Sweden Declares War on Cash, Punishes Savers

Sweden Declares War on Cash, Punishes Savers with Negative Interest Rates

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Among the endangered species in Sweden are the gray wolf, European otter—and cash. Back in June, I shared with you the story of how, in 1661, the Scandinavian monarchy became the first country in the world to issue paper money. (It was an unmitigated disaster, by the way.) Now it might be the first to ban it altogether.

All across Sweden, cash—the physical kind, not cash in the bank—is disappearing. Many if not most businesses have stopped accepting it. ATMs are now as uncommon as pay phones. Churchgoers tithe using mobile apps. Fewer and fewer banks even accept or dole out cash.

Here’s the chart showing the decline in the average yearly value of Swedish banknotes in circulation:

So what’s going on?

For one, the Swedish people have enthusiastically embraced mobile payment systems. Even homeless newspaper vendors now carry card scanners.

But that’s not the concerning part.

Cash’s demise appears to be orchestrated by Sweden’s central bank, which of course stands to benefit from the switch. In a purely electronic system, every financial transaction is not only charged a fee but can also be tracked and monitored. Plus, taxes can’t be levied on cash that’s squirreled away in Johan’s sock drawer.

Since July, interest rates in Sweden have lingered in negative territory, at -0.35 percent, forcing accountholders to spend their money or else see their balances slowly melt away. Negative rates can also be found in Denmark and Switzerland, where they’re as low as -1.25 percent. The Swiss 10-year bond yield plummeted to -0.40 percent on Tuesday, which means people are paying the government to hold their “investment.”

Nick Giambruno, senior editor of Casey Research’s International Man, calls negative interest rates in a cashless society a “scam.” His perspective is worth considering:

If you can’t withdraw your money as cash, you have two choices: You can deal with negative interest rates… or you can spend your money. Ultimately, that’s what our Keynesian central planners want. They are using negative interest rates and the “War on Cash” to force you to spend and “stimulate” the economy.

The War on Cash and negative interest rates are huge threats to your financial security. Central planners are playing with fire and inviting a currency catastrophe.

Sovereign Man goes even further, writing:

Financial privacy has been destroyed. Banks are now merely unpaid spies of bankrupt governments, and they will freeze you out of your life’s savings in a heartbeat if some faceless bureaucrat orders them to do so.

Never-ending Regulations Suffocate Small Businesses and Investors

Over the years, we’ve seen corrupt, unbalanced fiscal and monetary policies wreak havoc in socialist countries all around the globe where governments often feel entitled to restrict and even confiscate their citizens’ assets. In 2008, Argentina nationalized approximately $30 billion in private pension funds. A little over two years ago, the Cyprus government ransacked citizens’ bank accounts to “fix” its own mistakes and mismanagement. Last year Venezuela put $700 credit card spending limits on vacationers visiting Florida. Limitations on how much someone can spend and save can be found in many countries, from Italy to Russia to Uruguay.

In example after example, people’s rights to save and freely hold cash have been disrupted, with tragic results—and today we’re seeing these disruptions in first-world countries such as Sweden, Switzerland and Denmark.

I have faith that the dynamic American political system will not allow these things to happen, but we need to be aware of events in other countries and be vigilant in protecting our assets.

At the same time, many poor policies here at home have disrupted how we save and spend. For example, it’s easier to open a credit card account than a savings or investment account—which obviously doesn’t encourage either of those things.

And a recent flood of new regulations passed down from the federal government continues to suffocate small businesses. Since 1960, the Code of Federal Regulations has grown from 22,877 pages to a bloated 175,268 pages in 2014.

A 2014 study conducted by the National Association of Manufacturers found that these regulations came with a hefty price tag of $2 trillion in 2012 alone, an amount equal to 12 percent of GDP. The negative effects of these laws trickle down for years through various businesses and industries, costing jobs and opportunities at wealth creation—and ultimately creating a downward multiplier effect on the country’s economy.

In December 2013, USGI made the decision to exit the expensive money market fund business because of the increasing regulatory cost of anti-money laundering laws and FATCA. It had become too costly to bear the expense of subsidizing yields so they didn’t fall below zero. With zero interest rates and increasing regulatory costs, protecting the integrity of the $1 net asset value (NAV) had cost the money market fund industry nearly $24 billion in waived expenses between 2009 and 2013, according to the Investment Company Institute (ICI).

So what can we do to protect our wealth? One option is to store a portion of it in gold, which, compared to a basket of 24 commodities, has held on to its reputation as a long-term store of value.

American consumers recognize gold’s resilience and took advantage of lower prices in November. The U.S. mint sold 97,000 ounces of gold coins, up 185 percent from October, after selling out. Meanwhile, American Eagle silver coins hit an all-time annual sales record of 44.67 million ounces.

I always recommend having 10 percent of your portfolio in the yellow metal—5 percent in gold stocks, the other 5 percent in coins and bullion.

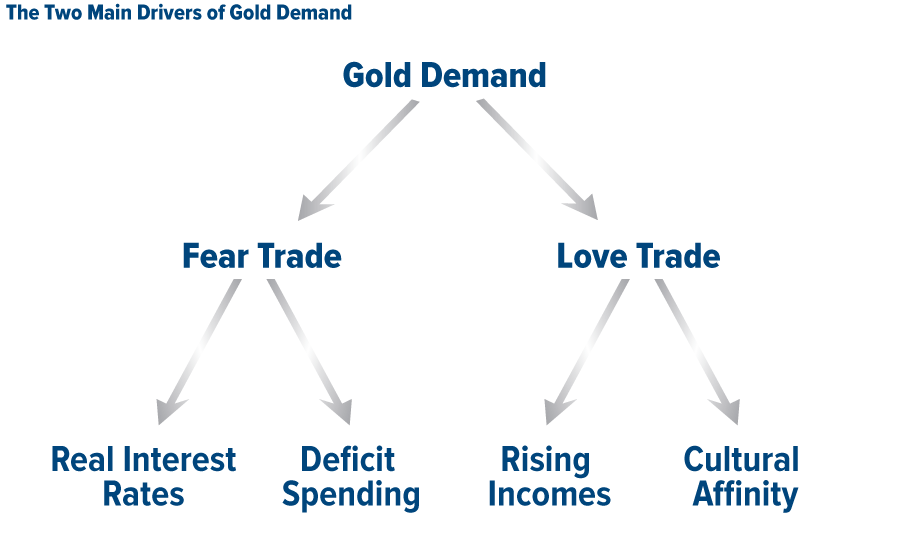

Gold has two pillars of demand: the Love Trade and the Fear Trade.

The Love Trade is associated with traditional gift-giving during the Indian festival and wedding seasons, Christmas and the Chinese New Year. The Fear Trade, on the other hand, has to do with what we’re seeing in Sweden and elsewhere. Negative interest rates and poor government policies wipe out citizens’ ability to save. In such scenarios, investors have historically found shelter in gold.

The Chinese Renminbi Just Went Mainstream

Speaking of currencies, the International Monetary Fund (IMF), as expected, moved to include the Chinese renminbi in its Special Drawing Rights (SDR) currency basket this week, a decision that solidifies the Asian giant’s prominence in the global financial system.

This is indeed an historic milestone, not just for China but also emerging markets in general. The renminbi, also known as the yuan, is the first currency from such a country to join the elite ranks of the U.S. dollar, British pound, euro and Japanese yen. Global intelligence company Stratfor calls this “the start of a new era in the global economic structure” and an acknowledgment of “economic power in new parts of the world.”

It’s worth pointing out that the inclusion is largely symbolic. Many analysts are pointing out that it will have little near-term benefit to China, especially since the change will not go into effect until October 2016.

But according to BCA, among the long-term implications of IMF inclusion is that the “renminbi should eventually claim over 5 percent of global official reserves, or $400 billion, up from about 1 percent.” Currently, the renminbi ranks seventh worldwide as a percentage of global reserves, behind the Australian dollar and Canadian dollar.

To have the renminbi recognized as a reserve currency has been an important fiscal priority for Chinese leadership in recent years. This summer, the country’s central bank announced it had added to its gold reserves substantially, and later it devalued the renminbi 2 percent. That it’s finally been added to the SDR is a huge PR win.

It also means, though, that further economic reforms will need to be made. Country leaders are now charged with ensuring that the renminbi lives up to its status as a high-quality international reserve currency by maintaining its stability and ease of use.

Global Manufacturing Poised for a Strong 2016

Just as we head into the new year, global growth bounced back a bit, alleviating investors’ fears that we were sliding into a recession. Although the global manufacturing purchasing manager’s index (PMI) cooled somewhat in November, it stayed above the three-month moving average for the second month in a row—something it hasn’t done in a year and a half.

China’s manufacturing stabilized in November after six straight months of declines. The Asian giant posted a 48.6 for the month, up slightly from 48.3 in October. It’s still below the key 50.0 mark but headed in the right direction.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average rose 0.28 percent. The S&P 500 Stock Index rose 0.08 percent, while the Nasdaq Composite climbed 0.29 percent. The Russell 2000 small capitalization index lost 1.58 percent this week.

- The Hang Seng Composite gained 0.61 percent this week; while Taiwan was flat and the KOSPI lost 2.69 percent.

- The 10-year Treasury bond yield rose 5 basis points to 2.27 percent.

Domestic Equity Market

Strengths

- Information technology was the best performing sector for the week, increasing 1.62 percent versus an overall advance of 0.08 percent for the S&P 500.

- Newmont Mining was the best performing stock for the week, increasing 17.65 percent. The stock rallied after the company provided an upbeat assessment of its operating and financial future.

- November U.S. vehicle sales improved 10.5 percent year-over-year on a selling-day adjusted basis for a seasonally adjusted annualized rate (SAAR) of 18.1mm, in-line with consensus. After the strong SAAR months in September (18.1mm) and October (18.1mm), November’s momentum was particularly impressive given a tough 8.7 percent comp from last November, two less selling days, and a relatively late Black Friday weekend.

Weaknesses

- Energy was the worst performing sector for the week, falling 4.51 percent versus an overall advance of 0.08 percent for the S&P 500. Friday’s OPEC meeting concluded with no agreement on a unified output cap, with Iran saying it would not accept any limits until it emerges from Western-imposed sanctions.

- Kinder Morgan was the worst performing stock for the week, falling -29.53 percent. The company issued a statement this week which was interpreted by analysts as a warning of an impending dividend cut.

- Credit rating agency Standard & Poor’s lowered its rankings of eight big U.S. banks, saying that the government was less likely to provide any necessary bailouts. Bank of America, Citigroup, Morgan Stanley and Goldman Sachs were all cut to BB+. Bank of New York Mellon, State Street and Wells Fargo were dropped to A, and J.P. Morgan fell to A-.

Opportunities

- U.S. consumer spending has been lackluster for several years, but pockets of strength have emerged. One example is toy and hobby stores where retail sales are booming, in absolute terms and compared with overall retail sales. This trend should persist, based on the leading message from oil price weakness. Not only does it free up purchasing power for discretionary purchases, it also reduces resin costs for toy manufacturers. The group is highly out of favor after plunging nearly 50 percent in relative performance terms. Excessive bearishness could represent latent buying power.

- Despite ticking lower in November, manufacturing new orders in the developed market economies have been trending higher since mid-year. Should they continue to strengthen, this could then reinforce service sector growth.

- U.S. retail sales and consumer inventories are reported next Friday. Both measures will provide an important gauge on consumer spending as we start the holiday shopping season.

Threats

- U.S. equities have rebounded back to key resistance levels, but the only identifiable catalysts remain negative. Domestic financial conditions are tightening while the corporate sector is struggling to generate profit growth. Business sector free cash flow has plunged, representing a threat to the buyback boom. If earnings per share lose the support of repurchase activity, the burden on sales to produce profit gains will intensify. However, the revenue outlook is dim, as a result of the deflationary impact of U.S. dollar strength. The currency is forecasting a meaningful contraction in top-line performance, consistent with the plunge in corporate sector pricing power.

- There are rising challenges for capital market stocks. Marginal deterioration in credit availability and a rising cost of capital will undermine key profit centers, such as advisory fees earned on M&A transactions and capital formation. Both investor and business risk aversion is creeping higher. Furthermore, slipping economic confidence, as measured by the equity-to-bond (E/B) ratio, also signals that return on equity will be pressured through reduced capital markets activity. The contraction in the E/B ratio indicates that stock market returns are lagging behind those of the bond market. It is highly doubtful that equity fund sales will surpass bond fund sales when equity market returns lag, as fund flows tend to follow rather than anticipate performance. If assets under management tilt toward fixed income mandates, then profit margins are likely to narrow.

- The slowdown in buybacks in the technology sector may reflect a weaker profit profile than the recent jump in relative equity performance would suggest. As one of the most globally-exposed sectors, technology companies are particularly vulnerable to the drain from U.S. dollar strength. A declining number of tech industry groups are experiencing rising forward earnings estimates, a trend that anticipates earnings underperformance. Deteriorating breadth is also evident in measures of participation as the number of technology groups with positive cyclical momentum is very slim. The implication is that the recent relative performance jump has been very narrowly based, and calls into question the profit backdrop.

The Economy and Bond Market

Stock and bond prices fell on Thursday and the euro soared as the European Central Bank’s (ECB’s) policy move fell short of expectations. U.S. stocks rallied on Friday after a strong U.S. monthly payrolls report, though European shares remained in the red. Investors now expect a U.S. interest rate hike on December 16. Major global stock indices were down for the week, reflecting broadly weak U.S., Chinese and eurozone economic data. The Chicago Board Options Exchange Volatility Index (VIX) settled below 17 after reaching 19 on Thursday. The yield on U.S. 10-year Treasuries finished the week at 2.27 percent. OPEC maintained its current production quotas, helping send WTI below $40 intraday on Friday and Brent below $43 intraday.

Strengths

- The November jobs report was solid. The economy added 211,000 jobs while the prior two months were revised up by 35,000, leaving the six-month moving average at 213,000. The unemployment rate remained steady at 5.0 percent while the labor force participation rate rose to 62.5 percent.

- Factory orders increased 1.5 percent month-over-month (MoM) in October, up from a 0.8 percent MoM decline in the prior month, and above the expected 1.4 percent MoM.

- Construction spending increased 1.0 percent MoM in October, accelerating from 0.6 percent in September. This was better than market expectations of 0.6 percent. August was revised up as well, to 0.9 percent from 0.7 percent.

Weaknesses

- The ECB fell short of market expectations for QE2, providing only a 10 basis point cut in the deposit rate, a broader inclusion in the types of bonds the ECB will purchase, and an extension of asset purchases to March 2017. Draghi made the usual promises that more action will be taken if the path back to the 2 percent inflation target is too slow, but the ECB did not increase the monthly pace of asset purchases. Market disappointment was reflected in lower European equity indexes, and a surge in the euro and eurozone bond yields as QE trades reversed.

- The plunge in the U.S. manufacturing ISM below 50 in November will likely be ignored by the Fed. The index dropped to 48.6, falling into contraction for the first time since November 2012 and reaching the lowest level since June 2009. The plunge is not surprising given dollar strength, collapsing capital spending in the oil patch and weak global manufacturing and trade activity. Many analysts are downplaying the report because manufacturing is a small part of the economy. The much larger service sector remains robust, underscoring a services/manufacturing divergence that is occurring across several of the major countries. Nonetheless, manufacturing is a highly cyclical part of the economy and can provide important information about the business cycle. It has often led trend changes in the service sector and has been a useful leading indicator for earnings and earnings expectations as well. Thus, it seems incorrect to ignore the manufacturing weakness, but the Fed has set a low bar for a December rate hike.

- The trade deficit widened to $43.9 billion in October from $42.5 billion in September and was larger than the expected at $40.5 billion. Exports fell 1.4 percent MoM to $184.1 billion, and imports declined 0.6 percent MoM to $228 billion.

Opportunities

- According to MRB Partners, headline inflation in the G7 economies declined sharply this year, primarily because of falling oil/energy prices. The base effects of this on headline inflation should begin to fade in the months ahead, pushing the year-over-year rate from near 0 percent to 1.5-2 percent over the next 12 months, even in the absence of any rise in the core inflation rate.

- The U.S. Supreme Court may announce as soon as today whether it will hear an appeal by Puerto Rico to reinstate a law that would allow some island agencies to restructure their debts. The high court is scheduled to review Puerto Rico’s appeal during a private conference today, when it often issues a list of new cases. The disputed law would affect $22 billion of Puerto Rico’s $70 billion in debt. That includes $8.2 billion owed by the Puerto Rico Electric Power Authority, known as Prepa, which is negotiating with its creditors and would gain new leverage from a ruling upholding the law.

- According to Bloomberg Intelligence Economist, the gradual pace of rate hikes that should follow the Fed’s liftoff should not damp U.S. economic growth until borrowing costs rise considerably. With GDP potentially growing more than rates increase in 2016, policy may in fact become more accommodative next year, even amid the onset of normalization.

Threats

- A Fed rate hike this month is widely expected, but the pace of tightening after the initial liftoff remains in question. Currently, Fed policymakers and investors disagree on where interest rates are headed. In real terms, the market believes that short-term interest rates will have to stick close to zero for another four years, contrary to the FOMC’s median “dot plot.” There are a couple of explanations as to why the market is disagreeing with the Fed’s forecast. One possibility is the dollar response and the risks for growth. The dollar could soar if there is a positive growth surprise, as it would magnify the monetary policy divergence between the Fed and the other major central banks. U.S. monetary conditions would tighten, but mainly via dollar strength rather than short-term interest rates. On the other hand, the dollar could weaken if there is a negative surprise, but the growth disappointment would reinforce the view that the Fed will be unable to lift rates off the zero bound anytime soon. Another possible explanation is that investors believe that the headwinds to growth will persist for much longer than do policymakers. Given the market’s disbelief, near-term risks for yields lie mostly to the upside.

- U.S. corporate high-yield bonds remain a risky proposition. According to BCA, only about 25 percent of the U.S. high-yield sectors have produced positive excess returns on a six-month moving average basis. The last few times that such readings were this depressed, 1999, 2008 and 2011, all coincided with periods of high global economic stress. Furthermore, retail investors are losing interest in the high-yield sector. Sales and net assets of high-yield ETF’s and mutual funds peaked in 2014 and have declined sharply this year. This is worrisome since the majority of new issuances since 2009 have been absorbed by retail investors. Ongoing issuance related to M&A activity and equity buybacks could pressure spreads wider if recent retail trends continue.

- Various indicators point to the potential for downside surprises in the capital expenditure cycle. Not only are profit margins beginning to decrease, but energy investment has plunged and there is no reason to expect a rebound until prices are substantially higher. Furthermore, the Duke CEO survey of capital spending intentions is at its lowest reading in three years while most regional Fed surveys confirm this as well.

Gold Market

For the week, spot gold closed at $1,086.84 up $29.43 per ounce, or 2.78 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, surged with a 9.47 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index slipped 0.93 percent. The U.S. Trade-Weighted Dollar Index fell 1.69 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-30 | GE CPI YoY | 0.40% | 0.40% | 0.30% |

| Nov-30 | CH Caixin China PMI Mfg | 48.3 | 48.6 | 48.3 |

| Dec-1 | US ISM Manufacturing | 50.5 | 48.6 | 50.1 |

| Dec-2 | EC CPI Core YoY | 1.10% | 0.90% | 1.10% |

| Dec-2 | US ADP Employment Change | 190k | 217k | 182k |

| Dec-3 | EC ECB Main Refinancing Rate | 0.05% | 0.05% | 0.05% |

| Dec-3 | US Initial Jobless Claims | 269k | 269k | 260k |

| Dec-3 | US Durable Goods Orders | — | 2.90% | 3.00% |

| Dec-4 | US Change in Nonfarm Payrolls | 200k | 211k | 271k |

| Dec-10 | US Initial Jobless Claims | 268k | — | 269k |

| Dec-11 | GE CPI YoY | 0.40% | — | 0.40% |

| Dec-11 | US PPI Final Demand YoY | -1.40% | — | -1.60% |

| Dec-11 | CH Retail Sales YoY | 11.10% | — | 11.00% |

Strengths

- Although gold got most of the attention this week with its price gains, platinum was the best performing precious metal, rising 5.17 percent. The price gains in the metal did not transmit to stock gains for the platinum producers though, as the FTSE/JSE African Platinum Index collapsed 28.74 percent for the week. Despite reinforcement of a December rate hike on news of a strong U.S. jobs report, bullion investors saw past the headline numbers and are taking the long view on gold, according to Bloomberg. Gold prices jumped the most since April, up as much as 2.6 percent. Tai Wong, director of commodity products trading at BMO Capital Markets, said in an interview that the market “seems convinced that once the December hike is out of the way it may be months before the next one…the gold market is moving higher on that sentiment.”

- China’s gold reserves ratio rose to 55.38 million ounces in October. The Chinese central bank website shows an addition of 14 tons made during the month. Other data from the Asian nation shows that China’s Shanghai Gold Exchange withdrawals continued strong, with another 49 tonnes taken out in week ended November 27, bringing the year-to-date total to just over 2,362 tonnes, according to Lawrie Williams.

- Bloomberg reports that India’s gold imports more than doubled during the month of November on the slump in global prices. According to the Indian Express Online, the country’s Sovereign Gold Bonds (SGB) Scheme, however, has seen less-than-impressive debut numbers with the creation of just enough gold backed bonds to be equivalent to about 0.1 percent of the country’s annual consumption of gold of 820 tonnes. Even with the lackluster start to the scheme, the Indian government called the response “excellent.”

Weaknesses

- Gold actually lagged all the precious metals this week. Selling of gold holdings in exchange-traded products fell for the eleventh consecutive day to the lowest since February 2009, according to Bloomberg data. In November investors sold 49.3 metric tons – that’s around three times as much as they bought in the previous three months combined.

- Gold forecasters from Citigroup estimate that the precious metal will average $995 per ounce next year, with the decline in price being a short-term move and mildly improving to an average of $1,025 an ounce in 2017. Another price forecast from ABN Amro shows the metal at $900 an ounce next year, with the bank citing higher U.S. interest rates cutting the demand for gold.

- Palladium, rising just 2.89 percent this week, significantly lagged the gains made in platinum. Reports out of Switzerland showed that they were a net exporter of the metal for the second consecutive month in October.

Opportunities

- BCA Research says although higher interest rates could be bearish for precious metals, there is considerable upside risk in these markets. BCA’s 2016 Commodity Outlook states that if we experience 1) a slower-than-expected rates normalization process, or 2) a complete course reversal by the Federal Reserve brought on by a too-strong U.S. dollar causing growth to stall, precious metals could rally. The rally would come in the wake of the short-covering rally that almost surely would follow.

- UBS is calling for a U.S. dollar pullback, according to the group’s latest note. Marc Mueller from UBS’s technical team thinks a December rally is still likely, but with a U.S. dollar pullback we could see a change of leadership – primarily with a rotation into metals and mining, commodities and emerging markets.

- The Global Mining Observer reports that Lundin Gold will announce its stability agreement with the government of Ecuador in the next few weeks. The basic terms of the agreement include a 22 percent tax rate and flat royalties fixed at close to 5 percent and renewable after 15 years. Lundin Gold could “quickly become a major new gold producer” if they can navigate Ecuador’s tax environment.

Threats

- With the Asian economies struggling, jewelry demand could also end up being weak, notes Bill O’Neill, a partner at Logic Advisors. He sees an undesirable outlook for precious metal: “Fundamentally, the gold market doesn’t look good, psychologically it doesn’t look good and the money flows don’t look good…so that’s a negative trifecta.”

- According to a report from Randgold Resources, a summary of gold industry data shows that total capital injection of $140 billion into the sector (about $90 billion in total equity raised and about $50 billion in total debt raised since 2005) isn’t helping to increase production levels.

Data from Randgold also shows that reserve life is much shorter than portrayed. In order to maintain a lower cost profile, many companies now produce at the economic grade required to make them appear to be low cost. These companies are high grading because these grades are above the reserve grades. As you can see in the chart below, this reduces the average reserve life of the industry.

- Over the past 18 months the U.S. dollar has seen rapid appreciation and triggered a significant drop in commodity prices, reports Sputnik News. This drop includes precious metals, with gold selling at its six-year lowest price. Mark Bristow of Randgold Resources said that “In the medium term, it’s a very bullish outlook for the gold industry. The question is, how long is the gold industry going to supply the market with unprofitable gold?”

Energy and Natural Resources Market

Strengths

- The U.S. Congress has finalized a $253 billion highway bill that calls for over $200 billion in highway spending over the next five years. It is also the first long term highway bill in 10 years, allowing the industry to engage in long term planning. According to Guggenheim Partners, building materials companies such as Martin Marietta and Vulcan Materials should see increased activity and improving backlogs.

- Platinum was the best performing major commodity for the week after rebounding from a six year low that saw its ratio to gold widen to multi year lows. Platinum prices have plunged 31 percent this year as demand was expected to decrease due to Volkswagen’s issues with diesel-engine technology. The rebound provides short term relief to South African production which continues to be under severe stress at current prices.

- Newmont Mining, the biggest U.S. gold producer, was the best performing stock for the week among major natural resource companies. The company provided updated guidance for 2016 and 2017, highlighting increased bullion production with costs remaining below $1,000 per ounce. The stock also benefitted from a significant rise in gold prices and overall bullish sentiment in the space toward the end of the week.

Weaknesses

- Oil prices fell as OPEC announced it will maintain its current output, adjusted upward for the inclusion of Indonesia into the quota. Despite much media noise suggesting Saudi Arabia may push for cuts to output, Iran, Iraq and Russia rejected the possibility of coordinated output cuts. As a result, OPEC is now targeting an overall target level of 31. 5 million barrels per day.

- Zinc was the worst performing metal for the week as China’s war on pollution is expected to reduce zinc demand. As part of the ongoing efforts to control pollution, China plans to further cut excess steel production capacity after the elimination of 31.1 million metric tons last year. Although this may help the price of steel, iron ore and zinc inputs may see lower realized demand.

- ArcelorMittal was the worst performing stock for the week among major natural resource companies as Citigroup downgraded the company citing a rapid deterioration of the spot steel market that could lower earnings expectations going into 2016.

Opportunities

- At current spot prices, oil and copper are approaching their 1990s bottom-of-the-cycle lows. According to a VTB Capital report, commodity prices have increasingly decoupled from fundamentals and while long term trends in real terms, as shown in the chart, show WTI is about 25 percent below and copper is 10 percent below the 1978 “typical” mid-cycle level from the past 30-40 years. VTB cautions that, while real prices are certainly neither definitive nor necessarily accurate, they provide further evidence to suggest the commodity selloff is substantially overdone.

- Gold staged a late rally this week, rebounding from a five year low as the Fed rate hike appears imminent. With the ECB cutting its deposit rate an additional 10 basis points into negative territory, and the monetary divergence of the Fed (tightening) versus the rest of the world (easing), inflation expectations for non-dollar currencies are set to rise, boosting the inflation protection appeal of the yellow metal. It is thus not surprising to see increasing retail demand in China, where it is widely expected that the People’s Bank of China will continue to allow the renminbi to devalue.

- Soybean futures rose to a six week high as dry weather forecasts threaten to reduce output. Brazil, which is forecast to produce 100 million metric tons, may see additional cuts as El Nino threatens crops with higher temperatures and less rainfall. In addition, recent exports from the U.S. to China have resulted in a decrease in U.S. stockpiles.

Threats

- Oil booked its tenth consecutive week of inventory builds as API reported a larger than expected 1.6 million barrel build. News reports highlight that after nine weeks of inventory builds in a row, expectations were for a modest 900k barrel draw. Oil traded down following the disappointing update.

- Asia’s liquefied natural gas (LNG) glut is expected to worsen as new production comes to the market at the same time as demand from top buyers Japan and South Korea, as well as China, continues to weaken. According to Reuters, new supplies will outweigh overall orders, resulting in a low gas price outlook for years to come.

- With the December rate hike a given in investor minds, MLPs and other rate sensitive areas of the market have been hit hard. The investor appeal of MLPs, which are catalogued as high income instruments, continues to wane as Fed rate hike expectations continue their rise, and oil declines on news that OPEC will be maintaining supply levels.

China Region

Strengths

- China A-Shares was the best performing market in Asia this week, as the International Monetary Fund’s (IMF’s) inclusion of the Chinese renminbi in its SDR basket, along with speculation on more property policy easing to counter disappointing manufacturing activity, aided investor sentiment. The Shanghai Composite Index gained 2.58 percent this week.

- Financials was the best performing sector in Asia this week, led by a rally in Chinese property developers on speculation of further policy easing in the real estate sector to smooth the country’s industrial slowdown. The MSCI Asia Pacific ex Japan Financials Index gained 1.59 percent this week.

- The Malaysian ringgit was the best performing currency in Asia this week, strengthening by 1.65 percent, as the country’s October exports growth surprised on the upside, rising 16.7 percent year-over-year, driven by a sizable recovery in exports of machinery and transports equipment.

Weaknesses

- South Korea was the worst performing market in Asia this week, as foreign investors net sold Korean equities by the largest weekly amount since late August to help de-risk ahead of the Federal Reserve’s decision in mid-December. The Korea Stock Exchange KOSPI Index retreated 2.69 percent this week.

- Technology was the worst performing sector in Asia this week, as large-cap technology bellwethers in the region, in both hardware and software spaces, corrected from the previous week’s advance. The MSCI Asia Pacific ex Japan Information Technology Index lost 0.89 percent this week.

- The South Korean won was the worst performing currency in Asia this week, weakening by 0.71 percent, on intensified worries that persistent Chinese demand slowdown could add to Korea’s exports challenges and weigh on its growth outlook next year.

Opportunities

- This week’s rally in Chinese property stocks, amid renewed weakness in China’s official Purchasing Managers’ Index (PMI) data and rising layoff announcements in the country’s metals and mining industry, best reflects investor expectations of further government policy support for the economically-critical property sector to smooth the slowdown. Land sales have shown initial signs of recovery and historically led property investment by six months. Reset of mortgage rates at least 125 basis points lower (effective January 1, 2016 thanks to the cumulative cuts so far this year) is expected to save homeowners RMB 160 billion, according to CLSA. Property and select consumer categories should be major beneficiaries going forward.

- This week’s approval of the Korea-China free trade agreement by the Korean National Assembly should help promote trade between the two countries by eventually abolishing tariffs on more than 90 percent of products over the next decade. Korea’s consumer sector, including staples and cosmetics, is set to benefit from this government policy change on top of the structural growth of Chinese inbound travelers to Korea.

- Continued slowdown in the Chinese economy, the market’s perception of a rising interest rate cycle in the U.S., and chronically sluggish global trade next year might shift investor focus back on sectors and countries exhibiting traits of defensive growth, such as health care and the Philippines. Both hold promises of secular expansion thanks to demographics and growth cycle, respectively, and yet remain relatively insulated from cyclical or external headwinds.

Threats

- Macau’s gross gaming revenue declined by a worse-than-expected 32.3 percent year-over-year in November to the lowest level since September 2010, as declines in both premium and mass market businesses widened. In addition to unabated anti-corruption fears, China’s tighter scrutiny of capital flight to combat rising speculation of a fresh round of renminbi depreciation only makes any swift recovery of liquidity influx to Macau casinos less likely. Macau casino stocks are vulnerable to further valuation de-rating, as fundamentals remain at risk.

- Hong Kong’s still anemic October retail sales reinforces the ongoing trend of slowing tourist arrivals in the city, and another 17 percent year-over-year decline in jewelry sales speaks to less mainland Chinese spending because of voluntary avoidance of corruption perception and weaker Chinese renminbi against the Hong Kong dollar. This, coupled with travel warnings in the wake of recent Paris attacks, means Hong Kong retailers and hotels could continue to face headwinds.

- The recent mini-recovery in Malaysian stocks might not be sustainable, given the prospect of a slowdown in both private consumption (led by weaker income growth and high household indebtedness) and public investment due to fiscal retrenchment next year. Lingering uncertainties on crude oil prices and domestic political scandal might continue to weigh on the Malaysian ringgit and investor sentiment.

Emerging Europe

Strengths

- Hungary was the best relative performing market this week, losing 35 basis points. The latest Manufacturing Purchasing Managers’ Index (PMI) data came in at 56.2 versus the prior reading of 55.3. GDP expanded to 2.4 percent on a year-over-year basis.

- The euro and the Czech koruna were the best performing currencies this week, each gaining 2.6 percent against the dollar. Both currencies appreciated 3 percent in a single day on Thursday after the European Central Bank (ECB) announced a small stimulus push that fell short of many investors’ expectations.

- The consumer discretionary sector was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing market this week, losing 6.5 percent. Greek banks underwent a recapitalization process causing massive dilution. Trading of Greek banks on the Athens Stock Exchange was suspended for a few days due to a reverse stock split. The New York Stock Exchange announced it will de-list American Depositary Receipts (ADRs) of the National Bank of Greece after losing 91 percent of their value this year.

- The Russian ruble was the worst performing currency this week, losing 2.7 percent against the U.S. dollar. November inflation declined to 15 percent from 15.6 percent a year earlier. Russia’s Composite PMI, that tracks business trends across both manufacturing and services sectors, crossed above the 50 mark. Despite stronger economic data this week, the ruble weakened along with Brent, which lost 3.8 percent.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

- On January 1, 2016, the Deep and Comprehensive Free Trade Area Agreement (DCFTA) between Ukraine and the European Union will enter into force. It could take from five to 10 years for the agreement to reach its full potential, but it presents Ukraine with the opportunity to be more “pro West.” Russia opposes the agreement, saying it could lead to a flood of European imports across its own borders and could damage the competitiveness of Russian exports in Ukraine.

- HSBC in its November 2015 GEMs Equity Strategy publication said that Russian equities have more rewards than risks. Key elements to watch when considering investments in Russia include the price of oil. Oil & Gas sector equity analysts from HSBC expect Brent to average $60 per barrel in 2016, $70 per barrel in 2017 and $80 per barrel in 2018 (in U.S. dollars). Russia’s 12-month forward price-to-earnings (PE) ratio, relative to other emerging markets, is well below the long-term average and the discount is also visible in its 12-month forward price-to-book (PB) ratio.

- The National Bank of Hungary took control of the Budapest Stock Exchange and has promised a more welcoming environment for companies to encourage new listings. The Budapest Exchange has only a handful of actively trading stocks, with OTP Bank accounting for more than half of the volume. In the past 15 years, the Budapest Exchange has had 35 initial public offering (IPO) listings. In contrast, the Warsaw Stock Exchange had 127 IPO listings in the past five years.

Threats

- This week markets were awaiting a new stimulus push in the eurozone that did not materialize. The euro surged to a one-month high and stock markets in Europe sold off after the European Central Bank (ECB) lowered its deposit rate to minus 0.3 percent and extended its bond buying program, at least until 2017. Many investors were expecting a bigger cut to rates and predicted that the ECB would up its 60 billion euro of monthly bond purchases by at least 10 billion euros or more.

- On December 3, Poland announced plans to tax banks at 0.39 basis points of their assets, as part of the government’s plan to introduce a levy on the sector in order to finance its social spending. Starting February 1, banks will pay a tax of 0.0325 percent of assets per month, amounting to 0.39 basis points a year. The rate for insurers will be 0.05 percent per month.

- The eurozone’s Retail PMI data for November came in weaker than the prior reading, 48.5 versus 51.3. Inflation was reported at 0.1 versus an expected 0.2. Manufacturing PMI was reported at 52.8 and in-line with the prior reading, while Service and Composite PMIs were reported at lower levels, but still above the 50 mark that separates growth form contraction.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| DJIA | 17,847.63 | +49.14 | +0.28% |

| S&P 500 | 2,091.69 | +1.58 | +0.08% |

| S&P Energy | 473.94 | -22.40 | -4.51% |

| S&P Basic Materials | 287.05 | +1.22 | +0.43% |

| Nasdaq | 5,142.27 | +14.75 | +0.29% |

| Russell 2000 | 1,183.40 | -18.98 | -1.58% |

| Hang Seng Composite Index | 3,059.66 | +18.53 | +0.61% |

| Korean KOSPI Index | 1,974.40 | -54.59 | -2.69% |

| S&P/TSX Canadian Gold Index | 136.50 | +13.98 | +11.41% |

| XAU | 49.95 | +5.03 | +11.20% |

| Gold Futures | 1,086.20 | +30.00 | +2.84% |

| Oil Futures | 40.11 | -1.60 | -3.84% |

| Natural Gas Futures | 2.18 | -0.03 | -1.40% |

| 10-Yr Treasury Bond | 2.27 | +0.05 | +2.30% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| DJIA | 17,847.63 | -19.95 | -0.11% |

| S&P 500 | 2,091.69 | -10.62 | -0.51% |

| S&P Energy | 473.94 | -47.93 | -9.18% |

| S&P Basic Materials | 287.05 | +1.52 | +0.53% |

| Nasdaq | 5,142.27 | -0.21 | -0.00% |

| Russell 2000 | 1,183.40 | -6.99 | -0.59% |

| Hang Seng Composite Index | 3,059.66 | -111.52 | -3.52% |

| Korean KOSPI Index | 1,974.40 | -78.37 | -3.82% |

| S&P/TSX Canadian Gold Index | 136.50 | +5.42 | +4.13% |

| XAU | 49.95 | -0.54 | -1.07% |

| Gold Futures | 1,086.20 | -20.90 | -1.89% |

| Oil Futures | 40.11 | -6.21 | -13.41% |

| Natural Gas Futures | 2.18 | -0.08 | -3.58% |

| 10-Yr Treasury Bond | 2.27 | +0.05 | +2.07% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| DJIA | 17,847.63 | +1,745.25 | +10.84% |

| S&P 500 | 2,091.69 | +170.47 | +8.87% |

| S&P Energy | 473.94 | +9.76 | +2.10% |

| S&P Basic Materials | 287.05 | +24.09 | +9.16% |

| Nasdaq | 5,142.27 | +458.35 | +9.79% |

| Russell 2000 | 1,183.40 | +47.23 | +4.16% |

| Hang Seng Composite Index | 3,059.66 | +219.29 | +7.72% |

| Korean KOSPI Index | 1,974.40 | +88.36 | +4.68% |

| S&P/TSX Canadian Gold Index | 136.50 | +14.53 | +11.91% |

| XAU | 49.95 | +4.62 | +10.19% |

| Gold Futures | 1,086.20 | -36.20 | -3.23% |

| Oil Futures | 40.11 | -5.94 | -12.90% |

| Natural Gas Futures | 2.18 | -0.47 | -17.85% |

| 10-Yr Treasury Bond | 2.27 | +0.15 | +6.92% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the commentary were held by one or more of U.S. Global Investors Funds as of 9/30/2015:

Citigroup

Lundin Gold

Martin Marietta

Newmont Mining

OTP Bank

Randgold Resources

Vulcan Materials

These market comments were compiled using Bloomberg and Reuters financial news.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

Chicago Board Options Exchange (CBOE) Volatility Index (VIX) shows the market’s expectation of 30-day volatility.

The ISM manufacturing composite index is a diffusion index calculated from five of the eight sub-components of a monthly survey of purchasing managers at roughly 300 manufacturing firms from 21 industries in all 50 states.

The J.P. Morgan Global Purchasing Manager’s Index is an indicator of the economic health of the global manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P GSCI Total Return Index in USD is widely recognized as the leading measure of general commodity price movements and inflation in the world economy. Index is calculated primarily on a world production weighted basis, comprised of the principal physical commodities futures contracts.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The FTSE/JSE Africa Platinum Mining Index is a market capitalization-weighted index.

The MSCI Russia 10/40 Index is calculated from the MSCI Russia Index, a market capitalization-weighted index designed to measure equity market performance in Russia. MSCI 10/40 Equity Indices are calculated with a base level of 100 as of December 31, 1998.

The Shanghai Composite Index (SSE) is an index of all stocks that trade on the Shanghai Stock Exchange.

The MSCI Asia ex-Japan Index is a free float-adjusted, capitalization-weighted index measuring the performance of all stock markets of China, Hong Kong, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand, India and Pakistan.