Investors, analysts and financial journalists use different measures of value to make their investment cases and it is not a surprise that these different value measures sometimes lead to confusion. For instance, at the peak of Apple’s glory early last year, there were several articles making the point that Apple had become the most valuable company in history, using the market capitalization of the company to back the assertion. A few days ago, in a reflection of Apple’s fall from grace, an article in WSJ noted that Google had exceeded Apple’s value, using enterprise value as the measure of value. What are these different measures of value for the same firm? Why do they differ and what do they measure? Which one is the best measure of value?

What are the different measures of value?

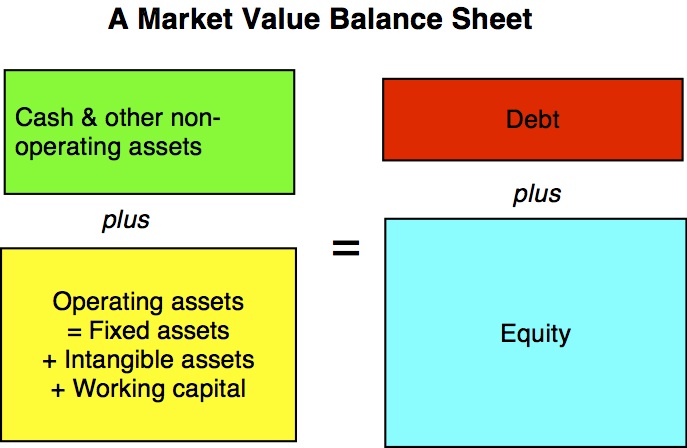

To see the distinction between different measures of value, I find it useful to go back to a balance sheet format, with market values replacing accounting book values. Thus, the market value balance sheet of a company looks as follows:

Note that operating assets include not only fixed assets, but also any intangible assets (brand name, customer loyalty, patents etc.) as well as the net working capital needed to operate those assets and that debt is inclusive of all non-equity claims (including preferred equity).

Let’s start with the market value of equity. Rearranging the financial balance sheet, the market value of equity measures the difference between the market value of all assets and the market value of debt.

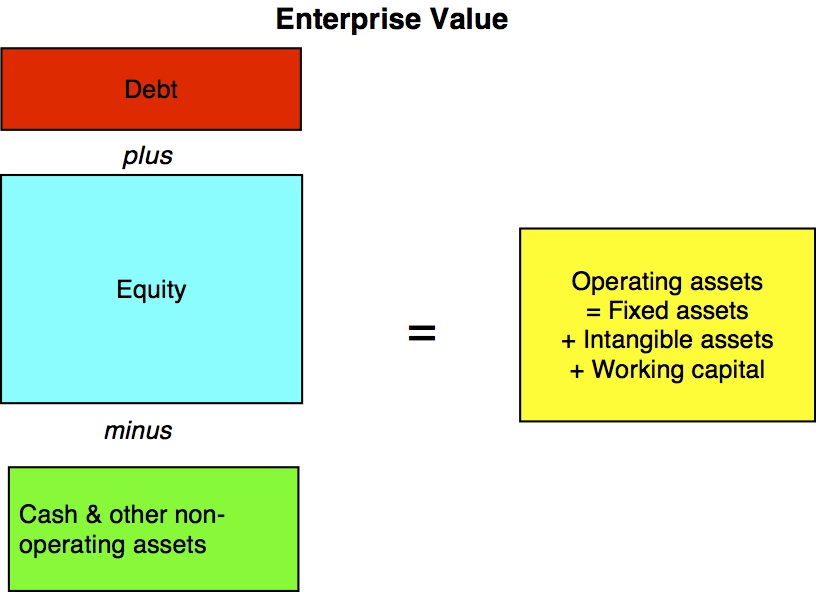

The second measure of market value is firm value, the sum of the market value of equity and the market value of debt. Using the balance sheet format again, the market value of the firm measures the market’s assessment of the values of all assets.

The third measure of market value nets out the market value of cash & other non-operating assets from firm value to arrive at enterprise value. With the balance sheet format, you can see that enterprise value should be equal to the market value of the operating assets of the company.

The measurement questions

To arrive at the market values of equity, firm and enterprise, you need updated “market” values for equity, debt and cash/non-operating assets. In practice, the only number that you can get on an updated (and current) basis for most companies is the market price of the traded shares. To get from that price to composite market values often requires assumptions and approximations, which sometimes are merited but can sometimes lead to systematic errors in value estimates.