Employment measures including current employment levels and those early indicators reflecting new employment creation continue to trend higher. These are not creators of economic activity, but stand as one of the better measures after economic activity has already occurred. Rising economic activity forces businesses to hire additional employees and build additional capacity to meet demand or they will miss the opportunity to take advantage to expand profits. There are no earlier measures of changes in economic activity other than Vehicle Sales, Chemical Activity Barometer and Job Opening measures. These indicators are relatively good at capturing the economic turn when coming out of recessions. Coupled with the SP500 Value Investor Index, these indicators help us to make important portfolio decisions anticipating economic recovery to capture the rise in equity markets.

In anticipation of economic peaks and equity market tops, Vehicle Sales, Retail and Food Service Sales and new employment measures flatten 12mos-18mos prior to peaks in equity markets. Markets have always been substantially over-valued at economic peaks due to optimistic market psychology. The SP500 Value Investor Index only helps investors to identify ‘fair valuation’ but does not indicate how high a market can become over-valued. The extent of market optimism is impossible to predict. It is one thing to measure value, but measuring levels and predicting changes in market psychology is not something with which we have ever been successful. The single most useful economic measure we have for predicting when economic activity is about to slow is the ‘Credit Spread’. It is when credit spreads narrow to 0.0% that lending slows considerably and economic activity shifts to correction. When lending slows rapidly, economic momentum of the past few years is suddenly perceived as having been in excess. Many businesses trying to reverse their own excess investment causes an economic correction. This occurs because business spending carries the inherent anticipation that the economic environment is likely to continue ~5yrs. (Business loans are typically 5yr obligations.) Credit spreads today, the difference between T-Bill and 10yr Treasury rates is a little over 1.25%. While not overly robust, lending continues as does economic activity.

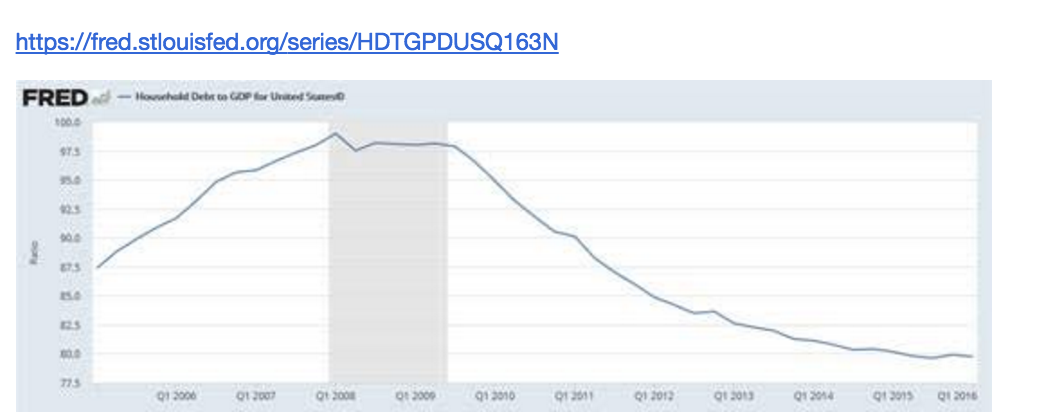

The Credit Spread is the difference between the cost of funds available to lenders and what they receive when they lend those funds to borrowers. Lenders are intermediaries. They source capital from those willing to lend it short-term (3mos-24mos) at low rates and lend it out at longer maturities (5yrs-25yrs) at higher rates. The spread has been often 3% or 300 basis points. Lenders capture the difference in rates as revenue which is how they generate profits. Lenders also accept the risks of potential losses that changing economics may force borrowers to default at some future date. Regulators dictate lenders must build reserves in anticipation of future defaults and set the level of fractional lending which is permitted. One of the features of the Sub-Prime crisis was that regulators became overly sanguine concerning underwriting standards and permitted lenders to carry as low as 2% capital to offset potential defaults, i.e. 50:1 lending leverage. This left lenders with little ability to absorb poor lending decisions. Today’s slower lending market is in part due to tighter regulations with 10%-11% reserve requirements and higher underwriting standards. Another feature of today’s credit markets has been Fed Reserve QE actions. The Fed has forced mtg rates lower in the mistaken belief that this would spur home buying activity. The opposite has occurred. Forcing longer-term rates lower has resulted in narrower credit spreads which combined with higher underwriting standards and much higher reserve requirements, has kept mtg lending to less than ½ that deemed normal. Single-Family home activity remains at 1991 levels while the US population has expanded ~30%. As a result, we have had very favorable down-trend in Household Debt to GDP. Recent recession predictions due to financial risks in our system and excess spending from high-profile investors have no supporting data.

In spite of lower credit spreads and subdued housing activity, the US and Global economic activity has continued to expand. Today’s employment report indicate that our rising trend since 2009 remains intact. The Household Survey reported that there were 420,000 additions to employment rolls occurred in July 2016 which includes those who are self-employed. No other employment measure includes the self-employed. This data is collected statistically as are all economic measures but is not revised monthly as many are. Vehicle Sales and Household Survey (Employment) continue to reflect a continuation of economic expansion

The early employment creation indicators continue to remain at record levels with the April 2016 Bureau of Labor Job Openings measure being revised to its highest level reported of 5,845,000. (Revisions are often ignored by market commentators, but important in understanding the trends)

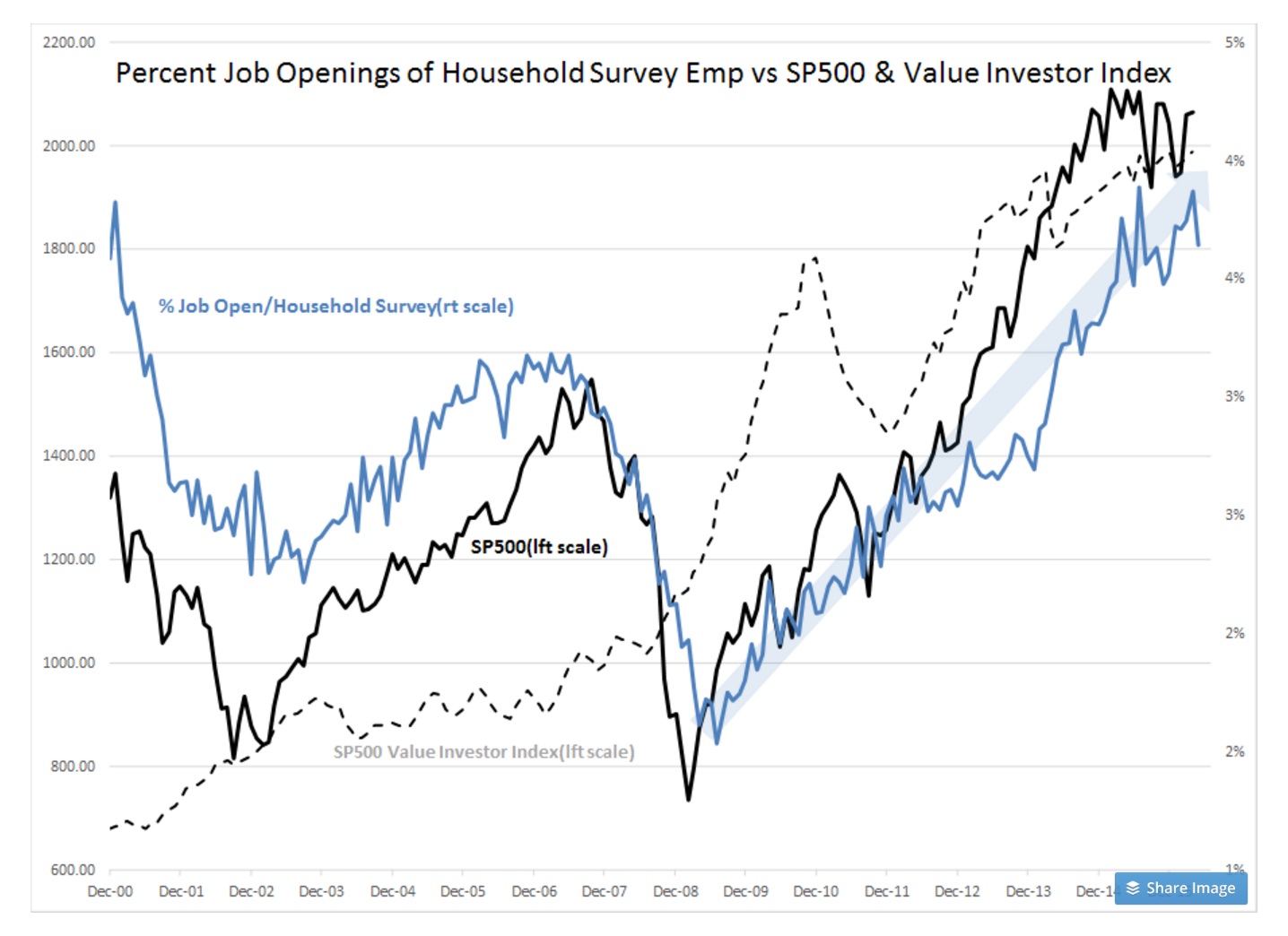

Bringing together valuation, employment and the SP500 in a single chart provides a consolidated view of how the various economic fundamentals fit with market pricing. Market pricing is not a fundamental measure of anything. Market pricing is only a reflection of what investors believe. Investor consensus as reflected in the most repeated market commentary is simply off the mark regarding economic fundamentals. There is a much less vocal minority of Value Investors which cause markets to track fundamentals.

In Percent Job Openings of Household Survey Emp vs SP500 & Value Investor Index, theSP500 Value Investor Index is represented by the Dashed Black Line, the SP500 is represented by the Black Line and an indicator created by calculating the Percentage of Job Openings of Household Survey Emp is represented by the Blue Line. Employment indicators tend to lag coming out of recession but they provide early warning to economic peaks. The SP500 reflects investor responses to perceived economic changes with Value Investors buying at market lows and Momentum Investors driving market prices to extreme levels even after economic activity has begun to slow.

The SP500 pause of the past 2yrs has no justification in fundamentals. The many calls for recession have no fundamental support. Today’s credit spreads reflect tight credit markets. Household finances reflect a low level of financial risk. The continued up-trend in employment and new employment creation continue to forecast economic expansion. The SP500 Value Investor Index reflects fair valuations historically, i.e. no general excess speculation. Add to current market psychology the impact on US$ levels since 2014, one appreciates how Momentum Investors can influence prices short-term even in the face of fundamentals which dictate far different conclusions. Free Market activity eventually causes all fundamentally divergent perspectives to normalize. There are significant investment opportunities present when investors have misread economic fundamentals. In my opinion, financial risks are low, markets remain overly pessimistic in the face of continued improvement in fundamentals.

Higher equity markets are justified by the continued improvement in fundamentals in my opinion.