More and more in fashion lately in the financial world is companies taking huge write-downs of some flopped acquisitions. Even the big-name players with tremendous resources to scrutinize the acquisition can’t escape this fate.

Microsoft Corporation (NASDAQ: MSFT) had to own up last July to a $6.2-billion write-off of the acquisition of aQuantive, a digital advertising company that Microsoft bought for $6.3 billion cash in 2007. The size of the write-down is significant even for Microsoft. For comparison purpose, Microsoft operating operating profit in Dec. 2012 quarter was $7.8 billion.

Nevertheless, Microsoft can at least have some consolation as just four month later, shares of tech giant Hewlett-Packard Company (NYSE: HPQ) suffered a 11% plunge partly because of a massive $8.8 billion write-off at Autonomy, a British software company it acquired in 2011 for around $10 billion, due to ‘serious’ accounting issues.

This is not just limited to the typically high-flying tech sector either. Last week, Caterpillar, the manufacturer of mining and construction equipment, also said it would need to write off $580 million in 4Q, 2012 goodwill related to a 2011 acquisition in China citing possible accounting fraud.

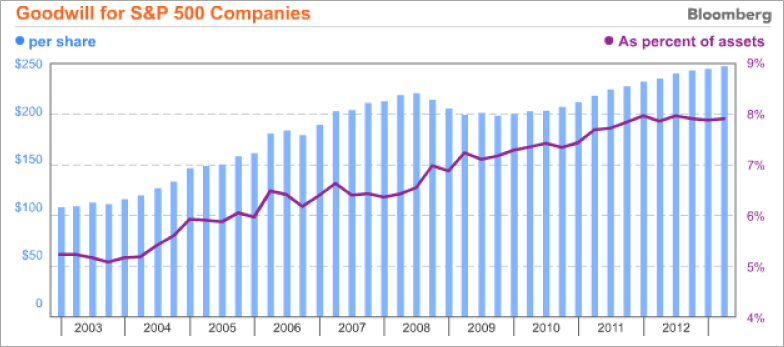

According to Bloomberg, goodwill, basically the amount paid over the book value of the target firm in an acquisition, in the S&P 500 companies have more than doubled on a per-share basis as companies have paid an increasingly higher takeover premium over the underlying asset value (i.e. goodwill) for the past decade.

Why do you think these companies supposedly with some of the best financial minds in the world at their disposal would overpay that much for another company? A large part of it is that M&A is still one of the quicker and easier way to generate some positive buzz juicing up company stock. Hungry for future top-line growth (which is usually tied to executive pay) in a lack-luster world economy, corporation executives are more inclined overlook certain “ambiguity.”

Furthermore, increasing foreign acquisition in new/developing markets has also increased the risk of accounting discrepancy or min-interpretation more than most people have realized. Of course, the unprecedented synchronized QEs from world’s central banks have a big hand in over-valuation in almost all asset class as well.

It typically takes at least 2-3 years for companies to realize the full synergy, or discovering the dog, of an acquisition. Bloomberg quoted Erin Lyons, a Citigroup Inc. credit strategist, that some 44 companies listed on U.S. exchanges are potential candidates for write-downs, and that three S&P 500 companies — Frontier Communications Corp (NASDAQ: FTR), NASDAQ OMX Group, Inc. (NASDAQ:NDAQ) and L-3 Communications Holdings, Inc. (NYSE: LLL) — have more goodwill than market value.

So it looks like goodwill could turn nasty pretty soon for the U.S. companies, particularly the tech sector, which historically tends to have a bigger goodwill appetite than other industries.