Logica Capital April 2023 Commentary

Logica Capital commentary for the month ended April 30, 2023. Summary Relative to the 1.5% gain for the S&P 500, implied volatility … Read more

Everything ValueWalk knows about Value Investing, including the latest news, tips, features, ideas, value investors and images.

Logica Capital commentary for the month ended April 30, 2023. Summary Relative to the 1.5% gain for the S&P 500, implied volatility … Read more

If I were only able to analyze a single metric before investing in a company it would be ROIC (Return … Read more

Crescat Capital commentary for the month ended April 30, 2023, titled, “Whistling Past The Graveyard.” US policymakers continue to act … Read more

My first trip to the Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) annual meeting in Omaha was over 20 years ago, in 2002. … Read more

Hidden Value Stocks issue for the first quarter ended March 31, 2023, featuring Lowell Capital Value Partners’ investment idea: Sylvamo … Read more

Logica Capital commentary for the month ended March 31, 2023. Summary Markets/factors continued to diverge further in March, with the … Read more

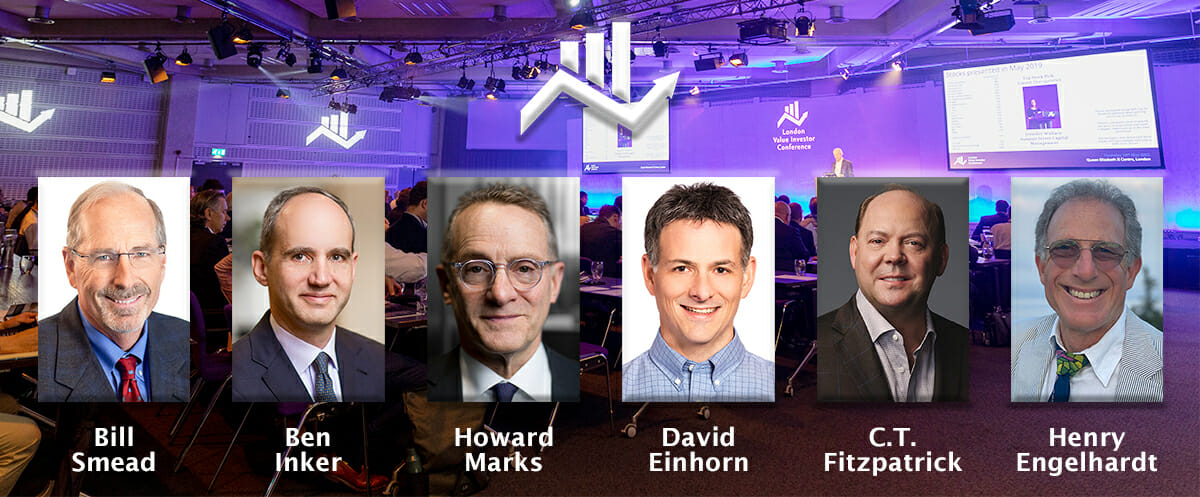

ValueWalk will be covering the London Value Investor Conference which will take place on Thursday 18th May 2023 in Westminster. … Read more

Owning shares of Berkshire Hathaway stock is a way for investors to gain exposure to many of Warren Buffett’s favorite … Read more

Last week, the markets were hit with more market-crushing news: Credit Suisse was under pressure when its top backer Saudi … Read more

What makes a retail business successful? Indeed, how do we measure the success of such a company? Profitability, margins, sales … Read more

Dan Loeb’s letter to Third Point investors for the fourth quarter ended December 2022, discussing his new long position in … Read more

Black Bear Value Partners LP commentary for the fourth quarter ended December 31, 2022. “Don’t play everything; let some things … Read more

Nu Holdings may be seen as an unusual holding in Buffett’s portfolio, but there’s a good reason for it. The … Read more

David Einhorn’s 2022 letter to investors. The full PDF can be viewed here and at the bottom. Dear Partner: The … Read more

Dear fellow investors, As we start the year 2023, we are reminded of the profound poetry from the band, Echosmith, … Read more