“The most rewarding things you do in life are often the ones that look like they cannot be done.”

“I’ve always made a total effort, even when the odds seemed entirely against me.

I never quit trying; I never felt that I didn’t have a chance to win.”

— Arnold Palmer

Arnold Palmer! Well done our wonderful friend, well done. And welcome home!

[drizzle]

Some years ago, Susan and I were watching Arnie’s final Masters. She gasped, “Oh my God, what was that?” She looked at me and asked, “Is that really his swing?” (If you’ve never seen his swing, it’s fair to say “unorthodox” comes to mind.)

His style was not subtle. His father, a professional greenskeeper at Latrobe who had set him up with a cut-down three-iron when he was four, told him to hit the ball hard, and he obeyed. Even his putts, delivered pigeon-toed and slightly knock-kneed, packed a punch. To play any other way, he said, would be to deny his feelings.

“Go for broke” was his motto, and his speciality was the “Palmer charge,” where he would roar in from behind to clinch a title: most famously at the 1960 Open again, with seven birdies in the final round.

It seemed risky, and often was. Double-bogeys might be followed directly by eagles, and vice versa. It all made for great television as elation and dejection chased across his handsome face. (Between holes, in his prime in the early 1960s, a cigarette added to the glamour.) But the risk seemed less to him.

– First, he found golf pure joy, despite the exasperation; as a boy he had even played in deep snow, towards cups frozen solid on iced-over greens. Risk added sweetness.

– Second, though he didn’t relish booming shots into trees and sandtraps, he found the getting-out fun.

– And third, he never tried a shot he couldn’t make. “Powerhouse Palmer” always believed he could pull it off. And he generally did.

His heart was simple; a man for steak, beer and Westerns, a conservative and unashamed provincial who spent most of his time in Latrobe, looking out at the woods where he had practised escapes to an audience of trees. His champions’ medals were set in an old walnut table in the games room—with a few holes left ready to take the ones he felt sure he could win in future.

– Excerpts from The Economist (I wish I could write that well.)

I loved his unassuming and humble way. Arnie’s Army…then, now and forever – count me in.

“He never tried a shot he couldn’t make.”

I feel that $15 trillion in central bank liquidity has driven the ball way left and nearly out of bounds. Is there a recovery shot to be played? Can Yellen, Kuroda and/or Draghi get the ball back in the fairway? The game is being played in a debt-loaded and highly leveraged storm. I wish Arnie was standing over the ball.

Last week, I shared my views on valuations and probable forward returns. Today, let’s take a quick look at two charts that I found that may be helpful in explaining to your clients the returns we might expect over the coming 10 years. You’ll also see the same data presented that tells us we have less of an idea as to what returns might be over the coming three years. I think this information may help us decide the type of shot we need to play.

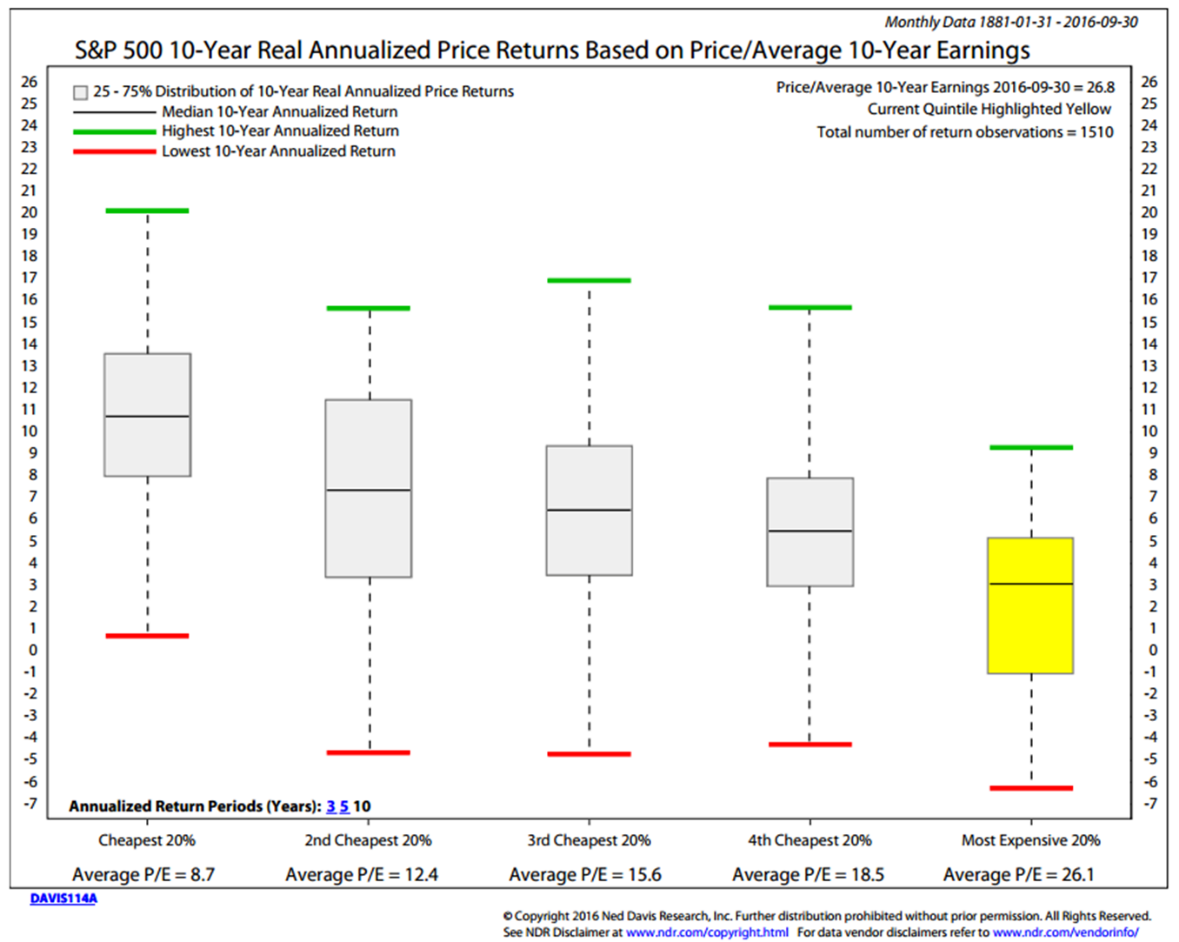

What do historical valuations and returns look like statistically? Ned Davis Research (NDR) analyzed monthly 10-year earnings data going back more than 100 years. They looked at each month-end earnings data point and calculated the actual subsequent 10-year annualized return.

For example, what was the earnings data at the month ending January 1976? Then, what was the annualized return over following 10 years ending December 1985? What was the earnings data in February 1976 and the annualized return through January 1986? Every month, 10 years later, plot return, step forward a month, plot return, etc.

NDR then grouped the returns into five quintiles. Cheapest to most expensive. Below is what the 10-year data looks like. The dark line in the middle of each box is the median 10-year annualized return. That’s a lot of data and the outcome is telling. The green line shows the single best 10-year return in each quintile and the red line the single worst. (For each quintile, the green line represents the best outcome in more than 1,600 data points. So think about that when you’re placing your bet. The red line is the single worst 10-year outcome by quintile.)

The yellow highlighted box, “Most Expensive” quintile, is where we find ourselves today. The black line in that box tells us odds favor a 3% annualized return outcome over the coming 10 years (before inflation). Statistically, that may be the most probable return outcome, but you could get 9% (doubt it) and you could get -6% (doubt that also). Remember the returns are annualized returns, so -6% per year for 10 years is a loss of more than 50% on top of 10 years of lost return opportunity.

Source: NDR

As Warren Buffett said, “We in the Buffett household like hamburgers, and when the prices go down we sing the Hallelujah chorus [we get much more for our money], when they go up, we weep.” He doesn’t understand why investors don’t think about the markets in the same way. The 10-year data is a pretty good proof statement.

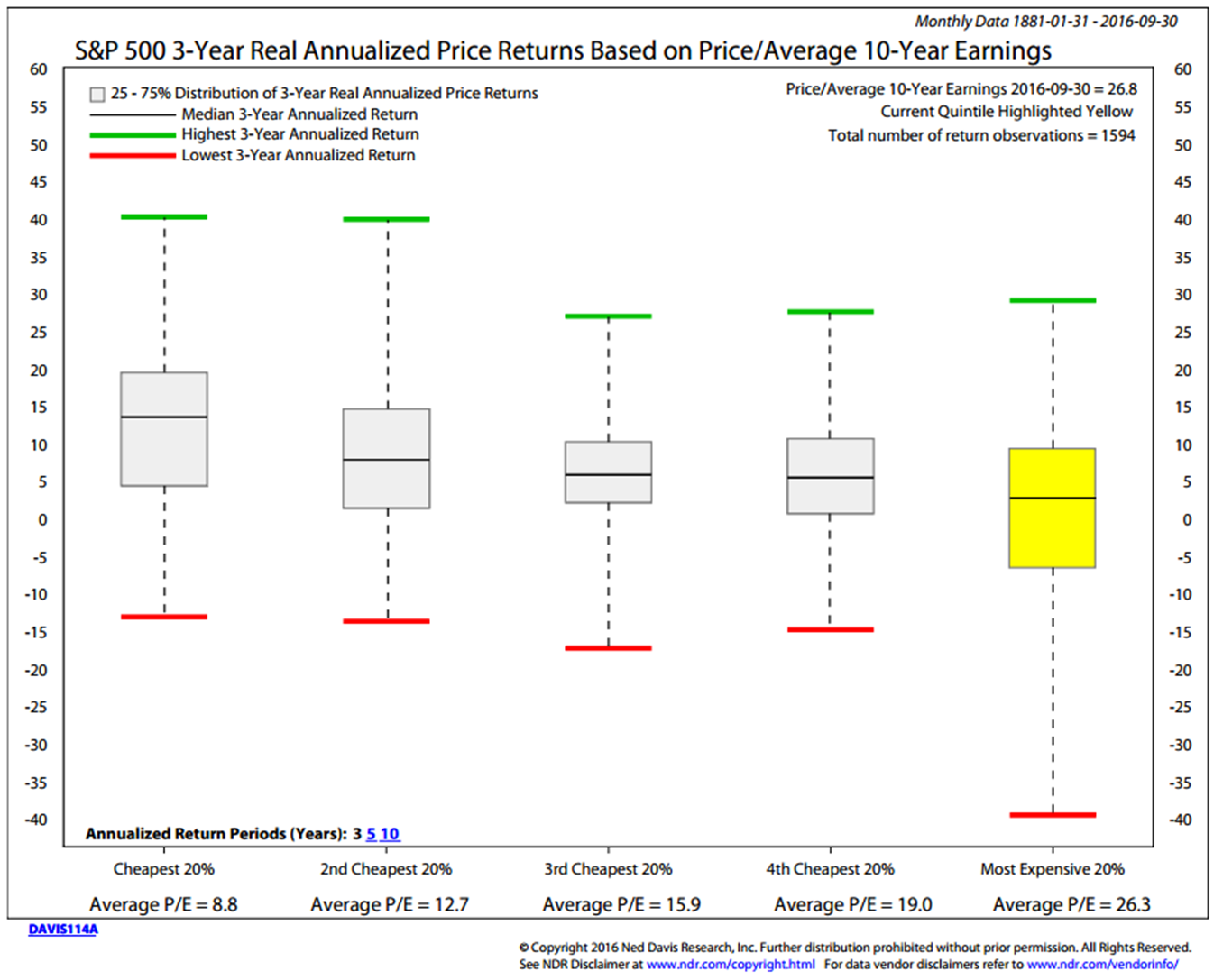

The easy part is measuring market valuations. The problem is they may stay elevated for extended periods of time. What about the next three years?

The next chart looks at the data the same historical valuation data but then plots and quintiles the subsequent returns over three years. What this is telling us is that valuations are not as good a predictor of three-year returns as they are of 10-year returns.

Source: NDR

The median returns for quintiles 2, 3, 4 and 5 are fairly bunched together in the 4% to 8% range (dark line in the center of the shaded boxes), but there still exists a much tougher shot to be played when we find your ball sitting in quintile five. The clear winner is quintile one, the “Cheapest.”

You might be wondering about five-year data. The median annualized return drops to 0% for the quintile we find ourselves in today (“Most Expensive”). Keep in mind that GMO’s most recent seven-year return forecast is calling for a -3.2% annualized real return for large cap equities (real means nominal return less inflation). Show this to your clients and before you do, know that, in general, the average investor is expecting 10%.

Investors are looking to score a 10% return over the coming years on equities. The data says 0% over five years, and maybe 3-4% annualized over 10 (before inflation). The hamburgers are expensive.

What is crystal clear from the data is that valuations matter and are good predictors of probable forward returns. Low valuations equate to higher returns. High valuations equal lower returns (and higher risk). The armature is looking to hook the ball through a forest of trees. Not sure even Arnie could pull off that shot.

Click here for last week’s post for more on the most recent market valuations if you missed it. Also, if you are not a subscriber to NDR’s independent research service, I suggest you should be. (I’m paid nothing for that endorsement… just a happy customer and long-time fan of their work.) And read Ned’s book, Being Right or Making Money. It’s awesome.

Today, forget the coffee and go mix an iced tea with lemonade. Then find your favorite chair. I share a few thoughts about the global debt mess and a few ideas on how you can use trend following trading strategies to provide a solid core within your portfolios. As your friend and caddie, that’s the shot I’m recommending you play today. In the concluding section below, you’ll find a link to a really fun 15-second ESPN video of Arnold making an “Arnold Palmer.”

Included in this week’s On My Radar:

- Debt — Here, There and Everywhere

- Trend Following Works — What You Can Do Today

- Trade Signals – Trend Remains Positive for Equities & HY; Negative for High Quality Bonds (10-12-2016)

Debt — Here, There and Everywhere

What troubles me most is the amount of debt and leverage that exists here, there and everywhere… a massive overabundance of debt.

Wikipedia defines it this way: “Debt crisis is the general term for a proliferation of massive public debt relative to tax revenues, especially in reference to Latin American countries during the 1980s, and the United States and the European Union since the mid-2000s. As well as the Chinese debt crises of 2015.” Do you remember the Asian crisis (Thailand, South Korea and Indonesia) that was ignited by the Russian debt default in 1998? That one brought down Long-Term Capital Management.

Today, we are not looking at just a few select pockets of extreme. Debt is extreme everywhere. Latest figures have global debt north of $200 trillion. That is about three times the global economy. We know from past studies that countries start to get into trouble when debt is at 90% of a country’s gross domestic product (“GDP”). 300% is a real problem.

I came across this next chart from Ned Davis Research this week. It looks at Total U.S. Credit Market Debts and compares it as a percentage of GDP. Note the yellow highlighted areas. Simply, when debt is high, growth is least.

Source: NDR

Debt is the global drag on growth. OK, the point is clear. High debt equals slow growth.

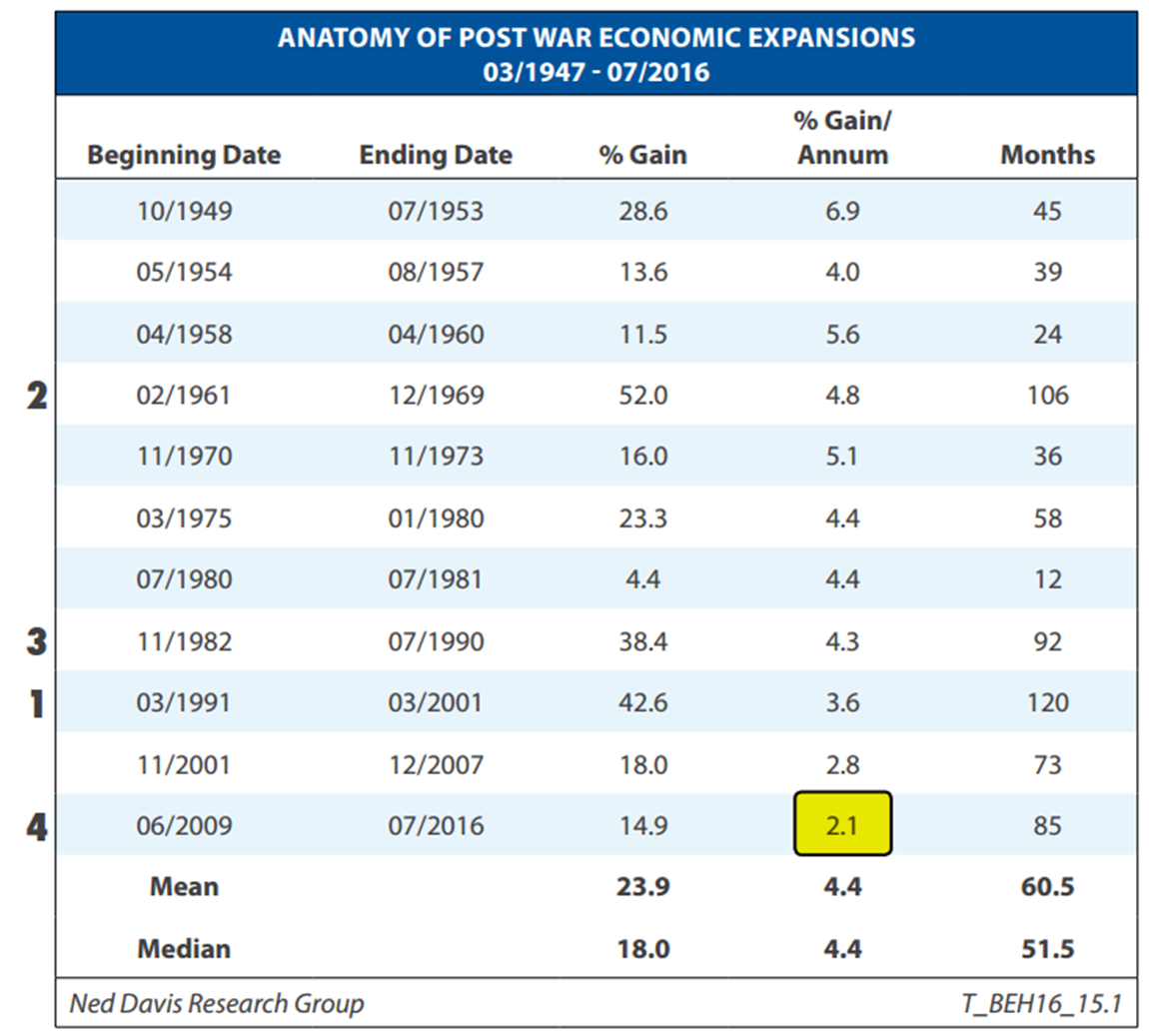

Note the 2.1% highlighted annual economic growth. More recent GDP figures are coming in at 1.5%. The numbers you see on the left rank the four longest periods of economic expansion as measured by month. At 85 months, the current expansion is the fourth longest since 1949. Note too that 2.1% is the lowest of all expansions.

This from the Atlanta Fed:

We are facing the mother of all structural issues. Debt! And the global central bankers know it. Thus, the warnings from the BIS, IMF and others. But your client may not know it and given the demographics of our aging population, the next 40% decline (or greater) will mean “no retirement for you.”

Debt, when initially taken on, is good for growth. It is a steroid shot in the arm to the economy, but it comes at the expense of future consumption and investment. And with more money owed to be paid back in the future, there is less money to spend (future demand decreases). This is the structural issue we must work through today.

The point is that when debt is high and leverage is high, growth slows and there is less room for error. We are in a period in time that we must consider risk. Preservation of capital is mandatory.

In the next section I talk about what you and I can do:

Trend Following Works – What You Can Do Today

Study up on trend following. Almost every effective strategy I know can be written on the back of a napkin. The processes may appear to be “deceptively simple” and many are, yet implementation can prove to be “endlessly complicated.” Similar to Arnold’s quote below.

My experience is that the best strategies can be explained simply. The “trend is your friend,” as they say. The hard part is having the emotional fortitude and discipline to stick to your process.

Why today? 71% of the world’s government bonds are yielding less than 1%. Equity market valuations are too high. Trend following strategies can help you participate in market advance and protect against major market declines.

You can come back from -10% to -20% relatively quickly; however, it takes years to recover from -50%. Click here for an educational piece I wrote called The Merciless Math of Loss. The most important investing lesson is to understand how compound interest works.

Here are a few good tips on Trend Following:

- It’s important to have a plan, remain disciplined in executing that plan and pay attention to what is actually happening rather than what you expect to happen.

- Investor behavior is the significant driver that creates trends. Profit seeking speculation is the driving force of all markets.

- Trend following trading is an important force in every market and should be a part of any diverse investment portfolio.

- Read Trend Following: Learn to Make Millions In Up Or Down Markets by Michael Covel. The book is the result of his 14-year journey for the truth about trend following trading. He believes, “trend following,” is the single best strategy to consistently make money in the markets.

- Trend following is based on price. Trend followers seek to capture the majority of a market trend, up or down, for profit.

- Trend following is not predictive… traders wait for the trend to shift first, then “follow” it.

I post various trend following charts each week in Trade Signals. I don’t believe you always need trend following trading strategies in your portfolio, but I do believe you need them most when valuations and risk are highest.

For more on Trend Following, see our short paper, Trend Following Works! I encourage you to do more research on this topic. You’ll find references to a number of important academic studies in the paper.

If you don’t have the time to do this on your own, diversify between a handful of trading strategies. Make sure they come at trend trading using different processes. That will aid in your diversification and should smooth the returns. Email me if you’d like to learn more.

Trade Signals – Trend Remains Positive for Equities & HY; Negative for High Quality Bonds (10-12-2016)

S&P 500 Index — 2,139 (10-12-16)

Posted each Wednesday, Trade Signals looks at several of my favorite stock, investor sentiment and bond market indicators. It is my weekly risk management dashboard, designed to keep me better in sync with the major technical trends. I hope you find the information helpful in your work.

Click here for the most recent Trade Signals blog.

Concluding Thought

“Golf is deceptively simple and endlessly complicated.”

– Arnold Palmer

So is investing.

I believe that we are heading for another significant correction. Something in the -40% to -60% range for equities and something in the -25% range for high quality fixed income. When? They come in recessions. Much depends on central bank policy, our collective confidence in central bank policy, on fiscal policy, on debt deleveraging, on debt monetization, on peace and on far too many things not mentioned.

But we do get recessions and we’ll always get recessions. What is true is that high valuations lead to large stock market declines during recessions. What is endlessly complicated is the behavioral (emotional) pull and push the investment arena creates. Investors tend to sell when they should buy and buy when they should sell.

Right now they are bubbling into high dividend payers and ultra-low yielding bonds (including junk bonds). Wrong time.

Recessions present the greatest risks to investors. But they are difficult to forecast and difficult to identify shortly after they’ve begun. The problem for stock investors is that most of the damage to the stock market happens before the recession data is confirmed.

Trend following can help. It won’t get you out at the top nor back in at the bottom and there may be a few false trades, but it can minimize declines and preserve your principal. This is vitally important in process of growing your wealth over time. I’ve suggested some resources in today’s piece. If you don’t have the time or discipline to do it on your own, email me… we have a number of good ideas.

Personal Note

One of my all-time favorite commercials featured two ESPN commentators watching Arnold Palmer making an “Arnold Palmer.” Take 15 seconds and click that link. You too may say, “Wow, that was awesome.”

Golf has always been in my life. It was one of the great bonds I had with my father. And it taught me a lot about life. Only you know if you touched the sand with your club. A painful one stroke penalty. Dad taught me early about integrity. One of the greatest deceits of all is to deceive yourself, he said. And often times, only you will know. But you will know. He’d then ask me, “Who do you wish to be?”

Arnold Palmer is one of those types of human beings I aspire to be. He did great, he did right and he taught us all. How can’t you be in love with that man?

A big soccer weekend is ahead. The boys have multiple games and Susan’s Penn Fusion team has games both Saturday and Sunday. We talked logistics over coffee this morning with no solid solution. It’s messy… we try to hit them all.

Sunday night, our Philadelphia Union faces Orlando City for an important MLS soccer game. Being the soccer nuts that we are, we’ll be cheering — Susan and me with IPAs and peanuts in hand and the boys with Chickie’s and Pete’s crab fries — for our home team to make the playoffs. Two games to go. We need the “W.”

I’ll be in NYC on October 24th for several interviews — The Street.com, WSJ and Fox Business news. How do you say what you need to say in 90 seconds or less? My fingers are crossed. Most importantly, I will be having dinner with my beautiful daughter Brianna that evening.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts via Twitter that I feel may be worth your time. You can follow me @SBlumenthalCMG.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

[/drizzle]