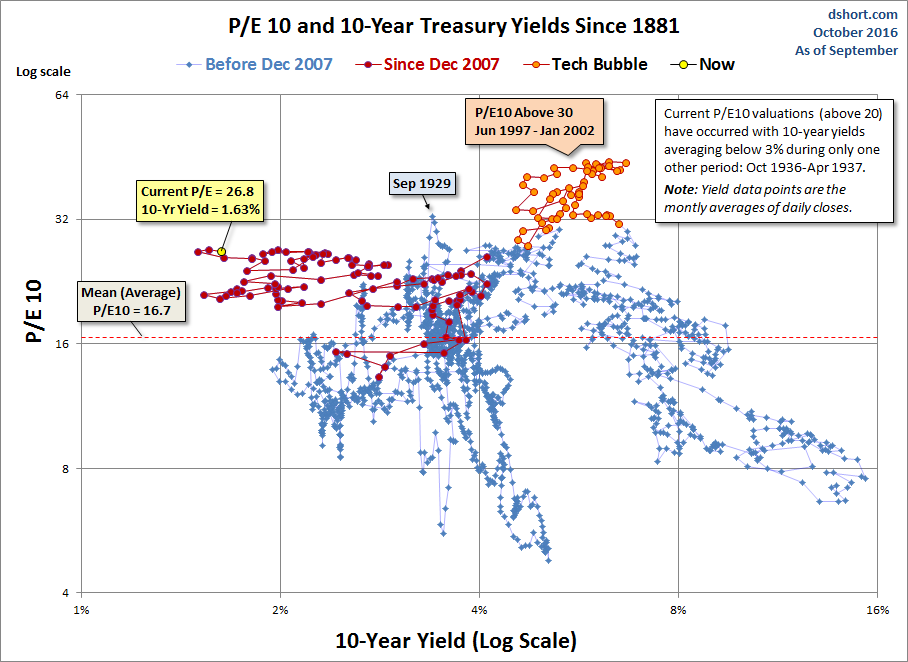

Chart 3: Uncharted Territory – Never in history have we had 20+ P/E10 ratios with yields below 2.5%

Source: dshort.com

Trade Signals – Little Movement in Equity Market, Equity Trend Remains Bullish, Sentiment Favorable and You’ll Find an Interesting Chart on QE’s Impact on the S&P 500 (10-26-2016)

S&P 500 Index — 2,143 (10-26-16)

Posted each Wednesday, Trade Signals looks at several of my favorite stock, investor sentiment and bond market indicators. It is my weekly risk management dashboard, designed to keep me better in sync with the major technical trends. I hope you find the information helpful in your work.

Click here for the most recent Trade Signals blog.

Personal Note

“If someone tells you they know how this is going to play out, take the information in with a high degree of skepticism.

We can know if player “A” does this, then “X” is likely to happen and if player “B” does that,

then “Y” is a probable outcome, but we just don’t know who is going to do what and when.”

— Steve Blumenthal

Send me an email if you’d like to learn more about how trend following works. I’ll send you an education piece I wrote on the subject. You’ll find that there are hundreds of academic studies and a number of money managers, such as CMG, with years of trading experience. I believe it is the right approach for the time in which we find ourselves today.

No major plans on the schedule this weekend. The weather looks good and fall is nearing its peak here in the Northeast. I’m going to see if I can get my boys to the golf course tomorrow. The trees are in full color.

There are no major travel plans on the schedule for November as of now. I see a quick business trip to Florida and I have Denver on the schedule on December 8. As I close today, I want to send a special hat tip out to Coach Bahr. I know his health is challenging for him right now and Coach, please know I think about you, I’m grateful for what you taught me and I’m wishing you well.

Here is a special wish to those most important to you and your life. Have a great weekend!

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts via Twitter that I feel may be worth your time. You can follow me @SBlumenthalCMG.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Wishing you and your family the very best!

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

[/drizzle]