The explosion in the numbers of these companies has also given rise to almost as many explanations for the phenomena, some based on rationality and some on the prevalence of a bubble. The rationality-based explanation for the surge in unicorns is that it has become easier to remain a private business, as private capital markets broaden and become more liquid, while it has become more costly to become a public company, with increased disclosure requirements and pressure from investors/analysts. The less benign argument is that investors are being driven by greed to push up the prices of young companies and that this has all the makings of a bubble. I think there is truth in both arguments and that you can have both good reasons for the increased number of large value private businesses and momentum driven froth in the market. However, I will leave that discussion to those who know more about these young companies than I do, and are more confident in their capacity to detect bubbles than I am.

If the conventional definition of a unicorn is a private business with a valuation that exceeds a billion, how do you arrive at the valuation of such a business? While you have no share prices or market capitalizations for these companies, you can extrapolate to the values of private businesses, when they raise fresh capital from venture capitalists or private investors. Thus, if a venture capitalist invests $100 million in a company and gets 10% of the ownership in the company in return, we estimate a value of $1 billion for that company, making it a Unicorn. There are, however, two problems that get in the way of a good estimation. One is that the capital infusion changes the value of the company, creating a distinction between pre-money and post-money values. The other is that the investor’s equity investment generally comes with bells and whistles, designed to protect the investor from downside risk and these protections can skew the value estimate.

In an earlier post on the offers and counter offers that you see on Shark Tank, the show where entrepreneurs pitch business ideas and ask competing venture capitalists for money, I drew the distinction between pre and post money valuations. If the capital raised in an offering is held by the company, rather than used to pay down debt or owners’s cashing out, the value of the company increases by the amount of the new capital raised, leading to the following distinction between pre-money and post-money values.

- Post-money valuation = Investor’s capital infusion/ Percentage ownership received in exchange

- Pre-money valuation = Post-money valuation – Investor capital infusion

In the example above (where an investor invests $100 million for 10% of a firm), the post-money value is $1 billion but the pre-money value is only $900 million. Thus, companies that are smaller than a billion can make themselves look like billion dollar companies, if they are willing to give up enough ownership in the company and can find investors with deep pockets.

While it is unlikely that you will be able to find an investor to offer $950 million in capital for a business with a $50 million valuation, it does illustrate why post money valuations may not always be comparable across businesses.

Note that the protection works fully when the value of the business is between $100 million and $ 1 billion and only if there is a capital event to trigger it. To value this option, you need three more pieces of information:

- Probability of capital event: Since a capital event is the trigger for the protection, there will be no protection if no capital event occurs, a scenario that will unfold if the business unravels quickly. Put differently, the protection is useless if the business never raises any additional capital. (Since the probability of accessing new capital will decrease as the value of the business drops, especially if the drop occurs quickly, the option value is likely to be overstated.

- Expected time to capital event: The timing of the capital event may not be known with certainty, but to the extent that it can be forecast, you need an expected value. If the protection covers multiple capital events, it is the expected time to the last one.

- Degree of protection: Depending on how it is structured, the protection offered an investor can range from 100% (with full protection) of the dollar capital invested to less (with weighted average).

Assume, for instance, that the investor in the example above (who invested $100 million for 10% of the business) if offered complete protection in an anticipated IPO of the company and assume further that there is a 90% chance of the IPO occurring in one year. For the standard deviation, I used the industry average standard deviation of 72.48%, derived from publicly traded stocks in the online software business. The expected value (allowing for the 90% chance of a capital event) that I estimate for the protection option, in this spreadsheet, is $25.116 million and the effects on the pre-money and post money valuations are captured below:

- Unadjusted value of protection = Value of put option = $27.98 million

- Value of protection = Value of put option * Probability of capital event = $27.98 * 0.90 = $25.116 million

- Investment made = Capital injected – Value of protection = $100 mil – $25.116 mil = $74.884 mil

- Ownership stake received = 10%

- Post-money valuation = Investment made/Ownership Stake = $ 74.884/.10 = $748.84 million

- Pre-money valuation = Pre-money valuation – Capital Infused = $748.84 – $100 million = $648.84 million

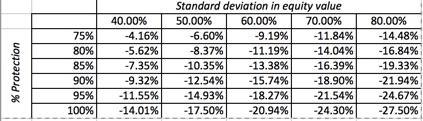

Thus, the capital increase pushed up the value by $100 million and the investor protection clause served to inflate the unadjusted post-money valuation from $748.84 million to $ 1 billion. The greater the investor protection offered and the larger the amount of capital raised, the greater will be the disparity between the true value of the business and its perceived value (based on the transaction details). In the table below, I list out the percentage difference between the true value and the perceived value as a function of investor protection and business risk (captured in standard deviation).

|

| For a $100 million investment for 10% of a company, with a 90% chance of a capital event. |

Thus, if investors get 95% protection in a business where equity values have an annualized standard deviation of 70%, the true value of the business will be 21.54% lower than the perceived value (which is $ 1 billion, based on the $100 million investment for 10% of the firm).

I know that I have simplified the complex world of venture capital deal-making in this example, and that allowing for more sophisticated protection mechanisms and multiple capital rounds will make it more difficult to estimate the protection value. However, this example delivers the general message that the more protections that are offered to investors at the time that they invest in young start-ups, the less dependable are the simple extrapolations of value (from capital invested and ownership stakes received).

It is easy to see why private company investors like protections against downside risk, especially when investing in young start-ups, where valuation is difficult to do. However, there are three consideration that investors need to keep in mind, when deciding how much protection to seek.

- At a fair price, protection adds no value: In investing, you can, for the most part, buy protection agains the downside (in the form of insurance or put options), if you are willing to pay the right price. At a fair price, the protection delivers peace of mind but no additional value. In the example above, the prices that I computed for downside protection were fair prices and neither the investor nor the owner lose at that price. Thus, an investor can either invest $100 million, with no downside protection, and ask for 13.35% of the post-money value of $748.84 million, or get full downside protection and settle for 10.00% of the artificially inflated post-money value of $1 billion.

- Paper Protection: When investing in young start-ups with uncertain futures, the protection clauses in agreements often deliver far less than they promise. The anti-dilution provisions fail if the business you invest in never seeks out additional capital and the liquidation preferences that many investors add to their investments will not provide much respite when these young businesses are forced to liquidated, since their valuations tend to be heavily tilted towards human and idea capital. It should therefore come as no surprise that a significant portion of venture capital investments, promise and protection notwithstanding, yield little or nothing for investors. At the risk of offending some of my readers, I would argue that the protection clauses in most venture capital investments have more in common with the rhythm approach for birth control, a hit-or-miss system that delivers big surprises, than with full-fledged contraception.

- Abdication of valuation responsibilities: Venture capitalists who view building in protection against the downside as an alternative to making valuation judgments are seeking false security. As an investor, if I were asked to choose between investing with a venture capitalist who makes good valuation judgments but is not adept at building in downside protection or with a venture capitalist who is superb at building in downside protection but haphazard about valuation judgments, I would pick the venture capitalist who makes good valuation judgments every single time.

There is also the very real concern is that some venture capitalists who believe that they are protected from downside risk (even if that belief is misplaced) may be inclined to take reckless risks in investing.

There are three benefits to founders and entrepreneurs from granting protection to investors. The first is that they allow them to raise capital in circumstances where its might not otherwise have been feasible. The second is that granting these protections may give the founders/owners more freedom to run the businesses as they see fit, without constant investor oversight. The third is that it allows for inflated valuations, as illustrated in the example above, that can then yield eitherbragging rights or access to more capital.The costs are equally clear. If owners give away too much of the firm for bragging rights, they will be worse off. In the example above, for instance, where we estimated the value of protection to be approximately $25.12 million, giving the investors more than 10% of the unadjusted post-money value of the business in return for $100 million in capital invested would be giving up too much. This cost is exacerbated by a behavioral quirk, which is that the founder owners of a business often tend to be far more confident about its future success than the facts merit. The same over confidence and faith that makes them successful entrepreneurs also will lead you to under price the investor protections that they are giving away in return for capital.

There is nothing wrong with investors seeking protection from downside risk, just as there it is perfectly natural for owners to seek to pump up post-money valuations to make themselves more attractive to new capital providers. The damage occurs when one or both groups let these desires dominate its investing and business decisions. At the risk of sounding presumptuous, I would suggest the following:

- Be real: Both sides would be well served by reality checks. Investors have to be recognize that the protection they are getting is porous and contingent on capital raising events and owners have to realize that offering these protections may alter how and when they raise additional capital, perhaps to the detriment of their businesses.

- Keep it simple: The only people who gain from complexity are lawyers, accountants and consultants. I may be missing the historical context here, but I think that there are far simpler ways of building in protection than the standards that exist today. For instance, rather than continuing with the practice of adjusting price per share for dilution, which is the practice today, I think it would be far simpler to write the protection in terms of dollar capital invested.

- Check the price of protection: At the right price, protection creates value for neither investors nor founder owners. If the protection is priced too high, with the investor settling for a far smaller percentage of the unadjusted value than he or she should, it is not worth it. If the protection is priced too low, founder owners are giving up too much of their businesses in return for the capital raised.

- Don’t forget your fundamentals: While the presence or absence of protection may make a difference in marginal investments, it should not fundamental change the businesses you invest in, if you are investor, or how you run your business, if you are an owner. Thus, if investors use the presence of downside protection as a reason for investing in over valued businesses, they will lose out in the end. (And making that investment convertible and calling it preferred will not make it a good investment.) By the same token, founders who give away much larger percentages of their businesses than they should, to pump up post-money valuations, will regret that decision in good times, and even more so in bad times.

Attachments