By Steve Blumenthal

“We live at a time where the unthinkable has become common.”

— B. Scott Minerd, Managing Partner, Guggenheim Partners

Do you remember the story book The Little Engine That Could? The best known version of the story was written by “Watty Piper,” the pen name of Arnold Munk, who was the owner of the publishing firm Platt & Munk. Arnold Munk was born in Hungary, and as a child, moved with his family to the United States, settling in Chicago and later moving to New York. Platt & Munk’s offices were at 200 Fifth Avenue until 1957 when Arnold Munk died.

In the tale, a long train must be pulled over a high mountain. Larger engines, asked to pull the train, for various reasons refused. A request is sent to a small engine, who agrees to try. The engine succeeds in pulling the train over the mountain while repeating its motto: “I think I can.” (Source)

My favorite part was when the small engine neared the top of the mountain, the steepest part, while losing energy and puffing smoke kept saying, “I – think – I – can.” Digging even deeper inside, the engine succeeded and crossed the top. As it moved down the other side of the mountain the small engine said, “I thought I could, I thought I could.”

Look, we can and we will… succeed. But the mountain of debt is steep and the engine, while not so small, is using up a lot of energy. The excessive level of debt is the most significant drag we have on growth.

This from Bloomberg this morning:

The U.S. economy grew less than previously reported last quarter on lower government outlays and a bigger depletion of inventories, capping a sluggish first-half performance propped up mainly by consumer spending.

Gross domestic product, the value of all goods and services produced, rose at a 1.1 percent annualized rate, down from an initial estimate of 1.2 percent, Commerce Department figures showed Friday in Washington. Household spending, the biggest part of the economy, was revised higher on used-car sales.

The economy’s failure to develop a sustained pickup has helped keep Federal Reserve policy makers from pulling the trigger on an interest-rate increase so far this year. Economists project a third-quarter rebound driven by household purchases and more stockpiling, and the report showed wages and salaries were revised sharply higher, indicating consumers have the wherewithal to continue spending.

Economists have consistently missed the mark. We’ll wait and see.

A client asked me how economic growth post the great financial crisis compares to other prior periods. I did some digging and found this from Ned Davis Research, “Currently in its eighth year of growth, this expansion is the fourth longest of the postwar period. Early next year it will be number three. The longest expansion was ten years, which ended in March 2001 and encompassed the technology boom.”

Here is a look at the data from 1947 to present:

Lowest and fourth longest. OK – not so great. Expansions die because of tighter Fed monetary policy (raising interest rates) or a systemic economic or financial event. My best guess on this expansion’s ultimate age is it ends with a 2017 recession, but that is really a guess. Data dependent I say. Sounds kind of weak… right? I agree.

Federal Reserve Chair Janet Yellen promised us today that the Fed has the tools to fight off recession. And Greenspan didn’t think housing was in a bubble and completely missed the subprime mess (we didn’t). So call me a skeptic! As I shared last week, “In the Realm of Economics, No Government Can Play God.” Onward we march.

Back to the data. Pay particular attention to the highlighted 2.1% annual GDP gain since the start of the last expansion in 2009. The latest GDP annualized number coming in at 1.1%. “I think I can, I think I can.” Something is structurally wrong here and that other, really large engine (our beloved elected officials), like the large engines in the story, remain unwilling to do the fiscal work.

‘I can’t; that is too much a pull for me,’ said the great engine built for hard work. Then the train asked another engine, and another, only to hear excuses and be refused. In desperation, the train asked the little switch engine to draw it up the grade and down on the other side. ‘I think I can,’ puffed the little locomotive, and put itself in front of the great heavy train. As it went on the little engine kept bravely puffing faster and faster, ‘I think I can, I think I can, I think I can.’

Yellen is not just saying, “I think I can;” I think she is saying, “I know I can.” Oh, dear God! Like Greenspan before her, I have my doubts.

Risk on remains the theme. Debt remains the mountain we must cross as the Fed and the rest of the developed world’s central bankers grit their teeth and fight like mad to summit the peak. More debt on top of debt, to me, is a short-term easy answer but not the right answer.

My two cents is that eventually some form of default cycle is a certainty. When? The next recession… When’s that? Not just yet. There are high probability indicators that may help as time moves forward. More on this in a future letter.

Today, I have a few great charts for you (Charts of the Week) and share commentary from Guggenheim’s very bright Scott Minerd. His theme is “The demand for new monetary policy strategy and greater fiscal action is growing.” Scott concludes, “We live at a time where the unthinkable has become common.” He tells us to brace for lower interest rates for a very long time.

Nominal GDP is perhaps the best indicator of what’s going on in the economy. We are experiencing the weakest recovery since 1935. I too remain in the lower-for-longer interest rate camp but ultimately I believe that supply and demand dictates price and price behavior can help us stay on the right side of interest rate trends.

So I keep the Zweig Bond Model “on my radar” (sorry). I look at it daily and post it for you each week in Trade Signals (link below). Not perfect, no guarantees, but pretty darn good. Like most of 2014 and 2015 when the majority on Wall Street was looking for higher rates, the ZBM signaled lower rates and maintains that signal today.

Ultimately, ultra-low interest yields are not good for savers, pension plans and insurance companies. Like Fed policy and their confidence pre-sub-prime, we have to question the potential unintended consequences of unconventional central bank policy and use tools available to us to risk manage the risks we investors must take.

Included in this week’s On My Radar:

- Charts of the Week

- “A New Policy Orthodoxy Is Emerging,” by B. Scott Minerd of Guggenheim Partners

- Trade Signals – Sentiment Too Bullish, S&P 500 Annualized Return Since 12/31/99 to Present just 2.41% (Wow!)

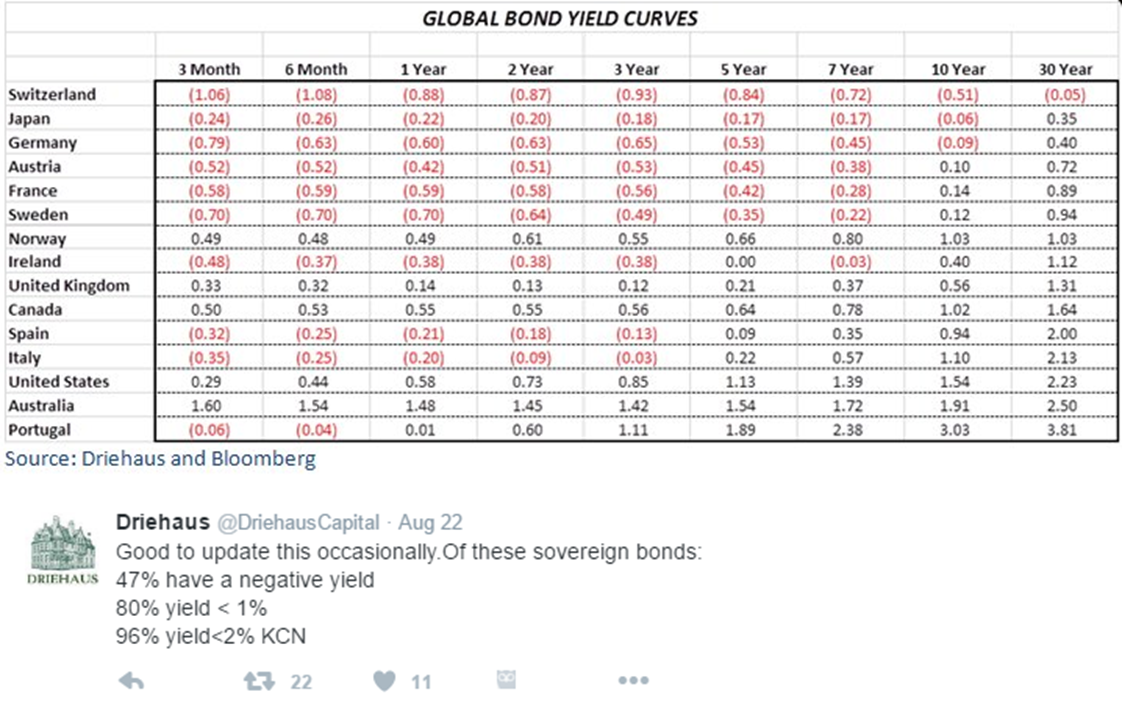

Charts of the Week

47% of global sovereign bonds yield less than 0%. 80% of global yields are under 1%. 96% are yielding less than 2%:

Federal Reserve Vice Chairman Stanley Fischer, today on CNBC, said employment will weigh heavily on the Fed’s decision as to when to raise rates. He also added, “The economy has strengthened.”

Here is a look at the Unemployment Rate:

And here is a look at the labor force participation rate – note the comparison vs. other post recovery periods:

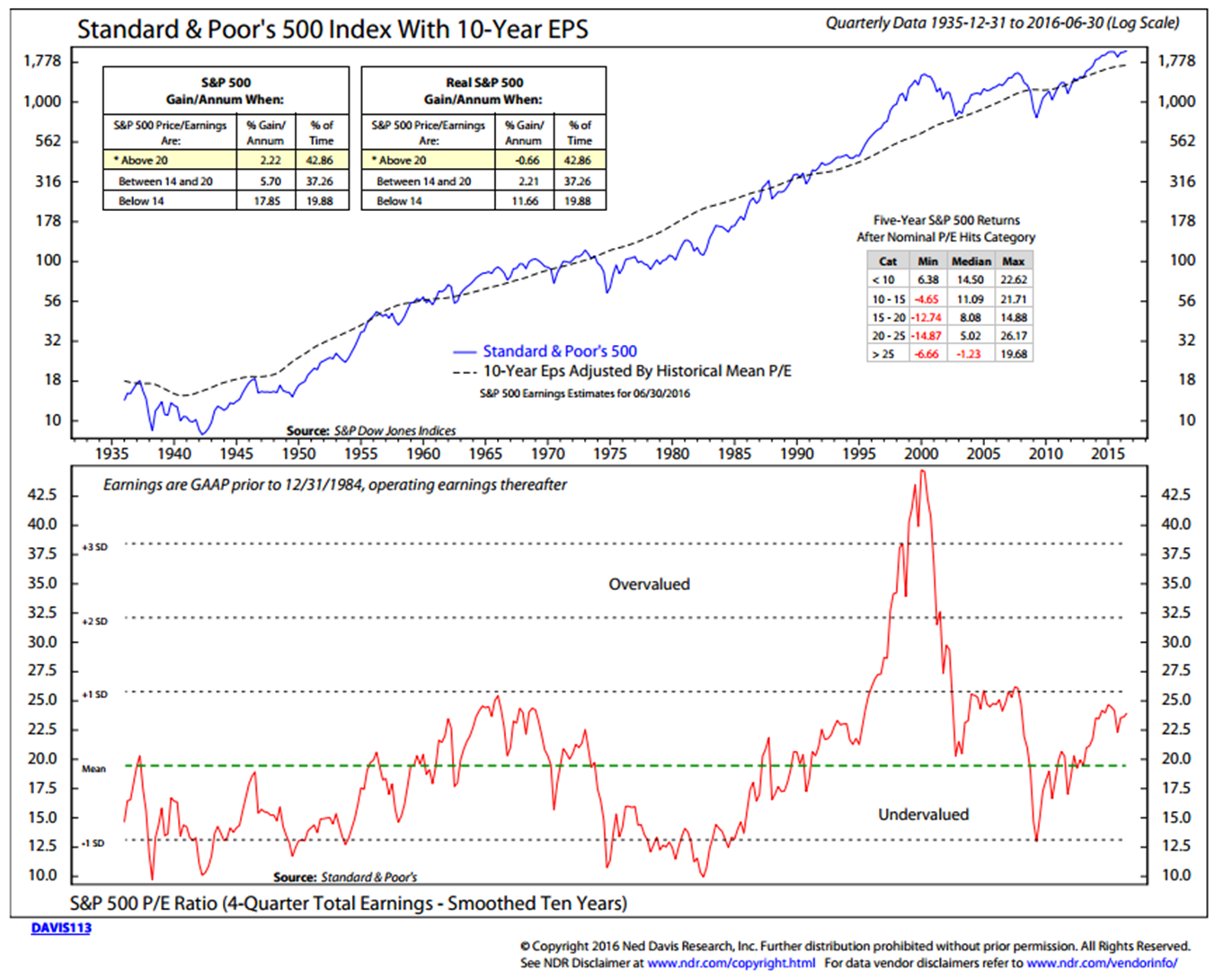

Valuations Are High and Forward Returns Probabilities Are Low:

Looking at data from 1935 to present, the next chart shows the subsequent annual nominal return in the 10-year periods following, based on median P/E. The current median P/E as of July 2016 is 24. The chart shows that when the reported number was greater than 20, the subsequent annualized return average was just 2.22% per year. After inflation (or in economic terms) the “real return” was -0.66%.

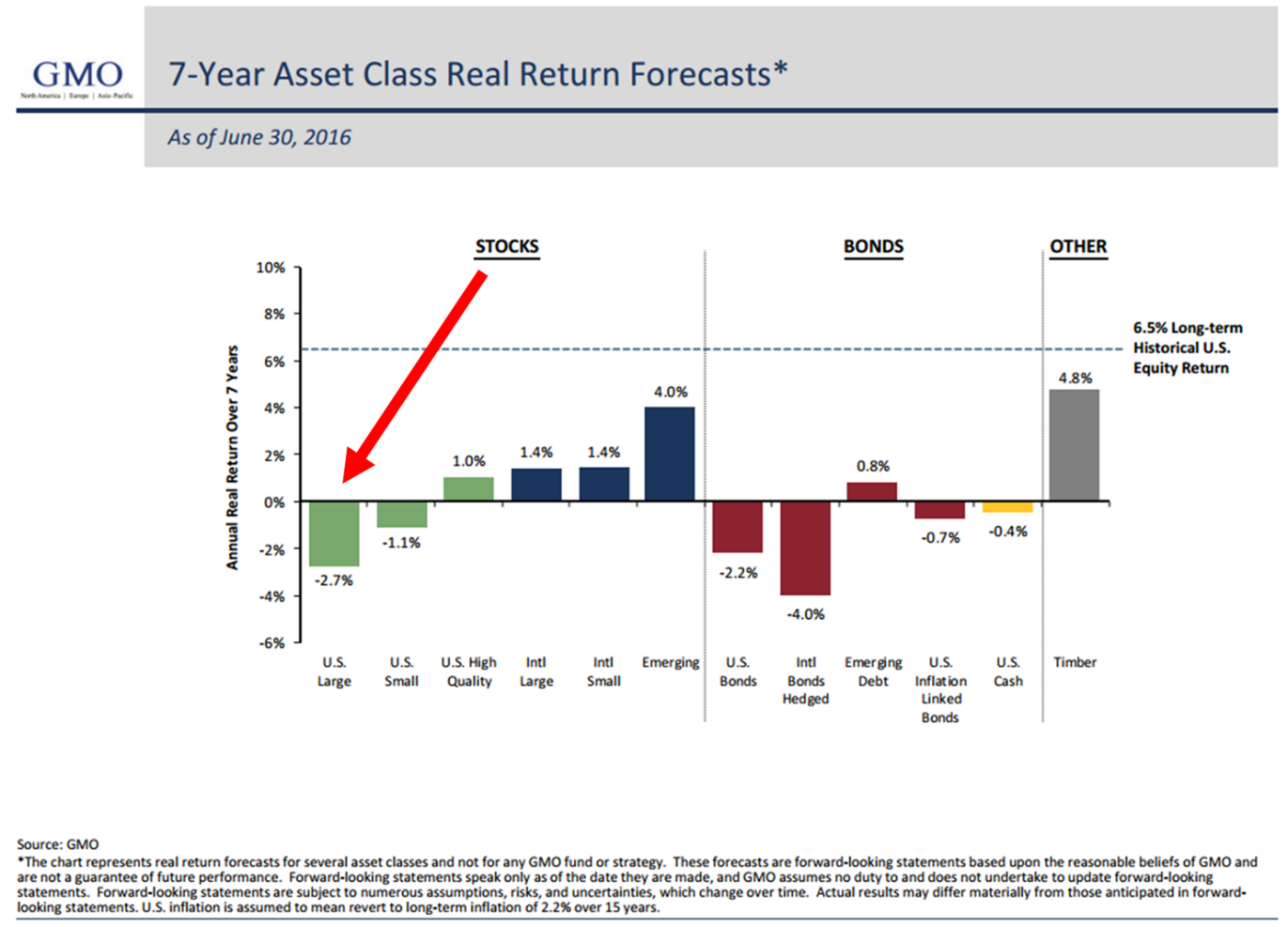

The disconnect is that individual investors, according to a recent State Street poll, are expecting 10% stock market returns over the coming five-plus years.

Further countering hopes for a 10% return is the reality of low probable seven-year forward returns – if you haven’t seen this from GMO, here you go:

Central bank balance sheets are still expanding.

A tweet from Jim Rickards expressing the Fed’s rate hike dilemma:

To that end, don’t worry because:

“A New Policy Orthodoxy Is Emerging,” by B. Scott Minerd of Guggenheim Partners

Following are a few bullet points, followed by a link to the full piece:

- The demand for new monetary policy strategy and greater fiscal action is growing.

- There is a new debate emerging among policymakers in advanced economies. Two Federal Reserve Bank chief executives have taken the position that the natural rate of interest in the United States is much lower than previously assumed.

- These experts suggest the need for a slow pace of increases in short-term rates, with one Fed president projecting only one 25 basis point increase between now and 2019, and the other suggesting negative rates are increasingly possible in the next economic downturn.

- Recently, U.K. gilts briefly joined the growing number of sovereign bonds that trade at negative yields. Investors should take note.

- Capital flows from regions of the world with slow growth and negative rates will continue to exert downward pressure on the term structure of the U.S. interest rates.

- As I have said before, it would be imprudent for investors to rule out the possibility of negative rates in the United States.

- As the world’s major economies are mired with record low bond yields, practically non-existent inflationary pressure and lackluster economic growth, policymakers cannot continue to simply do more of the same old thing hoping that even lower rates and more quantitative easing alone will reach the desired employment and inflation targets.

- After years of economic malaise in the wake of the financial crisis, the time has come to recognize that the current policy paradigm is nearing the limit of its effectiveness and perhaps already has exceeded it.

- “The critical implication of a lower natural rate of interest,” says San Francisco Fed President John Williams in a recent essay, “is that conventional monetary policy has less room to stimulate the economy during an economic downturn, owing to a lower bound on how low interest rates can go.”

- To address the problem, Williams has suggested a new orthodoxy for monetary and fiscal policy solutions. This new orthodoxy would expand unconventional monetary policy tools, including asset purchases and negative rates; create monetary policy frameworks that target either higher inflation rates or nominal GDP growth; increase long-term growth potential through targeted and scaled capital spending on infrastructure, education, and research; and make fiscal policy more countercyclical, including through changes to tax policy and federal grants to states.

- Numerous indications suggest that this new combined monetary and fiscal policy strategy may be on the horizon. In the United States, both presidential candidates are touting programs that feature significant infrastructure spending in 2017 and beyond.

- In Japan, policymakers are announcing fiscal stimulus while simultaneously flirting with the use of helicopter money.

- More broadly, a lower natural rate implies a slower baseline path of rate increases in coming years and a greater likelihood that a broader array of unconventional tools will be needed during the next recession.

- I fully expect elements of this new policy orthodoxy will be implemented, over time, here in the United States, as well as in Europe and Japan.

- The reality is that as low as rates are around the world, we now have leading regional Fed presidents updating their outlooks suggesting that the natural rate of interest is much lower than expected.

- Investors need to accept that ultralow short- and long-term rates will likely be with us through the rest of this decade and possibly beyond.

- We live at a time where the unthinkable has become common.

You can click here for the full piece.

Somebody get me a drink…

Trade Signals – Sentiment Too Bullish, S&P 500 Annualized Return Since 12/31/99 to Present just 2.41% (Wow!)

S&P 500 Index 2174

Posted each Wednesday, Trade Signals looks at several of my favorite stock, investor sentiment and bond market indicators. It is my weekly risk management dashboard, designed to keep me better in sync with the major technical trends. I hope you find the information helpful in your work.

“Because for any given level of return, if you diversify, you can generate that return with a lower risk; or for any given level of risk, if you diversify, you can generate a higher return. So it’s a free lunch. Diversification makes your portfolio better.”

— David Swensen, Chief Investment Officer

Yale University Endowment

With a nod towards broad portfolio diversification, here is a quick summary of what I am seeing — organized by investment category (equity markets, fixed income and liquid alternatives):

- Equity Markets: Investor sentiment remains extremely optimistic (short-term bearish for equities), Don’t Fight the Tape or the Fed moved recently from a +1 to 0 (now neutral on equities). The 13/34-Week EMA trend indicator remains bullish. The CMG NDR Large Cap Momentum Index is nearing a buy signal. While valuations remain extreme (overvalued), trend evidence suggests a neutral to positive view on equities (hedged).

- Fixed Income: HY remains in a buy signal or uptrend and the Zweig Bond Model remains in a buy (bullish on high quality fixed income).

- Liquid Alternatives: The CMG Opportunistic All Asset ETF Strategy is currently allocated 73% to equities and 27% to fixed income. Recent additions include technology, biotech and Emerging Market equities. For weightings by asset class, please see the pie chart below.

Several additional thoughts: Investor sentiment remains extremely optimistic (which is generally short-term bearish for equities). Due to high valuations and the aged nature of the cyclical bull market, I favor underweighting exposure to equities (hedged). I favor an endowment-like portfolio with approximately 30% exposure to equities (hedged), 30% fixed income (tactically managed) and 40% to liquid alternatives (e.g., tactical all asset, managed futures, global macro and gold).

Here is a not-so-fun fact: According to Ned Davis Research, the S&P 500 has gained just 2.41% annualized per year since December 31, 1999 (see Don’t Fight the Tape or the Fed indicator below). It has gained just 4.45% annualized per year since December 31, 1997 (see Volume Supply/Demand indicator below).

Click HERE for the most recent Trade Signals blog.

Personal Note

“Perhaps what resonates with me most is that nearly 30 years on, since the birth of the Greenspan put, so few lessons have been learned. Money is strong when grounded in investment in the future. But it is weak when built on the shaky foundation of cheap debt.”

— Danielle DiMartino Booth, former Senior Financial Analyst

Federal Reserve Bank of Dallas (Source)

Well said…

I have to say I have such fond memories of The Little Engine That Could. I believe that in our blood is the optimism that “we can.” And to the challenges we face today, we will get to the other side and say, “I knew we could.” Who didn’t root for that little engine? In the current story, that engine is you and me. Let’s win. I know we can.

For me, yesterday was a great deal of fun. I hosted a golf event at my club, Stonewall Links (suburban Philadelphia). I was joined by my friends from State Street, along with nine Wells Fargo wealth advisors. Our CMG Opportunistic All Asset Strategy is on the Wells platform and we trying our best to get the word out. A smart group of guys. Perfect weather and an overall great day.

Stonewall is hosting the U.S. Mid-Amateur on September 10-15. It will be televised on Fox Sports. Check it out – the course was designed by Tom Doak and is in outstanding shape. Of course, I’m a bit biased yet I’m told it is a “bucket list” course, so if you are a golf nut like me, let me know, and I’d be happy to take you out. Let me know if you are coming to Philadelphia.

The September travel schedule is looking a bit aggressive. I’ve yet to tell Susan and the boys. Though I am trying to make as many of their soccer games as possible. Four boys and three different high schools. It’s a logistical mess.

I’ll be speaking on portfolio construction using ETFs at the Morningstar ETF Conference on September 7-9 in Chicago. If you are going to be there, shoot me a note and let’s grab a coffee. Denver follows on September 13-15 where I’ll be attending a one-day S&P Indexing Conference and meeting with John Mauldin and team.

Late September finds me in Charlotte, NC and from there a two-day trip to Indianapolis. I’m presenting to an investor audience of 500+ on probable 60/40 forward returns and the need for a risk-managed endowment-like portfolio approach. Lou Holtz is the keynote speaker and the event is hosted by one of our advisor clients. I’m really looking forward to meeting and listening to Coach Holtz. That should be fun.

If you find the “On My Radar” weekly research letter helpful, please tell a friend … I believe the most important lesson to learn about investing is how money compounds over time. Markets move through states of undervaluation and overvaluation. Recessions are a healthy and important part of the economic cycle. At times, risk management matters more than other times. Now is one of those times. To that end, I hope you find this letter helpful.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Have an outstanding weekend. Enjoy the last week of summer! And with your favorite beverage lifted high in the air, let’s smile and toast together to the beginning of a new school year. Susan and I are smiling. Sorry kids.

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.