Lazarus Rising or Icarus Falling? The GoPro Inc (GPRO) and LinkedIn Corp (LNKD) Question!

As I watch GoPro Inc and LinkedIn, two high flying stocks of not that long ago, come back to earth my mind is drawn to two much-told stories. The first is the Greek myth about Icarus, a man who had wings of feathers and wax, but then soared so high that the sun melted his wings and he fell the earth. The other is that of Lazarus, who in the biblical story, is raised from the dead, four days after his burial. As investors, the decision that we face with GoPro Inc and LinkedIn is whether like Icarus, they soared too high and have been scorched (perhaps permanently) or like Lazarus, they will come back to life.

GoPro Inc (GPRO): Camera, Smart Phone Accessory or Social Media Company?

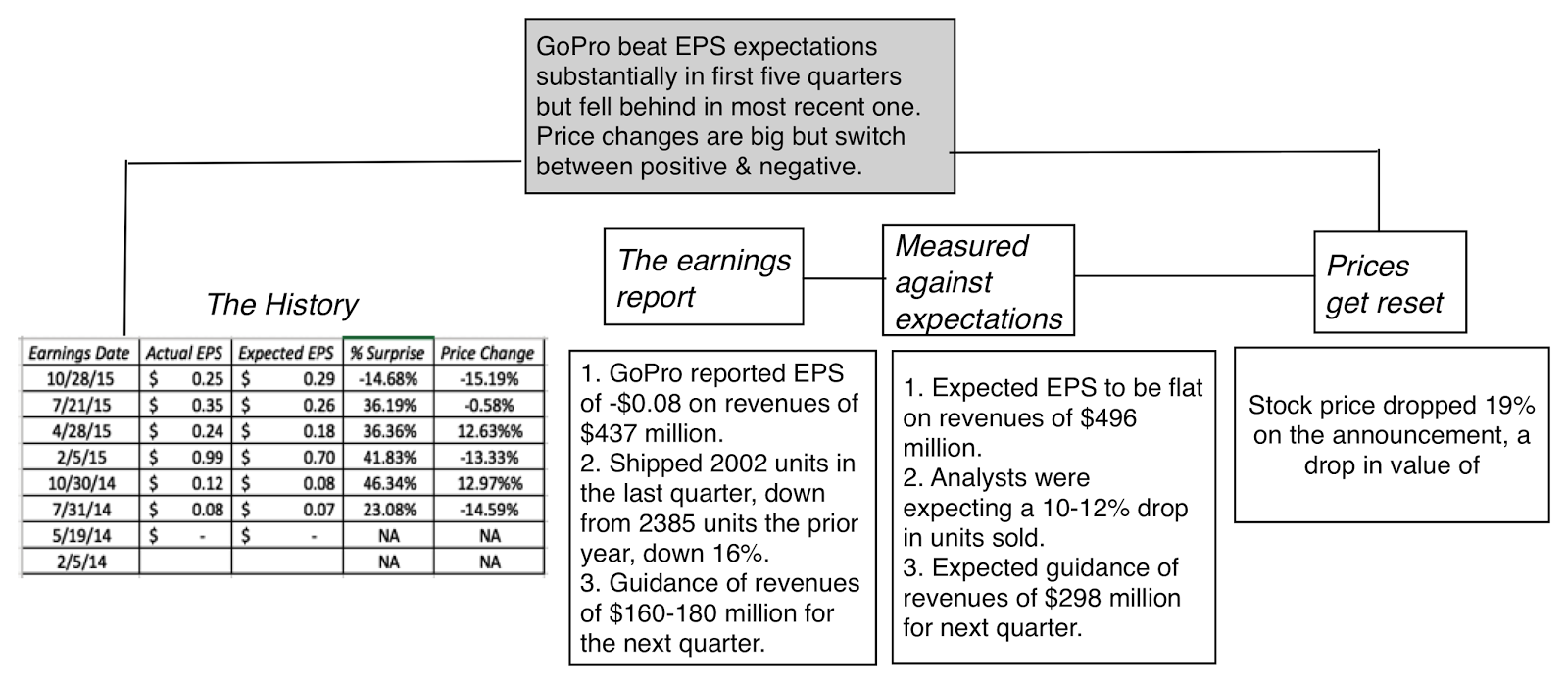

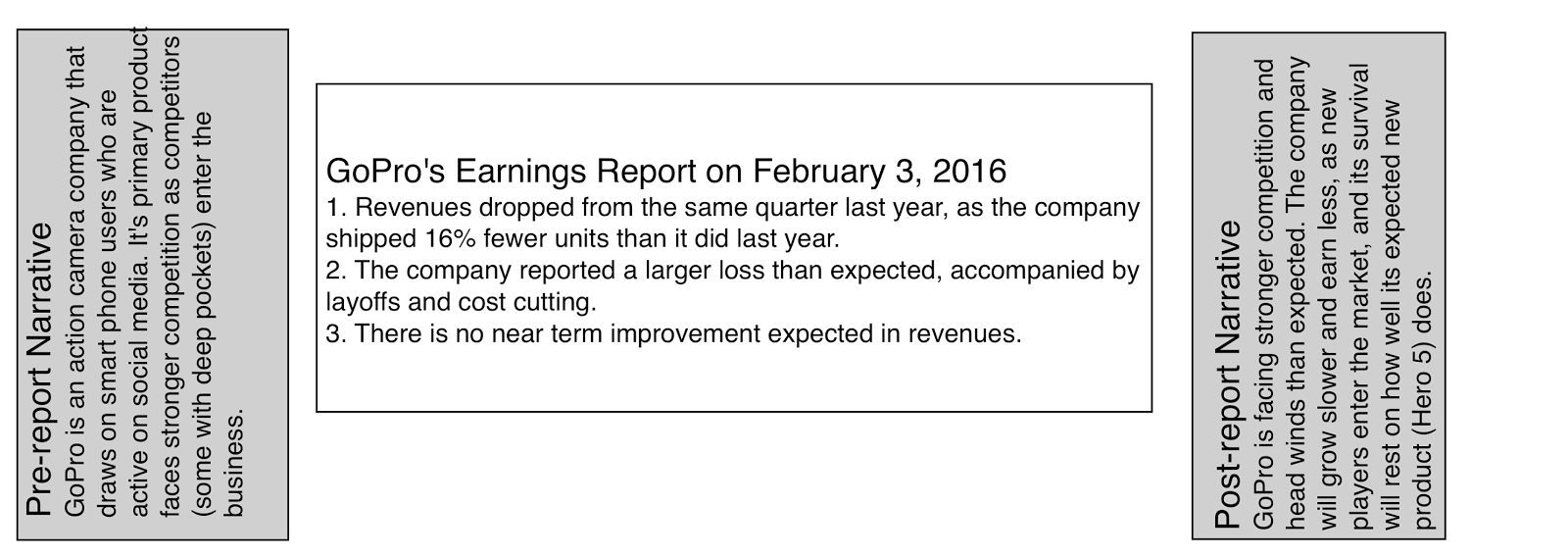

In the last year, GoPro Inc lost much of its luster as its product offerings have aged and sales growth has lagged expectations. It is a testimonial to these lowered expectations that investors were expecting revenues to drop, relative to the same quarter in the prior year, in the most recent quarterly earnings report from the company.

The company reported that it not only grew slower and shipped fewer units than expected in the most recent quarter, but also suggested that future revenues would be lower than expected. While the company’s defense was that consumers were waiting for the new GoPro 5, expected in 2016, investors were not assuaged. The stock dropped almost 20% on the news, hitting an all-time low of $9.78, right after the announcement.

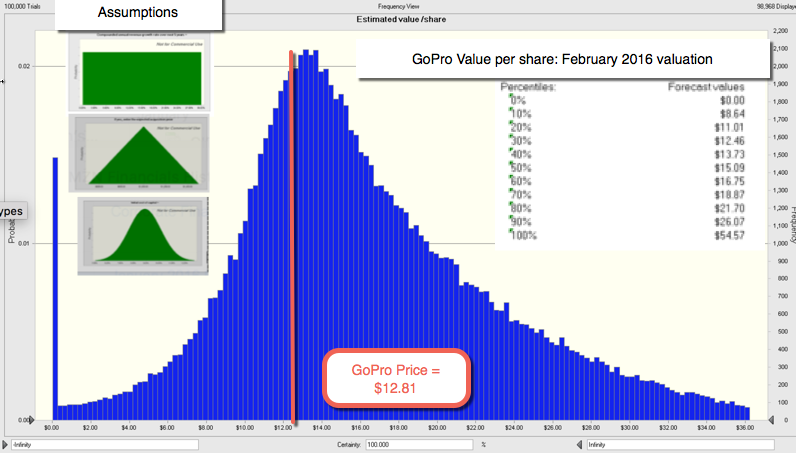

To evaluate how the disappointments of the last year have impacted value, I went back to October 2014, when I valued the stock at $30.57. Viewing it as part camera, part smart phone and part social media company (whose primary market is composed of hyper active, over sharers), I estimated that it would be able to grow its revenues 36% a year, to reach about $10 billion in steady state, while earning a pre-tax operating margin of 12.5%. Revisiting that story, with the results in the earnings reports since, it looks like competition has arrived sooner and stronger than anticipated, and that the company’s revenue growth and operating margins will both be more muted.

In my updated valuation, I reduced my targeted revenues to $4.7 billion in steady state, my target operating margin to 9.84% (the average for electronics companies) and increased the likelihood that the company will fail to 20%. The value per share that I get with my updated estimates is $17.66, 35% higher than the price per share of $12.81, at the start of trading on February 22, 2016. Looking at the simulation of values, here is what I get:

|

| Spreadsheet with valuation |

At its price of $12.81, there is a 68% chance that the stock is under valued, at least based on my assumptions.

I am fully aware of the risks embedded in this valuation. The first is that as an electronics hardware company that derives the bulk of its sales from one item, GoPro is exposed to a new product that is viewed as better by consumers, and especially so if that new product comes from a company with deep pockets and a big marketing budget; a Sony, Apple or Google would all fit the bill. The second is that the management of GoPro Inc has been pushing a narrative that is unfocused and inconsistent, a potentially fatal error for a young company. I think that the company not only has to decide whether its future lies in action cameras or in social media and act accordingly, but it also has to stop sending mixed messages on growth; the stock buyback last year was clearly not what you would expect from a company with growth options.

Linkedin: The Online Networking Alternative?

LinkedIn went public in May 2011, about a year ahead of Facebook and can thus be viewed as one of the more seasoned social media companies in the market. Like GoPro, its stock price soared after the initial public offering:

|

| LinkedIn Stock Price: IPO to Current |

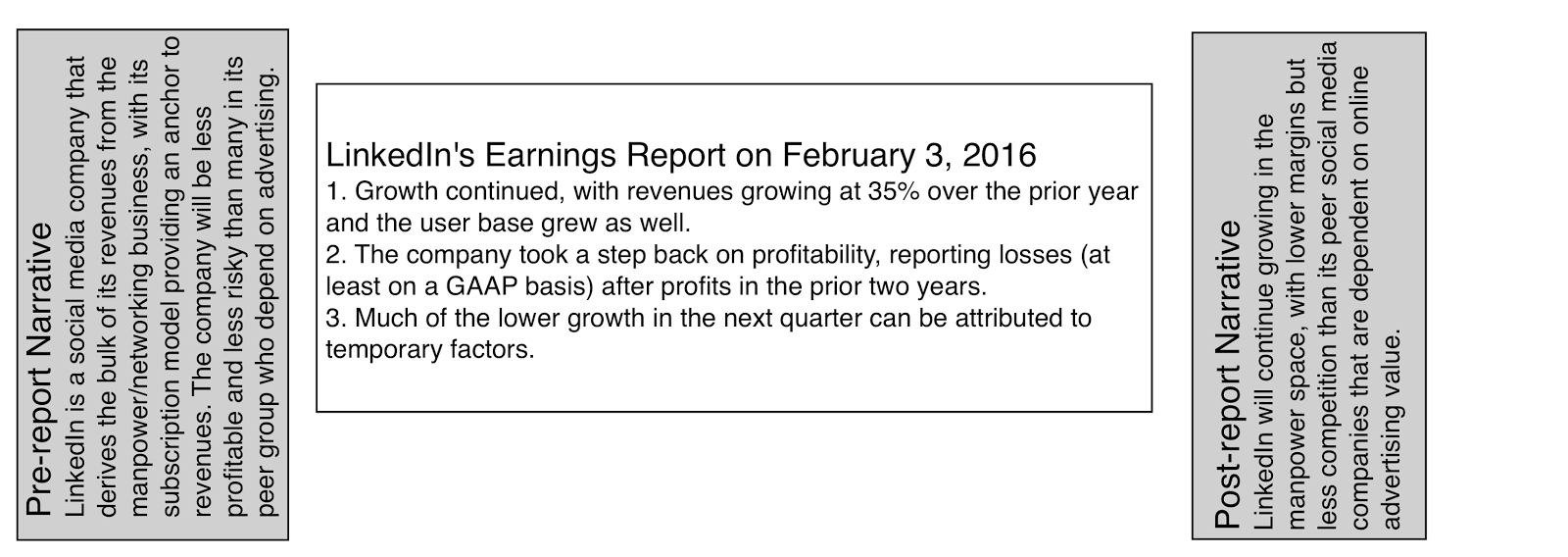

While I have not valued Linkedin explicitly on this blog for the last few years, it has been a company that has impressed me for a simple reason. Unlike many other social media companies that seemed to be focused on just collecting users, Linkedin has always seemed more aware of the need to work on two channels, delivering more users to keep markets happy and working, at the same time, on monetizing these users in the other, for the eventuality that markets will start wanting more at some point in time. Its presence in the manpower market also means that it does not have to become one more player in the crowded online advertising market, where the two biggest players (Facebook and Google) are threatening to run up their scores. Nothing in the latest earnings report would lead me to reassess this story, with the only caveat being that the drop in earnings in the most recent year suggests that profit margins in the manpower business are likely to be smaller and more volatile than in the advertising business.

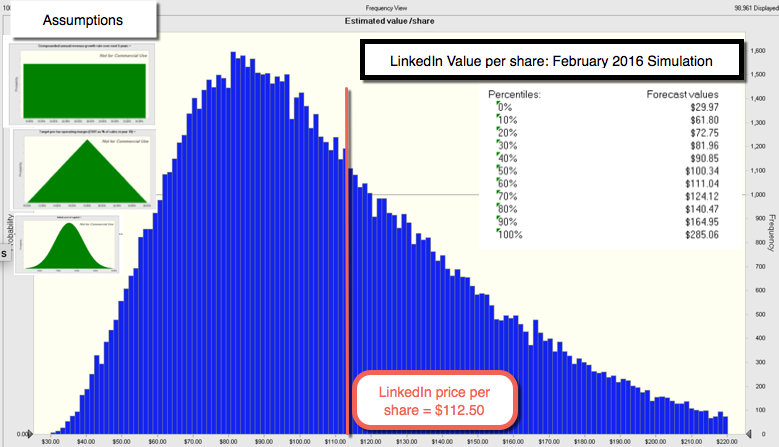

Allowing for Linkedin’s presence in two markets, I revalued the company with revenue growth of 25% a year for the next five years, leading to $15.3 billion in revenues in steady state (ten years from now), and a target pre-tax operating margin of 18%, lower than my target margins for Twitter or Facebook, reflecting the lower margins in the manpower business. The value per share that I get for the company is $103.49, about 10% below where the market is pricing the stock right now. The results of the simulation are presented below:

|

| Spreadsheet with valuation |

The Acquisition Option

Fighting my Preconceptions

- As noted earlier, unlike many other social media companies, it is not just an online advertising company.

- The other business (networking and manpower) that the company operates in is appealing both because of its size, and the nature of the competition.

- The top management of LinkedIn has struck me as more competent and less publicity-conscious that those at some other high profile social media companies. I think it is good news that I had to think a few minutes about who LinkedIn’s CEO was (Jeff Weiner) and check my answer.

- GoPro Inc – Bloomberg Summary (including 2015 numbers)

- LinkedIn – Bloomberg Summary (including 2015 numbers)

- A Violent Earnings Season: The Pricing and Value Games

- Race to the top: The Duel between Alphabet and Apple!

- The Disruptive Duo: Amazon and Netflix

- Management Matters: Facebook and Twitter

- Lazarus Rising or Icarus Falling? The GoPro Inc and LinkedIn Question!

- Investor or Trader? Finding your place in the Value/Price Game! (Later this year)

- The Perfect Investor Base? Corporation and the Value/Price Game (Later this year)

- Taming the Market? Rules, Regulations and Restrictions (Later this year)