Written by

Jae Jun

follow me on

What You Will Learn

- Why Microsoft’s strategic shift to combine software and hardware is working.

- How Microsoft is more expensive with higher expectations than Apple.

- My intrinsic value range for Microsoft.

Here’s my full disclosure first so that you get an idea of where I’m coming from.

- I only have an old iPad 2 that I got from eBay but Apple is my second biggest holding and I outline why Apple is an obvious buy.

- 100% of my laptops have been Windows and I don’t own any shares of Microsoft – yet.

Now that I’m a firm believer in Microsoft’s shift into the hardware space, I’m having a big case of “shoulda woulda coulda” for not having bought Microsoft in the $20 to low $30 range.

My Ignorant Mistakes

First, my biggest error was assuming that Microsoft would be stuck where it was forever. If you just look at the stock chart, it’s easy to think that because Microsoft was stuck at $30 for a decade.

Second was dismissing Surface Pro and its entry into the hardware space as a short-term test.

“It’s done nothing for 10 years, I’ve got plenty of time. I’ll look into Microsoft when there is nothing else to invest in,” I told myself.

But hindsight is 20/20 and money isn’t made in the stock market by dwelling on misses.

Why Microsoft Is Not Copying Apple

Keep in mind that I have no interest in making this into a tech gizmo article about specs, performance, future products and comparisons of the new Surface product line with the MacBook.

What is happening and is becoming more obvious with each Surface model is that Microsoft’s entrance into the hardware industry is revitalizing the PC space.

The company’s software and hardware combo strategy is finally working.

Why shouldn’t it?

Apple has shown how successful the business model is. Outside of the phone and computing industry, it’s common sense to provide your own software and hardware.

- The Bloomberg Terminal provides HW and SW for a massive amount of money and is entrenched in the financial industry.

- Square provides fantastic looking and functioning credit card swiping hardware with quality software.

- Fitbit (NYSE:FIT) has a gorgeous user interface that functions seamlessly with the HW.

- GoPro (NASDAQ:GPRO) will be stupid to distribute Adobe Premier Pro as its video editor.

So it doesn’t make sense to claim that Microsoft is copying Apple. To put it politely, Microsoft woke up from a 10-year beauty sleep.

How Microsoft Is Revitalizing The Industry

Just a few years back, it was unthinkable that Microsoft would be competing with its hardware partners like Dell and HP (NYSE:HPQ). But you can’t hide the cold hard facts that PC shipments dropped 11% last quarter and have declined for 14 quarters straight.

But Microsoft did what no other PC manufacturer was able to do. It created a product that broke boundaries and illustrated the capabilities of its software. This is why Microsoft will succeed and why I’m a firm believer in the company now.

Until recently, pure play hardware companies could only take their products and “innovation” to what the fastest chip was, how light and thin they could make the product. Their thinking and innovation was constrained to hardware specs instead of seeing beyond and breaking through convention.

You had to deal with big fat and ugly laptops from Dell, HP and other manufacturers.

Not anymore.

Thank you Microsoft.

Finally… Microsoft Is Sexy

The Surface Pro and Surface Book is a glimpse of Microsoft’s newfound sexiness and control over the entire product development.

Responses to the Surface Book?

Expect Increasing Cash Flow

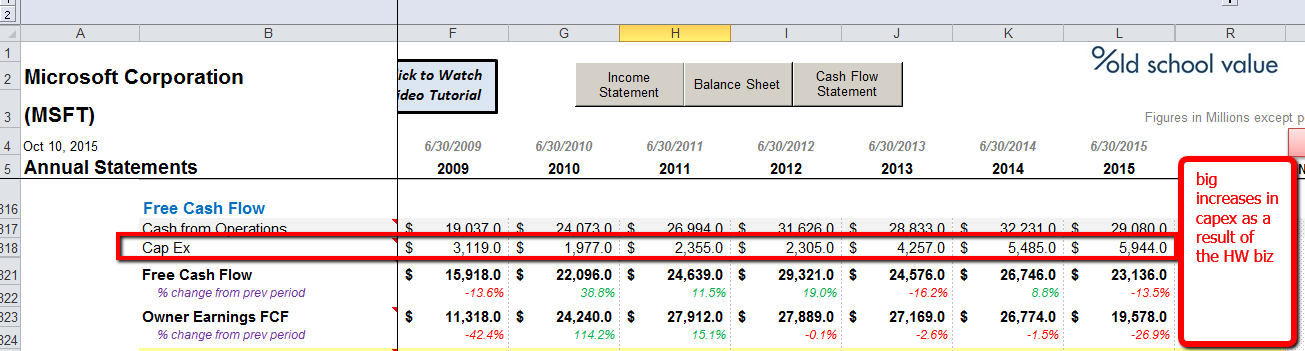

Microsoft is already a dynamite free cash flow machine thanks to Office, Windows and Enterprise business.

The Office subscription model is growing and now add hardware revenue growth that is sprinting forward. Three years ago, the Surface business generated a whopping zero.

Today, it’s up to $3.6 billion in sales.

Capital expenditures have obviously increased to support such sales, but the level of investment is promising.

MSFT Capex Growth | Enlarge

MSFT Capex Growth | Enlarge

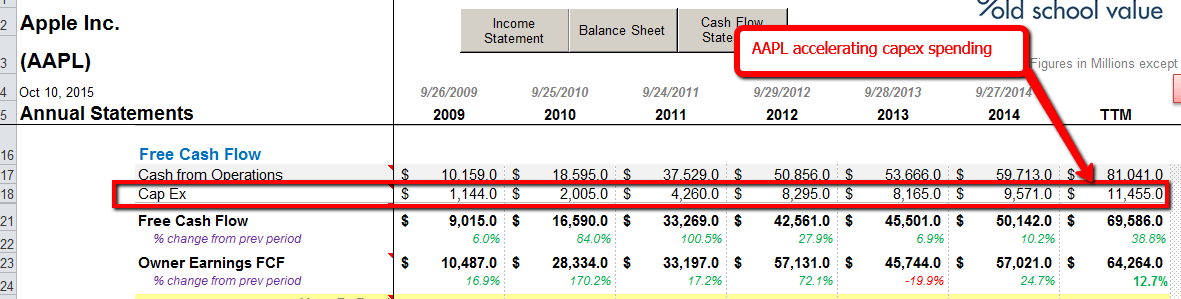

For comparison, Apple isn’t slowing down either.

AAPL Capex Growth | Enlarge

AAPL Capex Growth | Enlarge

At the moment, no company comes close to Apple in terms of FCF and the amount of money it holds, but this is a whole new revenue and FCF stream for Windows that is growing quickly.

When you put the $3.6 billion in sales into context, it makes up less than 4% of total revenues today, but my sneaking suspicion is that it won’t be so negligible in 3 years’ time and it will be another huge push to the bottom line.

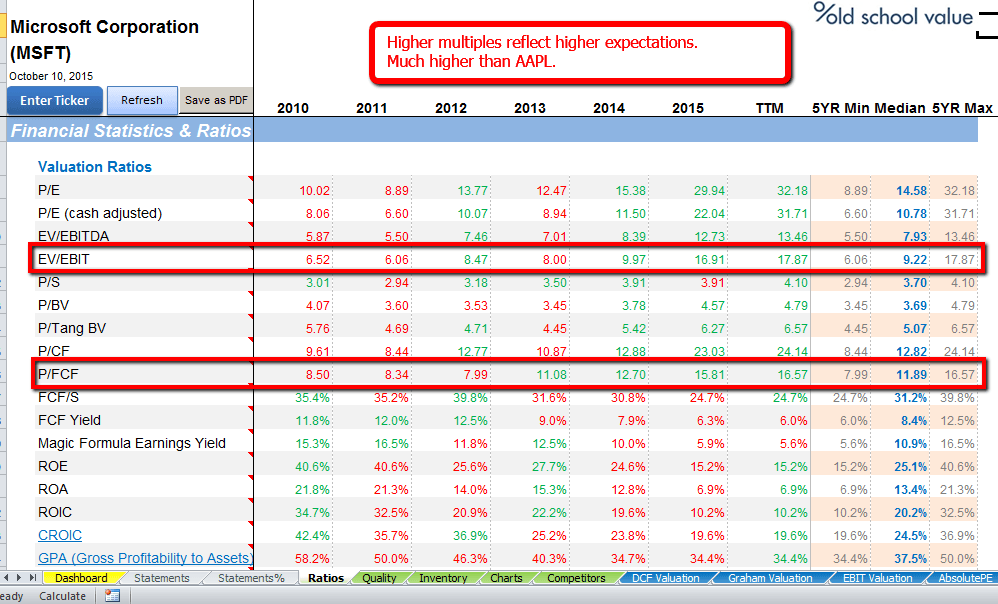

Microsoft Is Expensive With High Expectations… Compared To Apple

I would never have imagined saying this, but Microsoft is more expensive with higher expectations than Apple.

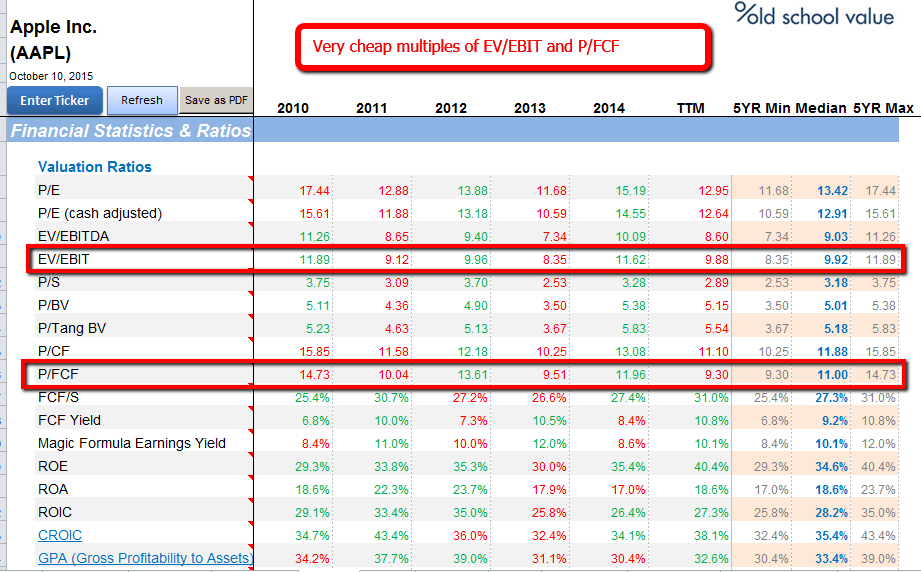

First, look at the EV/EBIT and P/FCF numbers for Apple.

AAPL Valuation Ratios | Enlarge

AAPL Valuation Ratios | Enlarge

Apple’s only receiving a multiple of 10x EV/EBIT. Its highest multiple in the past 10 years was 27x in 2007.

Now, look at Microsoft.

MSFT Valuation Ratios

MSFT Valuation Ratios

Microsoft ended 2015 with an EV/EBIT of 17x. The highest it has ever been in over 10 years, higher than Apple and above the industry average.

P/FCF is at 16x which is outside of my desired < 15x range.

Goes to show how quickly market sentiment can change for a stock. To prove this, one of the best ways is to perform a reverse DCF.

A reverse DCF will show you what type of growth is expected from the current stock price. It makes it easier to understand whether a stock is over or undervalued.

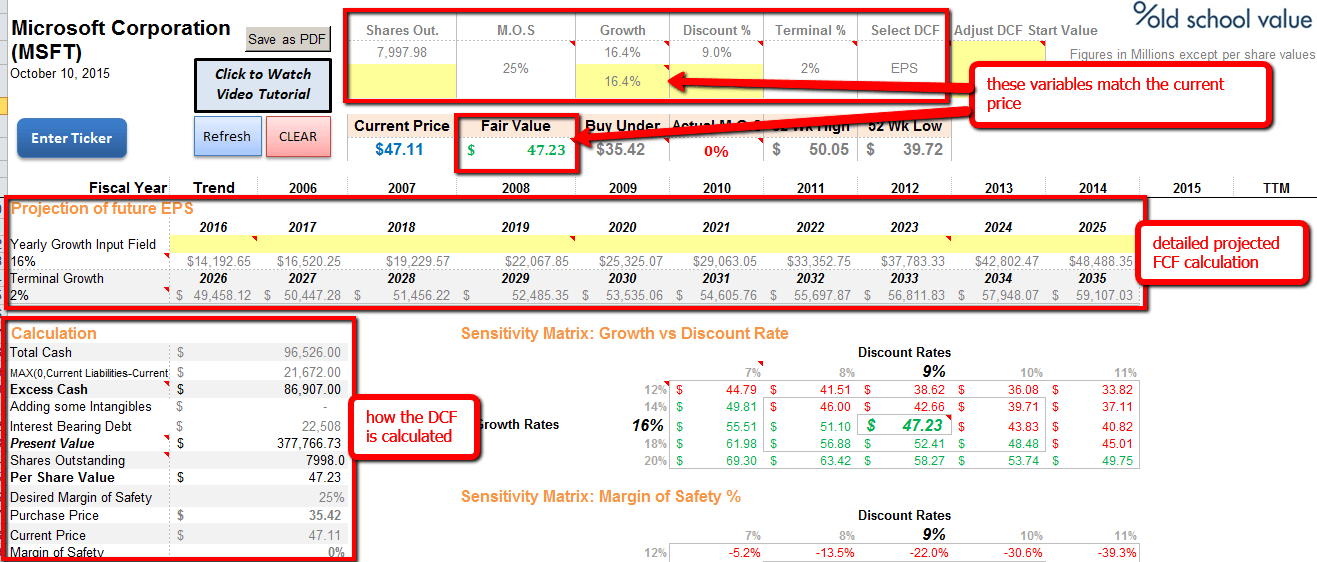

Microsoft Reverse DCF

Looks like the market is pricing in a growth rate of around 16% for Microsoft.

Here are the details if you are interested in the numbers.

MSFT Reverse DCF Breakdown | Enlarge

MSFT Reverse DCF Breakdown | Enlarge

Apple Reverse DCF

Doing the same for Apple shows an expected growth rate of 5% for Apple.

AAPL Reverse DCF | Enlarge

AAPL Reverse DCF | Enlarge

Microsoft’s Valuation Range Is…

Microsoft makes things easier on the valuation side because it’s such a stable business.

It also has plenty of moats.

Office is a moat. Windows is a moat. The Enterprise ecosystem is a moat.

In the reverse DCF, I used the GAAP net income number as that’s what the market uses to price stocks.

However, in the forward DCF valuation side, I could easily use FCF as Microsoft has steady FCF numbers.

Using the following:

- 2015 FCF of $23.1 billion

- Growth rate of 11.1% based on the median of 4 growth numbers I track

- Discount rate of 9%

- Terminal rate of 2%

- Decay rates of 10%

Fair value using a FCF method comes out to $61.

MSFT Forward DCF – Fair Value Calculation | Enlarge

MSFT Forward DCF – Fair Value Calculation | Enlarge

Another viewpoint is using earnings.

I use a Graham Formula method for this and it comes out to $55.

Graham Valuation with Earnings

Graham Valuation with Earnings

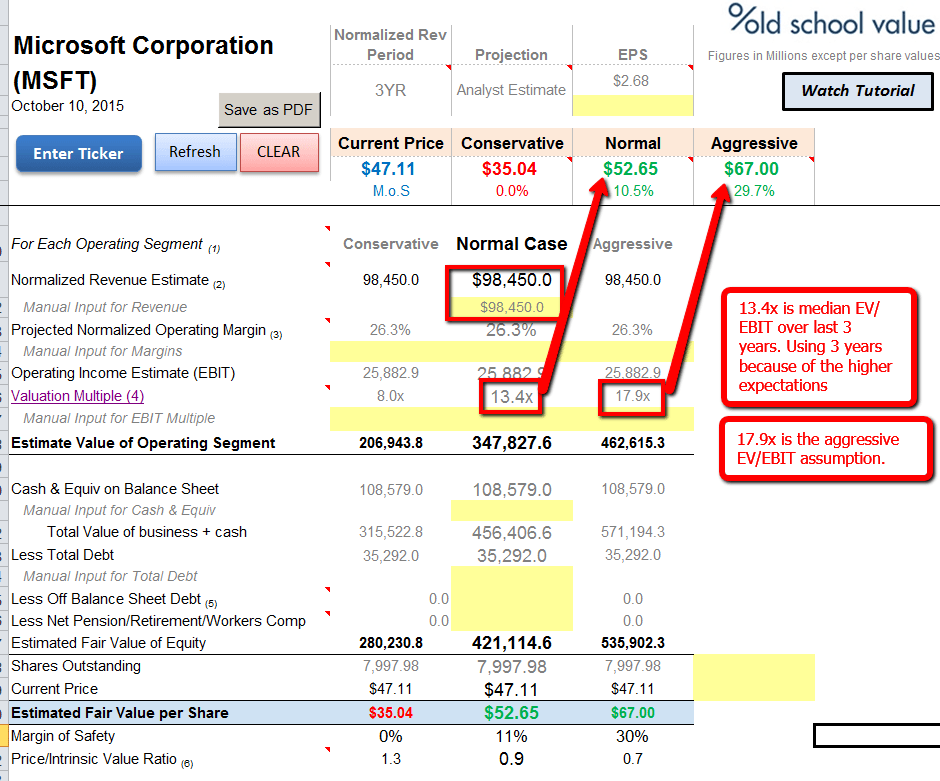

And lastly, here’s another way to value stocks using a simple EV/EBIT approach.

MSFT EBIT Valuation Scenarios

MSFT EBIT Valuation Scenarios

Combine all these different angles of looking at valuation and the fair value range I get here is $52 to $67.

Current stock price: $47

Waiting For A Bigger Margin Of Safety

In terms of margin of safety, a fair vale of $67 isn’t out of the question, but it also requires a lot of things to go in Microsoft’s favor.

Valuation is both art and science, and from the experience of having valued hundreds of stocks, my senses tell me that Microsoft is more in the mid $50 range. It also makes sense from a probability stand point too.

Predicting the time to hit $55 is out of my control and valuation is a moving target. Even if I took $55 as my target, it only offers a 14% margin of safety to the current price.

My fair values could drop or could increase but my investment philosophy is to be disciplined and not chase.

I miss out on a lot of investments, and by waiting for Microsoft to fall lower to be within my margin of safety buying range, I could be missing out on a great opportunity.

But at the same time, having the willpower to say no and sticking with basic principles has saved my bacon plenty of times.

My Final Dilemma

Do I get the Surface Book or not?

This post was first published at old school value.

You can read the original blog post here Why Microsoft Is The New Apple, Except For The Valuation.

No related posts.