By Steve Blumenthal

“Time to put 25% to 30% of your wealth in cash.”

– Mohammed El-Erian

“If you go to an investment adviser, they’ll tell you cash is wasted,” says El-Erian, chief economic adviser at Allianz. ‘I don’t think so.’ ‘You will have many opportunities to buy really good names at beaten down prices,’ says El-Erian, whose latest book, “The Only Game in Town,” was released this week.” Source

25% to 30% in cash? Take a step back and think about that for a second.

But what do you do when interest rates reach zero? Here is more on the cash subject from famed hedge fund manager, Ray Dalio, who founded Bridgewater Associates, the world’s largest hedge fund:

- “The discount rate is just about as compressed as it can be, so the potential value effect of lowering it is nearly at its end. That’s a big thing.

- “All else being equal, the more interest rates are pushed down, the more asset prices will be pushed up. That is how monetary policy now works.”

- “In terms of the risk premiums of ‘risky assets,’ they’re now neither especially high nor low, so there is a bit more to be squeezed out of them, more so in the US than elsewhere.”

- “Put these two pieces together and it’s clear that the future returns of assets will be low, which will be a problem given what the returns need to be to meet our future obligations.”

- “Though not pressing, that issue is something that central banks will have to deal with, which helps to inform the picture of what MP3 will probably look like—i.e.,they will need more ‘money printing.’”

- “From the perspective of an investor, if you look at the level of the returns relative to levels of volatility, the expected reward-risk could make those who are long a lot of assets view that terrible-returning asset called cash as appealing.” (emphasis mine)

Cash? Appealing? These are smart guys, folks.

When? How much? 25%? Easy to explain that one to your client when the market corrects. Tougher to do when it rallies like it has the last several days.

Here’s an idea I incorporate:

- Find a process that allows you to systematically increase cash (decrease equity exposure) or increase equity exposure (decrease cash exposure). The easy part may be raising the cash, but the harder part will be determining when to get back in. So, I believe it’s best to have a formal process that you have conviction in.

- I use our CMG Ned Davis Large Cap Momentum Index in just this way. Currently, for an investor with a moderate growth profile, I like 30% equity exposure and within that weighting, we trade one-third of it (10% of our total portfolio) between a strategic beta large cap index and short-term Treasury bills (via the ETF “BIL”). We moved 10% of our portfolio to BIL on June 30, 2015 when the S&P 500® Index was at 2063. The S&P 500® recently bottomed at 1812 and sits today near 1950.

- The verdict is still out, but this is about process, risk management and opportunity. The CMG Ned Davis Large Cap Momentum Index is my favorite equity market indicator, but, of course, there are others. Come up with a process you have conviction in and can stick to. (I post the signal each week in Trade Signals).

That doesn’t fully answer the 25% to cash conundrum, but it moves the needle in that direction. Personally, I believe a broader portfolio view that includes a weighting of 40% to liquid alternatives is a better bet than 25% in cash. Mix together five, six, seven or eight experienced managers (via mutual funds or ETFs) that have different return drivers (low correlation to each other), are not dependent of a bull market in stocks to create gain and follow a risk management process that is disciplined and sound. Managed Futures, in general, is a category that is doing well year to date. (Click here for a recent, interesting article on liquid alternatives by DailyAlts.)

Further, when equity valuations become attractive (and they will), change the bucket weightings from underweight equity exposure to overweight: maybe 70% equities, 10% fixed income and 20% liquid alts. Our industry calls this type of movement Strategic Asset Allocation. Consider the forward return opportunities and tilt the weightings.

Tactical strategies that have the ability to pivot between various asset classes, such as bonds, utilities, small caps, value/growth, health care, etc. can play an important role in a portfolio. To this end, I was interviewed by Barron’s recently. Click the image below. I share what we are seeing in regards to asset classes that are leading.

I personally don’t believe you need to go 25% or 30% cash. Include a diverse set of return drivers and have a game plan in place that you can stick to.

Gold is catching everyone’s attention and it appears it should. The trend for gold is now bullish. I wrote an article for Forbes this week titled, Charting The New Bull Market In Gold, in which I share a few ideas on the direction of gold and mention a few ETFs to consider. In short, it is time to put some gold in your alternative bucket.

You’ll also find a link today to Lacy Hunt’s most recent quarterly letter. I share some high-level notes below. Hint: he sees interest rates going much lower. I believe Dalio is correct: “Expect more money printing.”

This week’s post is short. I hope you enjoy it and find it helpful. Please share with me any feedback/questions you might have. This weekly OMR research dive has become a labor of love. It helps me and I hope it helps you as well. Thank you for spending time with me each week. Please know you are very much appreciated!

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Included in this week’s On My Radar:

- Forbes, Charting The New Bull Market In Gold

- Lacy Hunt – Quarterly Review and Outlook

- Trade Signals – New “Buy” Signals on Bonds and Gold; Cyclical Equity Market Trend Remains Negative – Posted 2-24-2016

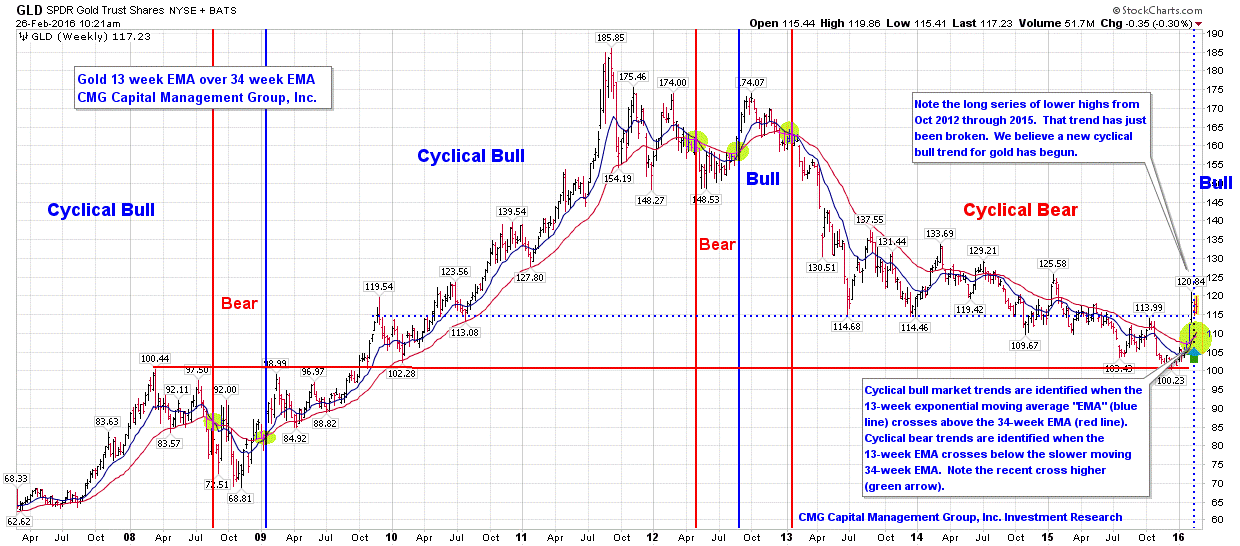

Forbes, Charting The New Bull Market In Gold

Below is the chart on gold. Note the green arrow in the bottom right. It identifies the beginning of a new cyclical bull period for gold. You’ll also find the chart along with an explanation on how to read it in my Forbes article, Charting The New Bull Market In Gold. I share several ETF ideas as well.

I conclude it is time to put some gold in the alternative portion of your portfolio(s). Call it a 5% to 20% weighting depending on an investors overall return and risk objectives. I like no more than 10%.

Understanding Gold

“At times, gold behaves like a commodity. The gold price tracks the ups and downs of commodity indexes. At other times, gold is viewed as a safe-haven investment. It competes with stocks and bonds for investor attention. And on occasion, gold assumes its role as the most stable long-term form of money the world has ever known.

Right now, gold is behaving more like money than a commodity or investment. It is competing with central bank fiat money for asset allocations by global investors. That’s a big deal because it shows that citizens around the world are starting to lose confidence in other forms of money such as dollars, yuan, yen, euros and sterling.” James Rickards

Many investors often think gold is an inflation play. It is not. U.S. investors often think of gold as an asset play dependent on what might be going on domestically in the U.S. It is a global play with millions of buyers for a variety of diverse reasons. Right now, I believe gold is a confidence play or a growing lack of confidence in government. In any event, it is showing both relative price leadership and a more positive trend.

Lacy Hunt – Quarterly Review and Outlook

Several high level notes:

- 2015 – A weak economic finish to a disappointing year. Surely the economy would be kick-started by: three rounds of QE and forward guidance, a record Federal Reserve balance sheet: and an unprecedented increase in federal debt from $9.99 trillion in 2008 to $18.63 trillion in 2015. Further, stock prices had gained sufficiently over the past several years, thus the so-called wealth effect would boost consumer spending.

- In short, the economic facts of 2015 displayed no impact from these massive government experiments. (Lacy dives into the facts.)

- The global economic picture is just as disappointing. Reflecting the depth of the underperformance, world trade was essentially flat for the first time since 2009. (Lacy dives into supporting evidence.)

- Since the introduction of unconventional and untested monetary policy operations like QE and forward guidance, an impressive amount of empirical evidence has emerged that casts considerable doubt on their efficacy. (Lacy points out that evidence.)

This is, at least for me, where the research gets interesting:

- In a paper presented at the Fed’s 2013 Jackson Hole Conference, Robert Hall of Stanford University and Chair of the National Bureau of Economic Research Cycle Dating Committee wrote, “An expansion of reserves contracts the economy”.

- Negative interest rates would have the same non-productive characteristics as QE.

- Until more recently, a casual explanation of why QE and forward guidance should have had negative consequences was lacking. Until now as explained in a chapter in a new book titled, “Where Did the Growth Go?” The book is co-authored by Michael Spence (2001 recipient of the Nobel Prize in economics) and Kevin M. Warsh (former Governor of the Federal Reserve). The book is titled, Growing Global: Lessons for the New Enterprise, published in November 2015 by The Center for Global Enterprise.

- The Spence and Warsh point is that “the post-crisis policy response” contributed to and helps to explain the slower economic growth during the past several years.

The most interesting part for me:

- Their line of reasoning is that the adverse impact of monetary policy on economic growth resulted from the impact on business investment in plant and equipment. Here is their casual argument: “…QE is unlike the normal conduct of monetary policy. It appears to be qualitatively and quantitatively different. In our judgment, QE may well redirect flows from the real economy to financial assets differently than the normal conduct of monetary policy.” In particular, they state: “We believe the novel, long-term use of extraordinary monetary policy systematically biases decision-makers toward financial assets and away from real assets.”

- In short, “Quantitative easing and zero interest rates shifted capital from the real domestic economy to financial assets at home and abroad:

- CEOs cannot be certain about the consequences of unwinding QE on the real economy. The resulting risk aversion translates to a preference for shorter-term commitments, such as financial assets.

Hunt’s quarterly letter is a must read for me. I particularly enjoyed this most recent piece. He goes on to talk about how the impact of the strong dollar means a continued pipeline of low priced foreign goods and believes that the damage to the U.S. trade balance and corporate profits is far from over. He sees lower vs. higher inflation to be the greater risk and concludes that, “In short, we believe that the long awaited secular low in long-term Treasury bond yields remains ahead.”

Here is a link to the full piece: Print it out and return to it from time to time. It is a great read.

Trade Signals – New “Buy” Signals on Bonds and Gold; Cyclical Equity Market Trend Remains Negative – 02-24-2016

S&P 500® Index 1908

By Steve Blumenthal

February 24, 2016

Since Wednesday’s post, HY has moved back to a “buy” signal. Short covering or a new intermediate trend move? We’ll know soon enough. Yields are particularly attractive. We have traded back into HY funds. Stops are in place.

Included in this week’s Trade Signals:

Equity Trade Signals:

- CMG Ned Davis Research (NDR) Large Cap Momentum Index: Sell Signal – Bearish for Equities

- Long-term Trend (13/34-Week EMA) on the S&P 500® Index: Sell Signal – Bearish for Equities

- Volume Demand is greater than Volume Supply: Sell Signal – Bearish for Equities

- NDR Big Mo: See note below (active signal: sell signal on 1-15-16).

Investor Sentiment Indicators:

- NDR Crowd Sentiment Poll: Extreme Pessimism (short-term Bullish for Equities)

- Daily Trading Sentiment Composite: Extreme Pessimism (short-term Bullish for Equities)

Fixed Income Trade Signals:

- Zweig Bond Model: Buy Signal

- High-Yield Model: Neutral (In a buy signal as of 2-26-16)

Economic Indicators:

- Don’t Fight the Tape or the Fed: Indicator Reading = 0 (Neutral for Equities)

- Global Recession Watch Indicator – High Global Recession Risk

- S. Recession Watch Indicator – Low U.S. Recession Risk

(S&P 500® Index monthly declines of -4.8% or greater below its five-month smoothing (MA) signaled recession 79% of the time: 1948 – Present). Data is updated each month end. Currently -3.0% below five-month smoothed moving average.

Tactical — CMG Opportunistic All Asset Strategy:

- Relative Strength Leadership Trends: Utilities, Fixed Income, Muni Bonds and Gold are showing the strongest relative strength:

Here is a link to the Trade Signals blog page.

Personal Note

I think the overall trend for interest rates is lower. I’m neutral at best on the equity markets seeing the potential upside target for the S&P 500® Index at 2150 (over-valuation) and the potential downside near 1600 (assuming earnings of $111 for the S&P 500® constituents). That level would mark fair valuation looking at median P/E over the last 50 or so years tied to estimated earnings of $111. This is just a guess and we could see movement beyond those bands. Let’s just call this the current range I feel we find ourselves in. Ultra-low interest rates should help us hold the downside. I continue to believe a recession is in our future (this year or next). If it occurs, expect -30%, -40%, -50% or even -60%. Recessions are an integral part of the business cycle. They happen so play good defense until a better buying opportunity presents.

Playing defense doesn’t mean you can’t make money. It just means that overweight traditional buy-and-hold stocks and bonds is a risky mix. Reduce and hedge your equity exposure, remain tactical with bonds and overweight alternatives (I define as anything other than traditional buy-and-hold stocks and bonds).

Overall, put me in Lacy’s camp as it relates to the economy and I believe Dalio has it right. “Expect more money printing” – indeed.

My youngest son Kyle is playing the Prince in tonight’s high school musical “Into the Woods.” Of course, his brothers are attending and the dinner table comments have ranged from “do we really have to go” to “can I sit in the back and watch videos on my phone” to “is it ok if I fall asleep”. I’d like to say they are just poking fun, but I think they are serious. Kyle has enjoyed the banter. Personally, I can’t wait. Brianna is coming in for Saturday’s show, so it will be back to it for me.

It will be Susan, me and the boys rushing to get some burgers at Shake Shack (and a Hop Devil IPA for the grownups) after the show. I view these big event moments as dividends. Kind of a return on the emotional investment we all pour into our children and there is no better return than ones that pang your heart. That cold IPA might pang my heart as well.

Back on a plane early Sunday morning. I’m attending the CBOE Risk Management Conference in Florida. A few days with some of the leaders in hedging strategies using exchanged traded options. Much to learn. There are many books on options hedging but it is confusing to many. The tools exist. I’m thinking about a new paper that breaks several processes down into a relatively simple understanding. Revision #3 of the white paper on the Total Portfolio Solution is with the editor. I’ll provide a link soon.

I will travel to Indianapolis in mid-March for an advisor’s client event and to San Francisco on March 23 and 24 for several meetings. And put Mauldin’s Strategic Investment Conference on your calendar – May 24-27. Though as I just checked the website – the event is sold out. Speakers include former Dallas Fed President Richard Fisher, James Grant, Lacy Hunt, Gavekal’s Anatole Kaletsky, David Rosenberg, David Zervos, Gary Shilling and more. We’re helping to sponsor the event and the speaker line-up looks outstanding. I’ll be sure to share my notes with you after the conference.

Have a wonderful weekend. Thank you for your interest in my weekly missives. I hope you find the information helpful. You can help me grow – please share it with a friend if you feel it appropriate.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

With kind regards,

Steve

Stephen B. Blumenthal

Chairman & CEO

CMG Capital Management Group, Inc.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Chairman and CEO. Steve authors a free weekly e-letter entitled, On My Radar. The letter is designed to bring clarity on the economy, interest rates, valuations and market trend and what that all means in regards to investment opportunities and portfolio positioning. Click here to receive his free weekly e-letter.