Want a simple way to tell which companies are likely to do better than the rest?

Despite how profitable a mechanical net net stock strategy is, I’m always looking for ways to stack the odds even further in my favor.

My most recent articles on Old School Value talk about the benefits of screening out companies with too much debt, and looking at the qualitative fundamentals. This helps to narrow it down to more promising investments.

At Net Net Hunter, I’ve talked a lot about choosing stocks selling for a tiny fraction of what they’re worth.

The lowest price in relation to net current asset value (NCAV).

After years of studying the investment habits of great investors, it’s clear that there are a few simple and reliable ways to identify the best investment candidates.

These techniques involve assessing simple characteristics inherent in investment situations themselves.

When a few of these are stacked together, you can rest assured that the odds of profit are overwhelmingly in your favor.

This same principle applies to Benjamin Graham’s most iconic mechanical investment strategy of investing in net nets.

Share Buybacks Are Awesome

I first read about share buybacks when plowing through one of Peter Lynch’s classic books. Since then, share buybacks has always been one of the top things I look for when assessing the investment merits of a stock.

Sometimes, management gets the idea that the best way to spend the company’s hard-earned cash is to buy its own stock in the open market. In such a situation, management literally sits at the end of a phone line instructing the firm’s broker how much stock to buy and at what price.

I regularly bump into these companies when scanning for lists of international net net stocks which I also share on Net Net Hunter.

Share buybacks are good but you still need to look hard to assess whether management is shareholder friendly.

I also love it when management decides to cancel the shares that have been bought back.

When a stock is canceled, not only is it taken out of circulation but it’s also eliminated as a claim of ownership in the business. This last act is extremely valuable to long-term shareholders for reasons I’ll get to later.

First, lets take a look at what happens when a company repurchases shares under various conditions and how these scenarios can create or destroy shareholder value.

The Effect of Shares that Get Canceled

To understand what happens when shares are repurchased, let’s run a little thought experiment.

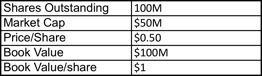

Look at fictional company Bert’s Biotech.

Here are its stats:

Bert’s Biotech

Bert’s BiotechIn this situation, let’s assume that book value is the real intrinsic value of the company and that the firm is undervalued.

Now what happens if Bert’s Biotech buys back and cancels its own shares?

If Bert’s buys back 5M shares, this is what it would look like.

![]()

The book value per share, or intrinsic value in this case, went from $1 to $1.03 which is a 3% increase.

Just by changing the number of outstanding shares, the value of the company increased by 3%.

Why does this happen?

The more money the company spends on buybacks while the company’s shares are undervalued, the more value per share management creates for investors.

The cheaper the company buys back its own stock, the more value it creates for shareholders.

Not All Buy Backs are Equal

When companies buy back shares at an inflated price, shareholder value is destroyed.

You don’t want your company to spend $1 to receive less than a dollars worth.

Every manager verbally espouses the goal of increasing shareholder value but ultimately it comes down to management action. Talk is cheap after all, and there is a lot of talk to please investors and the street.

In a 1985 article in Fortune Magazine, Warren Buffett is quoted as saying:

“All managements say they’re acting in the shareholders’ interests,” he observes. “What you’d like to do as an investor is hook them up to a machine and run a polygraph to see whether it’s true. Short of a polygraph the best sign of a shareholder-oriented management — assuming its stock is undervalued — is repurchases. A polygraph proxy, that’s what it is.”

My Experience with Starbucks (SBUX)

Way before I found my footing as an investor, I invested in Starbucks Corporation (NASDAQ:SBUX).

Starbucks was a great growth stock during the 1990s, and early 2000s. Management was thought to be a dream team of talent working in the interests of shareholders.

The company had risen rapidly for years and was now getting very large.

Large stocks can still be great investments but the larger a company is, the more growth it takes on absolute terms to increase earnings by the same percentages as when the company was younger.

Law of large numbers.

By management’s own admission, Starbucks growth was starting to wane and it couldn’t open enough stores to keep growing at the same rate.

During a certain quarter, despite the sizable dip in growth and the stock trading at nose-bleed levels, management went ahead and repurchased a huge batch of shares.

Back then, I was at least experienced enough to know what this would do to shareholder value and realized that management was trying to keep the stock price in the stratosphere.

While other shareholders applauded management during the next shareholder meeting, I had already sold my shares and was searching for another investment candidate.

While Starbucks looked good for so many years, the actions of management that year spoke volumes about management’s definition of shareholder value.

Starbucks spent the next three years on a steep downhill slide.

Large repurchases used to mop up the effect of large option grants is also depressing.

Options compensation is used far too loosely in USA and sometimes the company will repurchase shares to eliminate the effect of dilution due to option grants.

In such a situation, share repurchases are nothing more than the cost of maintaining top management.

A Vote of Confidence

As you can tell, I look for situations where management is ferociously buying back its company’s undervalued stock.

There are a large number of reasons why it is better to buy back shares cheaply rather than invest the money elsewhere.

………Goldman Sachs Group Inc (NYSE:GS)… in a 1983 presentation to client Getty Oil reeled off a string of reasons the company should buy its own stock. Said Goldman, paraphrased: “You will be purchasing crude oil and gas reserves substantially below fair-market value and below what you would pay in a competitive acquisition of another company. The price will also be below finding costs for new reserves. The risks of Getty’s business are already well known to management. Repurchases do not disrupt operations. Management time will not be spent on the reallocation of people and resources.” – Fortune Magazine

But, it takes confidence to make these share repurchases.

Share buybacks during a major business crisis sends a very strong signal.

No management team expecting a coming cash crunch or needing money to pay its bills will spend money on share buybacks.

In crisis situations, where management sees a clear and present risk to the survival of the firm, top executives are busy thinking of ways to fend off bankruptcy through cost cutting or new sales growth. The last thing management wants to do is waste money buying back the stock of a soon-to-be-dead company.

However, if stock purchases are being made during rough patches, the insiders are doing so because they see it as a good way to invest in undervalued assets and grow shareholder value.

As a net net stock investor, this is an outstanding sign. Companies trading below their net current asset value are troubled. They’re facing huge business problems that depress the price of the firm’s shares to ridiculously low levels.

If the firm is buying its own stock, though, that tells me that management sees the company’s situation turning around soon.

Share Buybacks Produce Outstanding Returns

In the Fortune Magazine study cited above, researchers used Value Line to identify firms that had repurchased at least 4% of their own stock in a given year.

Only company’s not pressured into repurchasing shares were included.

The study looked at the returns investors would earn after the buybacks were publicly announced. Results were recorded from the buyback announcement date to the end of 1984 – at most a span of 10 years.

The outcome was stunning.

As a group, companies which bought back their own shares returned a compound average return of 22.6% versus the S&P 500?s 14.1%.

Look for Share Buybacks

Next time, check out the insider trade information on your stock.

Not only does per share value increase with buybacks, but buybacks also provide a powerful indication that the company will recover sooner rather than later.

If you are having doubts about which stock to select, focus on the ones with share buybacks.

This post was first published at old school value.

You can read the original blog post here How Share Buybacks can Affect Your Returns.

No related posts.